by Mark Schiepp

February 1, 2022

I have felt compelled to keep you up-to-date monthly on the state of the economy because the progress of recovery from the pandemic recession has recently been both fragile and slow. Rising nervousness about the stock market and inflation are contributing to this fragility. In larger part however, there is deepening concern over the pandemic’s response by state and federal governments that has interfered with the return of the economy.

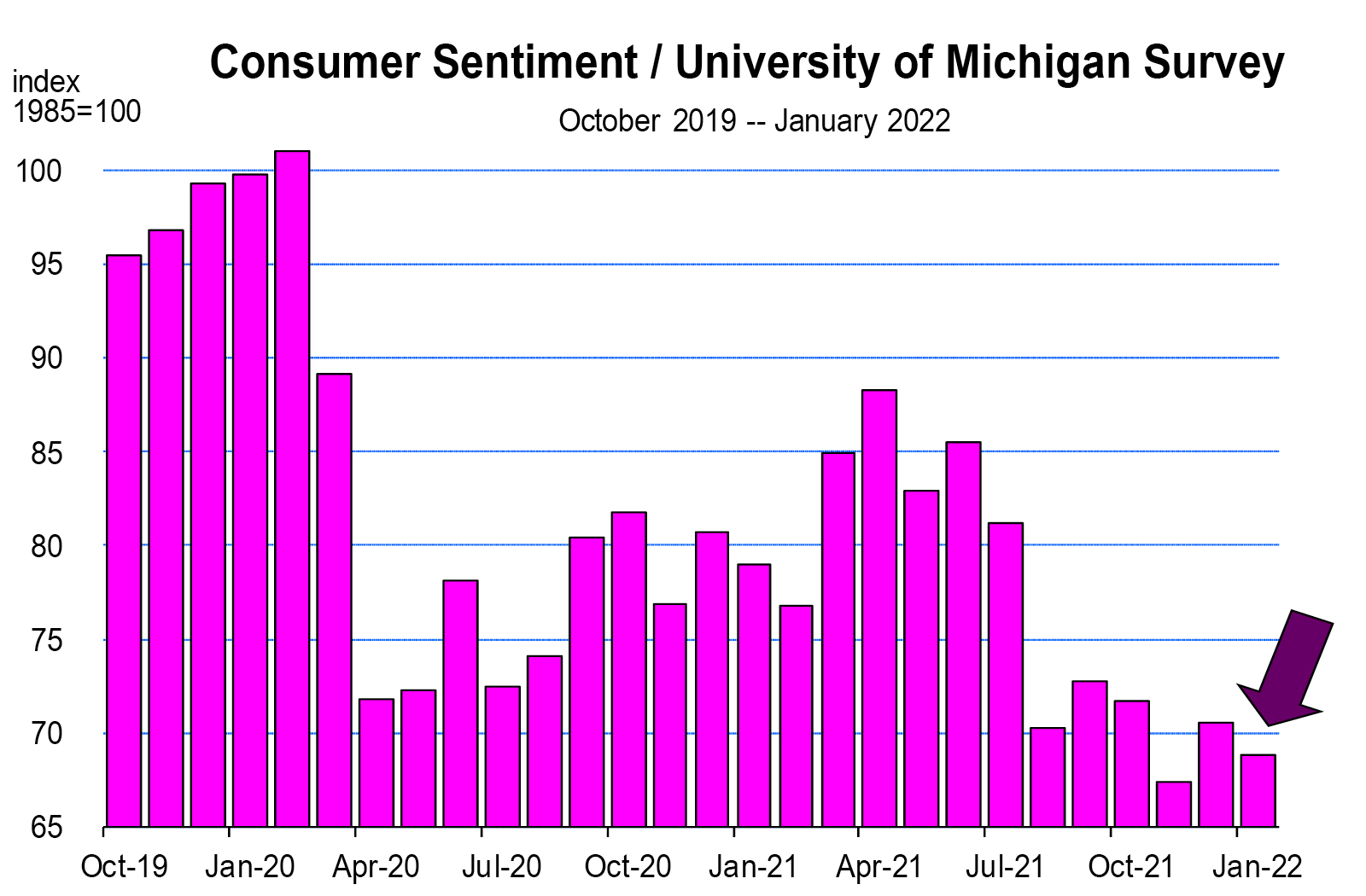

Consumers have jettisoned much of their optimism about future prospects for the economy. The sentiment index continues to flounder below the pandemic low. Is Omicron creating the reticence in people, or is it the response to how Omicron is being handled by state and local governments? I think the latter is more likely.

In response to the title of this newsletter: no; we are not back to normal. And I really don’t need to spell this out. Moody’s Analytics partnered with CNN to create the Back-to-Normal Index which uses 44 indicators to ascertain whether state economies have returned to pre-pandemic levels. The Back-to-Normal Index for California as of January 26 is 87 percent. Only Illinois, New York, Pennsylvania, Oregon, Massachusetts and Vermont are lower among all 50 states. Many state economies have slipped recently, including California which has the highest unemployment rate in the nation.

In response to the title of this newsletter: no; we are not back to normal. And I really don’t need to spell this out. Moody’s Analytics partnered with CNN to create the Back-to-Normal Index which uses 44 indicators to ascertain whether state economies have returned to pre-pandemic levels. The Back-to-Normal Index for California as of January 26 is 87 percent. Only Illinois, New York, Pennsylvania, Oregon, Massachusetts and Vermont are lower among all 50 states. Many state economies have slipped recently, including California which has the highest unemployment rate in the nation.

Why aren’t we normal yet? It could be that we still have the following experiments underway that are not normal:

- Massive fiscal policy

- Continuation of massive bond buying by the Fed

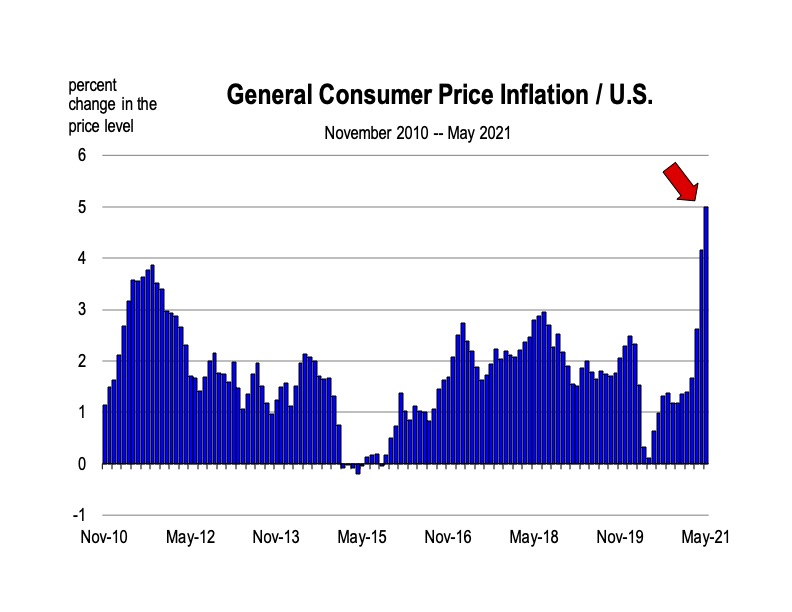

- No interest rate hikes yet to suppress ongoing and rising inflation (yes, the second derivative of the CPI is still positive through January 2022)

- Vaccination mandates1

More fiscal policy is simply not needed for an economy that initially rebounded back sharply on its own by removing restrictions. Now it has become the root cause of current inflation and more Americans see this clearly.

While the Fed has indeed tapered, they are still massively expanding monetary policy with $60 billion of bond purchases this month and next. And though rate hikes are going to occur this year, why have they not occurred yet when we need to have inflation shut down as soon as possible?

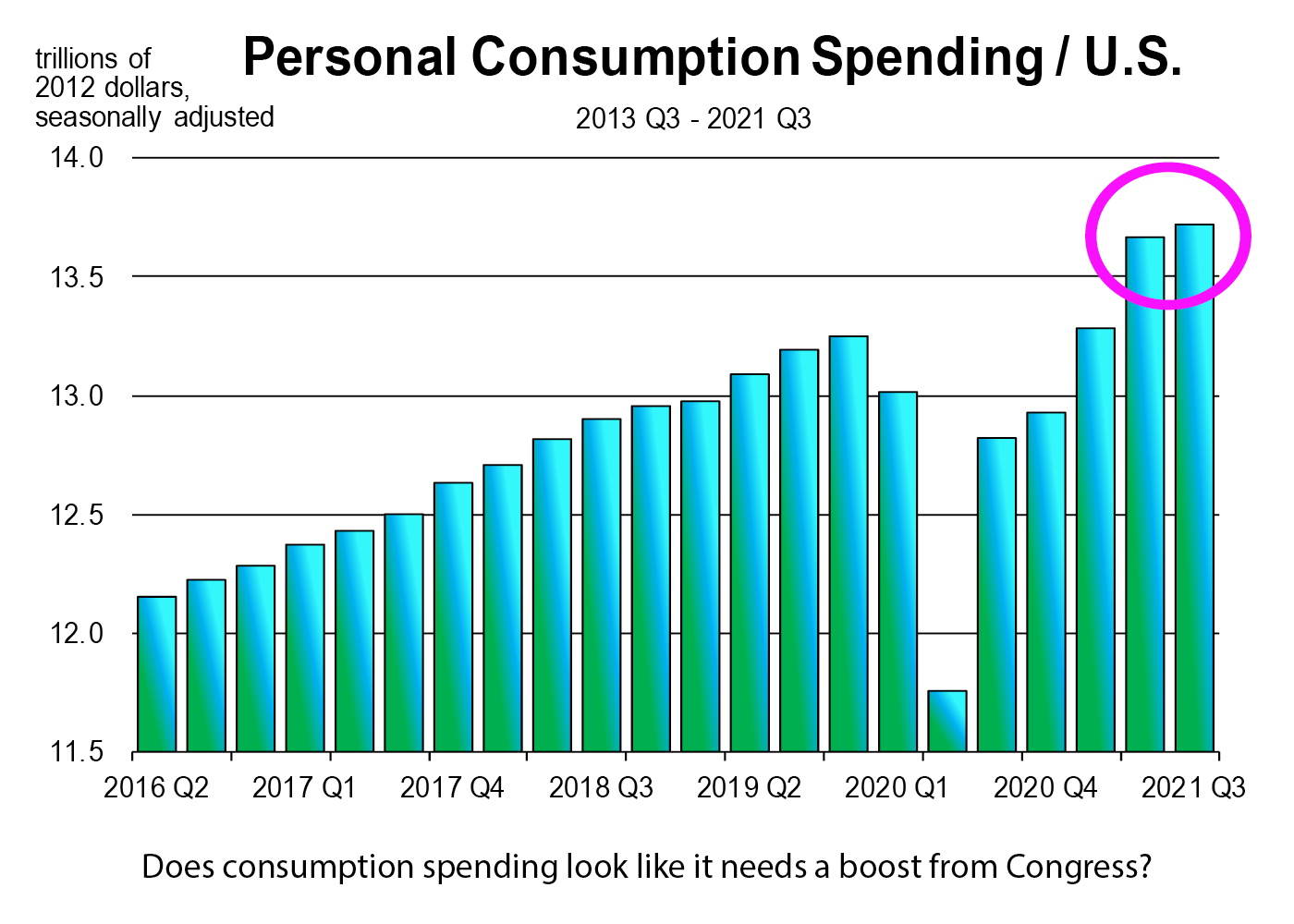

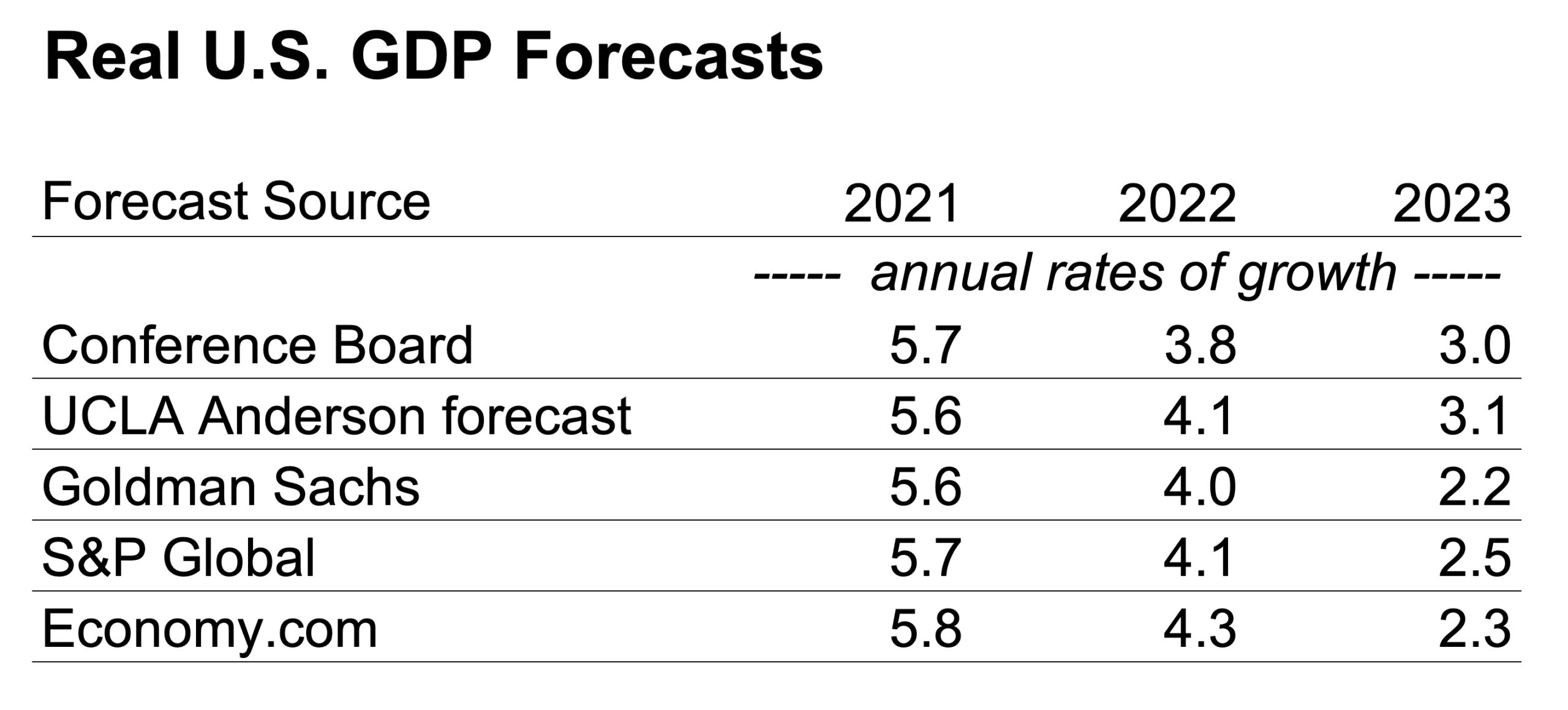

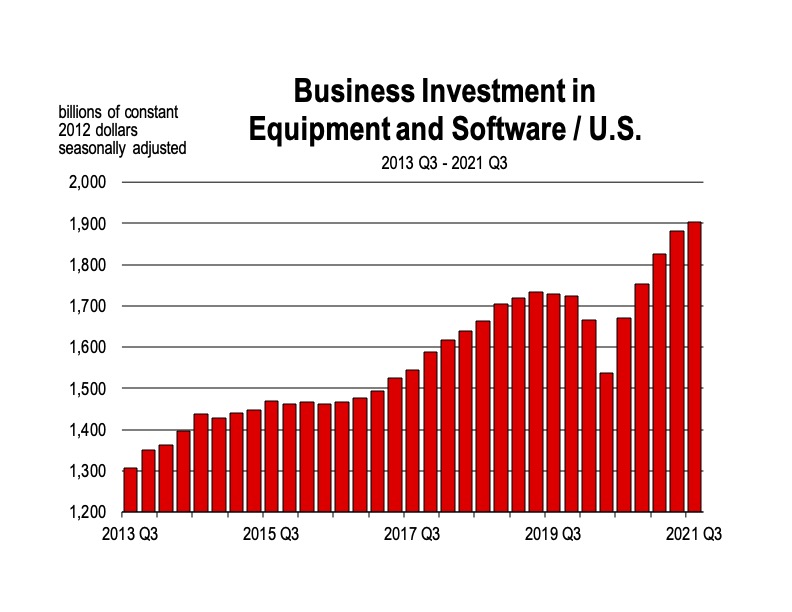

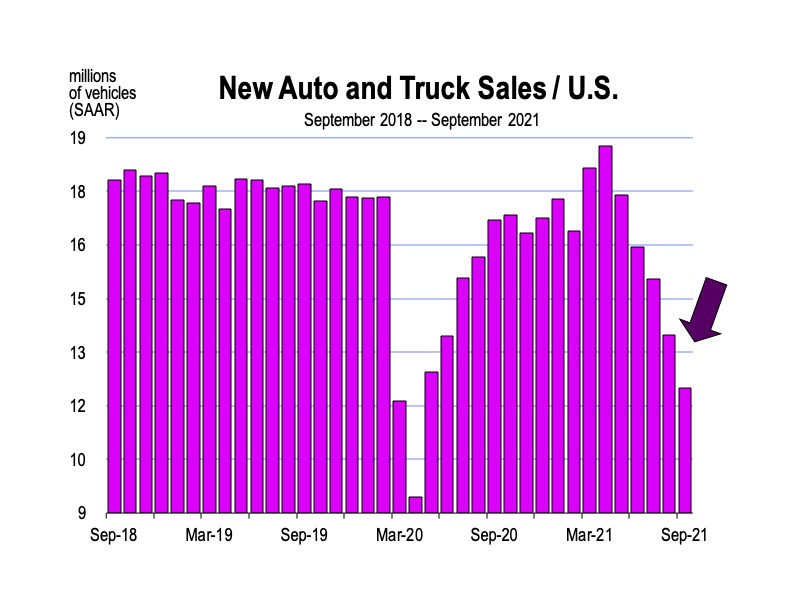

It’s likely because of the stock market correction throughout the month of January, and the fear that a bear market may prevail if the juice for the markets is withdrawn too fast. The economy may also be wobbling some. Recent news on U.S. manufacturing shows a softening, particularly in the delivery of finished goods. The near term outlook for manufacturing is compromised by the supply chain issues which are not resolving fast enough. GDP growth was sharply higher in the 4th quarter, but much of this was due to inventories which will have a depressing impact on the first quarter 2022 GDP report.

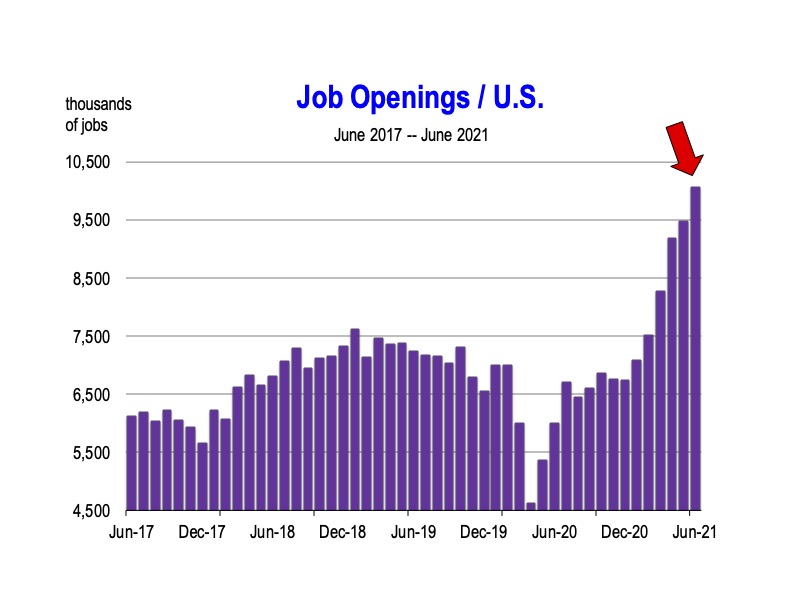

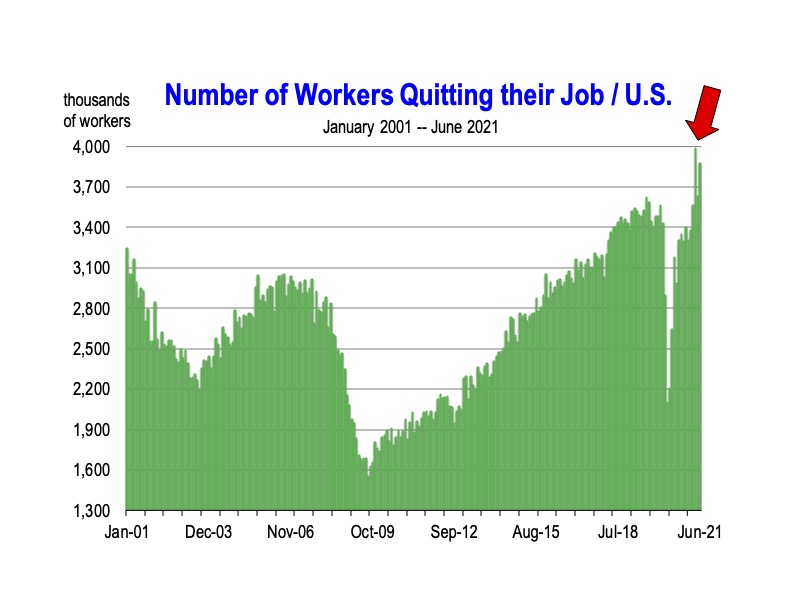

We Need More Workers

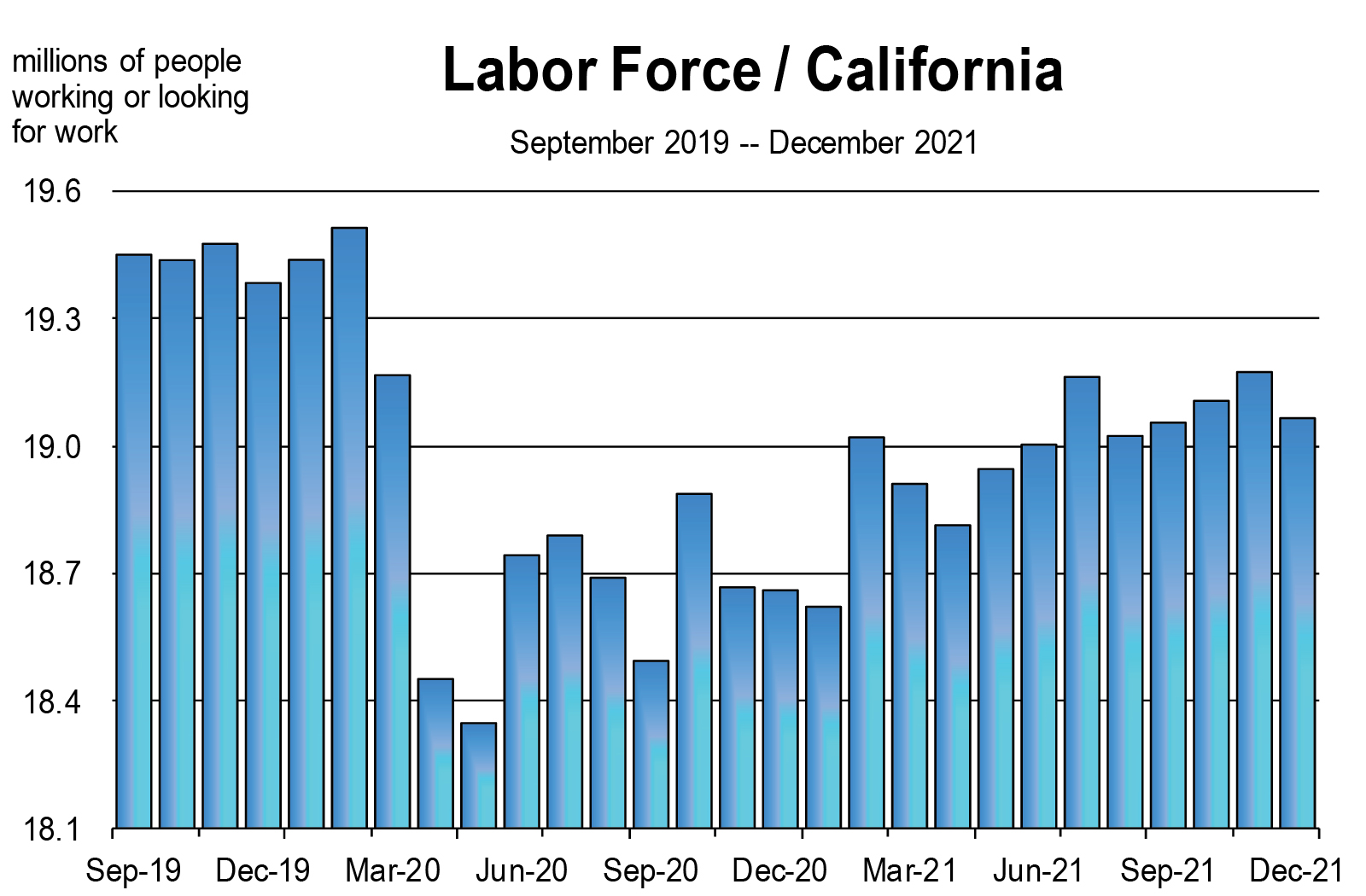

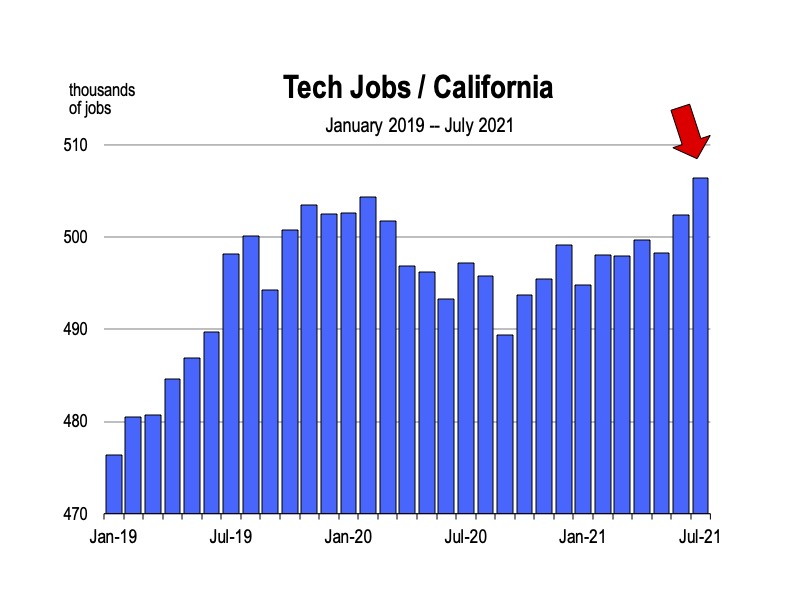

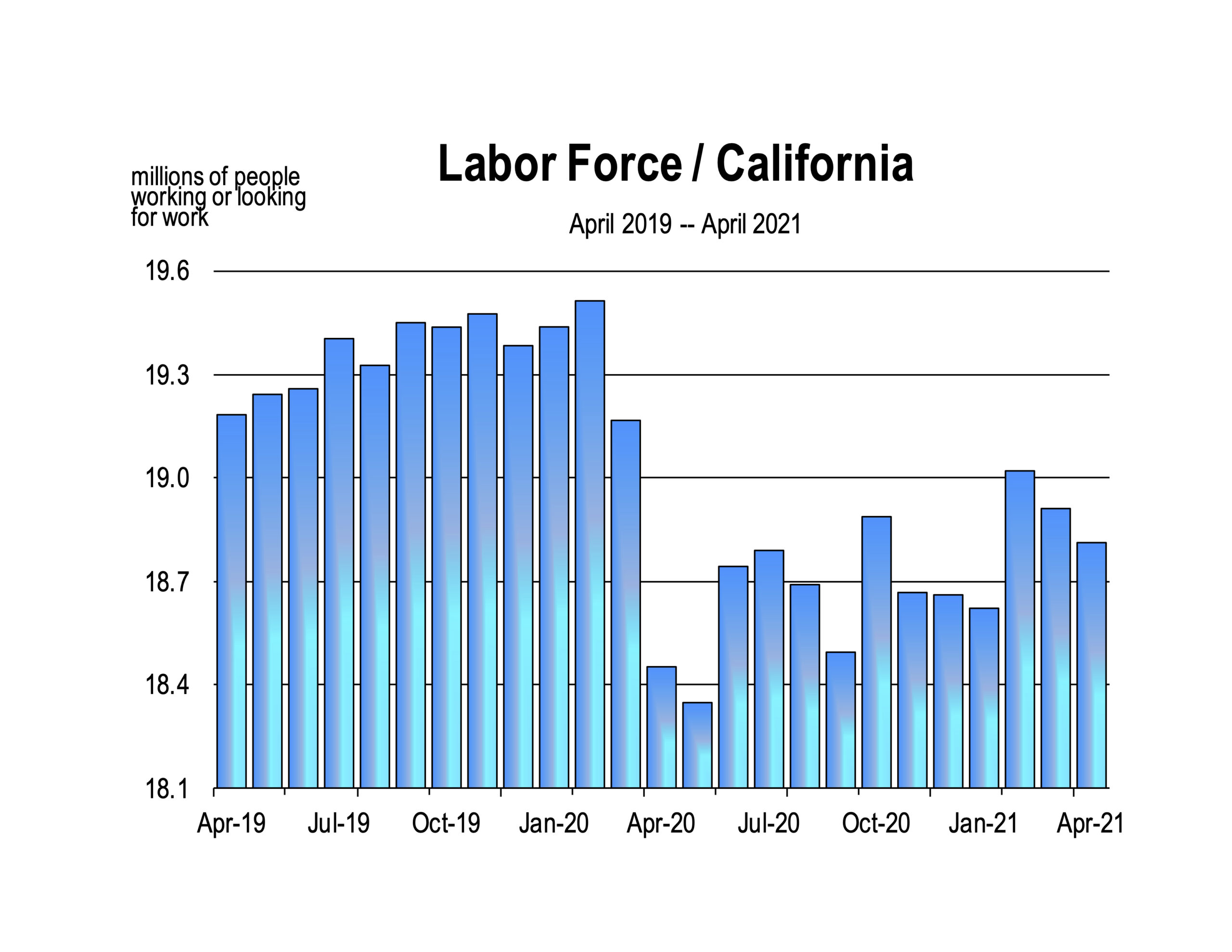

Labor availability issues remain with little relief through December. In California, many employment sectors have fully recovered or are close to complete recovery. But the labor force has not. California is still 400,000 potential workers short of the labor force peak that prevailed just before the pandemic hit. This is one of the most abnormal issues in California that remains seriously problematic to the restoration of the workforce and delivery of normal services to consumers, especially leisure and food services. The vaccine mandates may certainly be contributing to the drag on the labor force recovery.

Logistic Issues Persist

Logistic Issues Persist

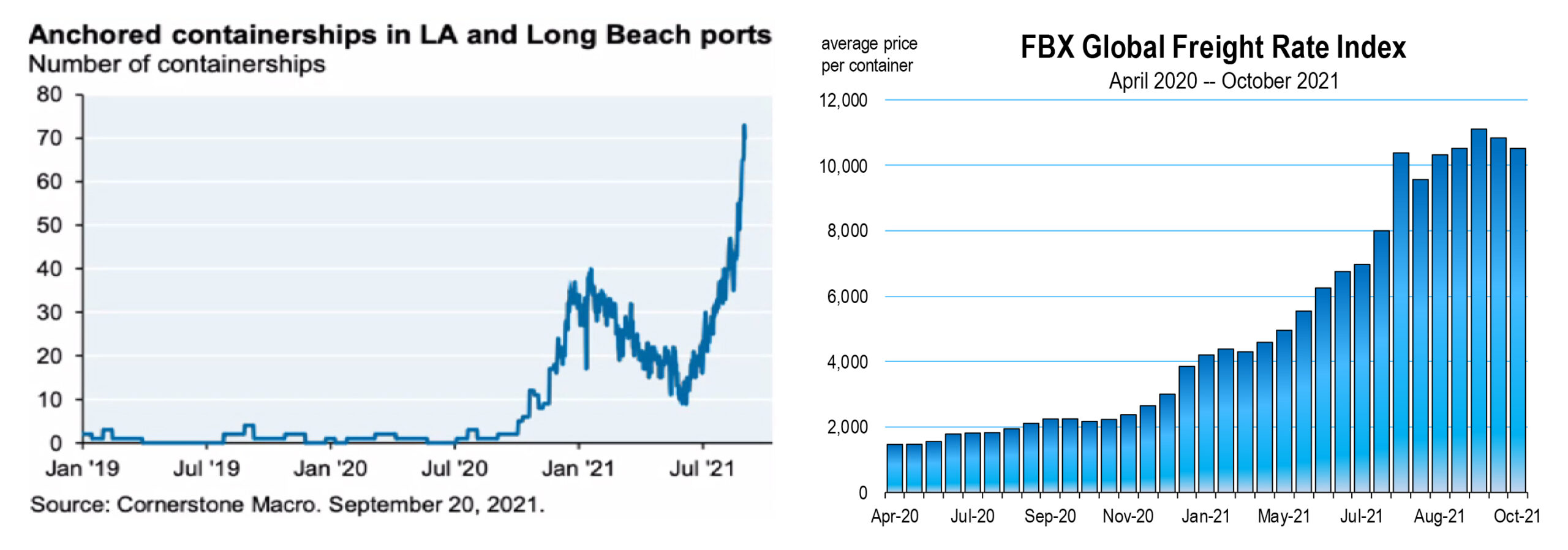

Supply issues persist and the manifestation of this is empty store shelves, which are pervasive today.2 Green onion rationing at Trader Joes? They told me to grow my own.

The backlog of containers with furniture, clothing, electronics and other imports that were piling up at the Los Angeles and Long Beach ports last summer and fall has been dwindling.

The so-called dwell time a container sits around on average before it gets picked up has fallen by more than half since late October and there are no longer dozens of ships at anchor outside the ports waiting for weeks before they can berth and offload their cargo.

But stacks of empty containers are preventing truck drivers from leaving their own empties and swapping them for fulls to deliver to desperately needed destinations. Furthermore, more ships heading this way from Asia are on the horizon. Unless a plan is devised for empty containers hording Port space, ongoing congestion problems will persist.

What We Need Right Now

I typically hesitate to make recommendations on what needs to occur to put the state on a faster track to normalization. But clearly, the experiments underway are obstructing this path, making more people fearful and/or pessimistic, and infuriating others. We can see it in the data. Therefore, putting my hesitation aside, here’s what needs to happen, IMHO:

Reverse the experiments—all of them. They are not normal anyway and largely unnecessary.

Don’t think of passing another spending or stimulus bill in Congress. In fact, rescind the $1.2 trillion Infrastructure Bill.

We should be accelerating the tapering of the quantitative easing or bond buying program, or entirely withdrawing it. We should not be waiting until March to raise interest rates. Rates should be hiked now. We need some bold moves that we saw work wonders in the past. The last time the Fed actively put downward pressure on inflation, the policy worked. This was in 1979. Aggressive increases in the federal funds and discount rates started in August when Paul Volker became the new Fed chair. This continued through April of 1980. Inflation peaked that month, and tumbled thereafter.

The courts have spoken about vaccine mandates. We need to end these now along with the passports. We should also be following in the footsteps of the United Kingdom and declare the pandemic over. This might by itself get us further back to normal than anything else.

1 Senate Bill 871 would add the coronavirus vaccine to the list of required school vaccines (with no exemptions) on January 1, 2023. Federal, state, and local authorities are requiring certain categories of workers to be vaccinated. Vaccine proof is required in Los Angeles County. Legislation in Sacramento is being designed to require vaccines for all people in workplaces, schools, and public venues like malls, museums and restaurants.

2 In previous newsletters, I have written extensively about the global supply chain disruptions due to congestion at ports and shortages of truck drivers and service workers in previous newsletters.

The California Economic Forecast is an economic consulting firm that produces commentary and analysis on the U.S. and California economies. The firm specializes in economic forecasts and economic impact studies, and is available to make timely, compelling, informative and entertaining economic presentations to large or small groups.

![]()

Into January 2022 we go and the pandemic continues; its future progression (or how long governments will continue to maintain a state of emergency in the name of public health) is uncertain. We generally believe the pandemic will be brought under control and that the disruptions and frictions it has caused in the labor market and to the supply chain will be resolved over time.

Into January 2022 we go and the pandemic continues; its future progression (or how long governments will continue to maintain a state of emergency in the name of public health) is uncertain. We generally believe the pandemic will be brought under control and that the disruptions and frictions it has caused in the labor market and to the supply chain will be resolved over time.

These are the four biggest issues that we, as consumers and businesses are facing in 2021. Moreover, these issues will not be resolved by year’s end. An escalation of at least two of these issues is likely, given that we’ve seen very little resolution to date.

These are the four biggest issues that we, as consumers and businesses are facing in 2021. Moreover, these issues will not be resolved by year’s end. An escalation of at least two of these issues is likely, given that we’ve seen very little resolution to date. The current Congress has already passed $3.1 trillion in spending bills this year, creating not only a surge of federal debt, but a potential surge in government spending which is front loaded for 2022, 2023, and 2024.

The current Congress has already passed $3.1 trillion in spending bills this year, creating not only a surge of federal debt, but a potential surge in government spending which is front loaded for 2022, 2023, and 2024.

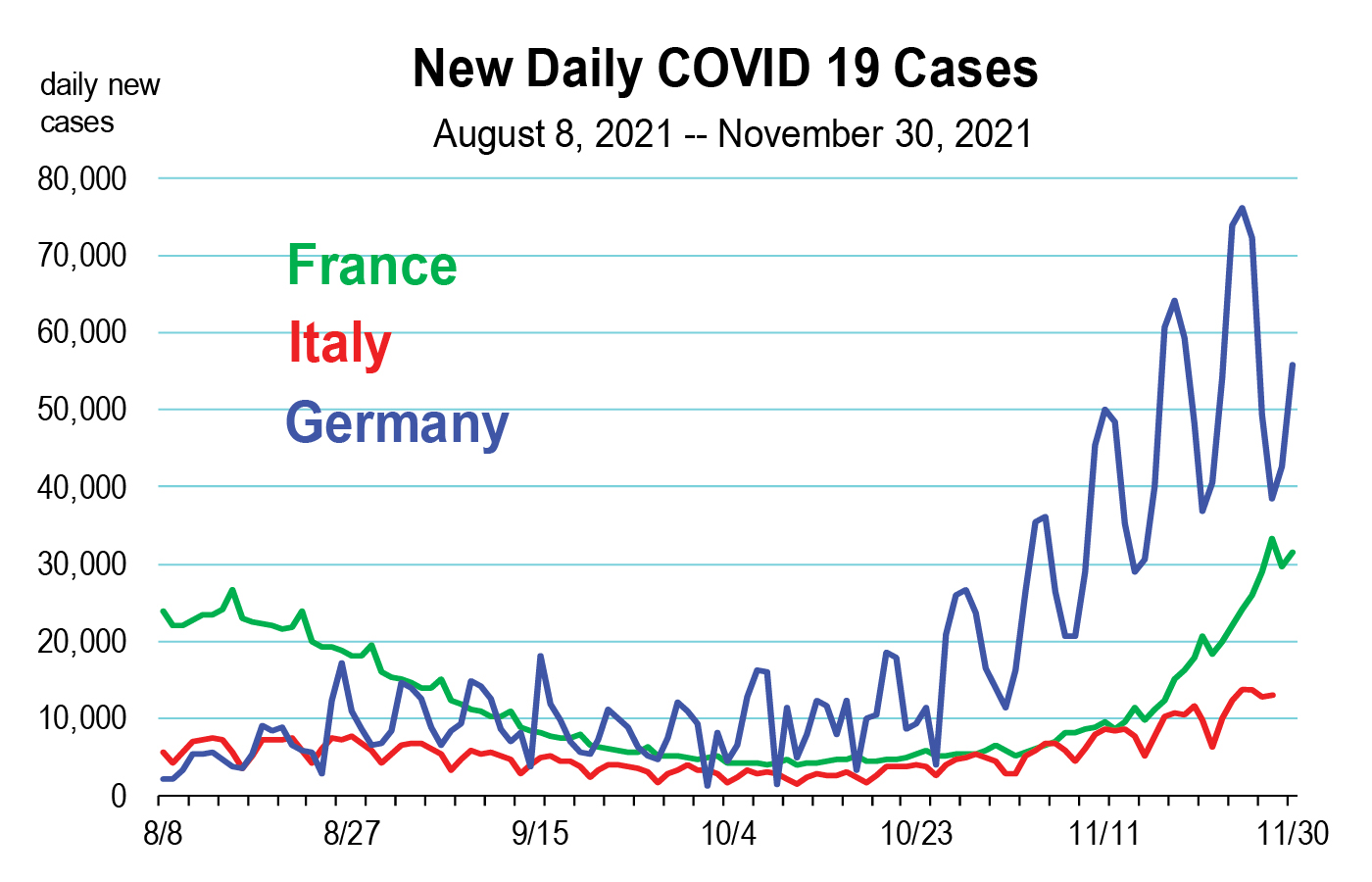

The global economic recovery remains tethered to the pandemic. And another wave is coming. We are seeing it in Europe, notably Germany and Austria. In Austria, a vaccine mandate and a national lockdown have now been imposed. In Germany, daily cases are now more than twice as high as they have ever been during the course of the entire pandemic.

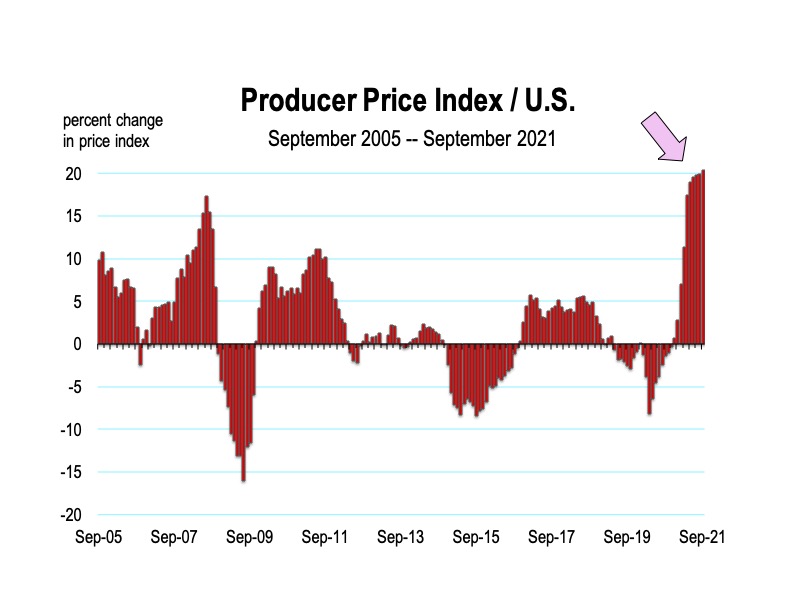

The global economic recovery remains tethered to the pandemic. And another wave is coming. We are seeing it in Europe, notably Germany and Austria. In Austria, a vaccine mandate and a national lockdown have now been imposed. In Germany, daily cases are now more than twice as high as they have ever been during the course of the entire pandemic. Moreover, producer price inflation has now hit 20 percent year-over-year. This is the highest rate of inflation in producer (or wholesale) prices since 1974.

Moreover, producer price inflation has now hit 20 percent year-over-year. This is the highest rate of inflation in producer (or wholesale) prices since 1974. The persistence and/or increase in inflation would have meaningful economic and financial consequences. And I believe we are more apt to see a persistence of inflation than we are to see stagnant growth because the evidence for the latter is relatively absent today.

The persistence and/or increase in inflation would have meaningful economic and financial consequences. And I believe we are more apt to see a persistence of inflation than we are to see stagnant growth because the evidence for the latter is relatively absent today.

But what’s the chance?

But what’s the chance? Global supply disruptions continue to hamper the U.S. economy, contributing to the acceleration of inflation. It doesn’t take a rocket scientist to notice the clear evidence that supply-chain issues are creating economic costs.

Global supply disruptions continue to hamper the U.S. economy, contributing to the acceleration of inflation. It doesn’t take a rocket scientist to notice the clear evidence that supply-chain issues are creating economic costs.

by Mark Schniepp

by Mark Schniepp The impact on the economy of California was more significant than the rest of the nation but the recovery will progress at a faster pace, catching up to the U.S. by 2023.

The impact on the economy of California was more significant than the rest of the nation but the recovery will progress at a faster pace, catching up to the U.S. by 2023. The Great Resignation

The Great Resignation Remote work and virtual meetings will continue

Remote work and virtual meetings will continue by Mark Schniepp

by Mark Schniepp

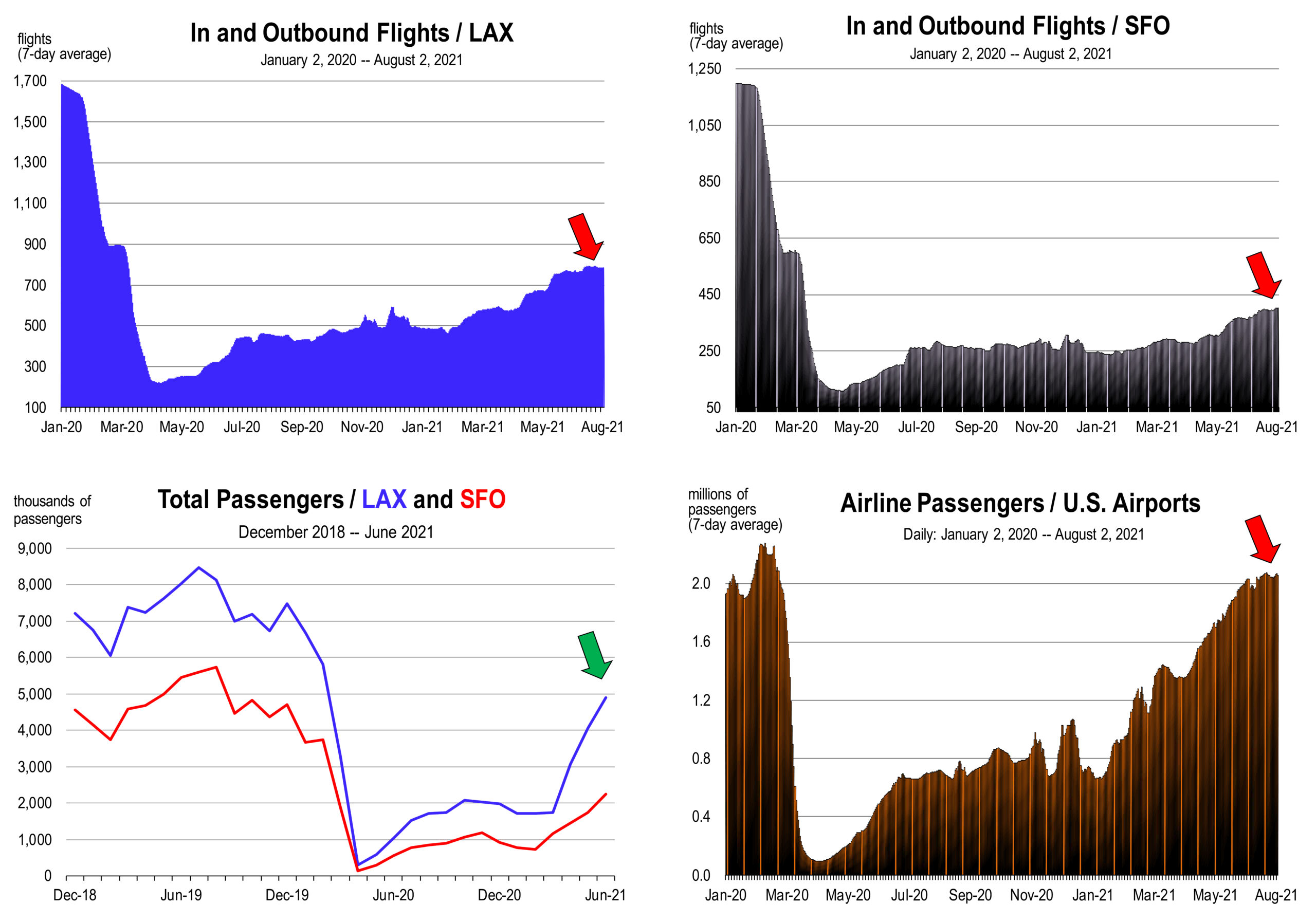

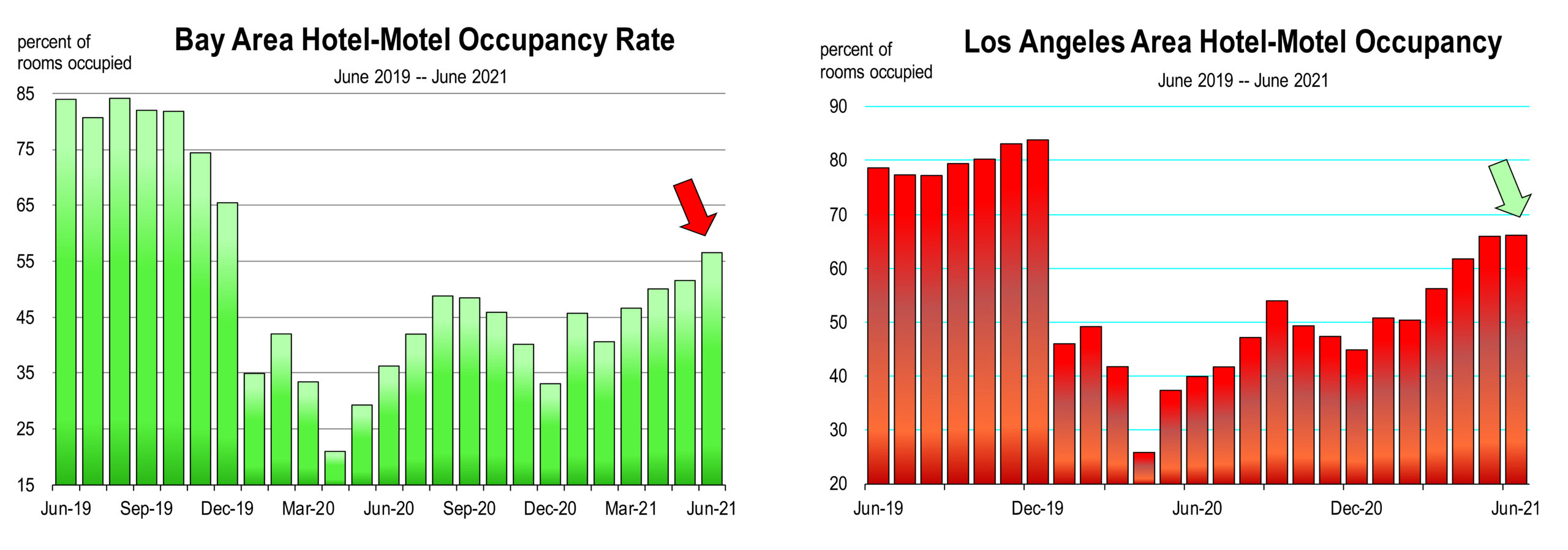

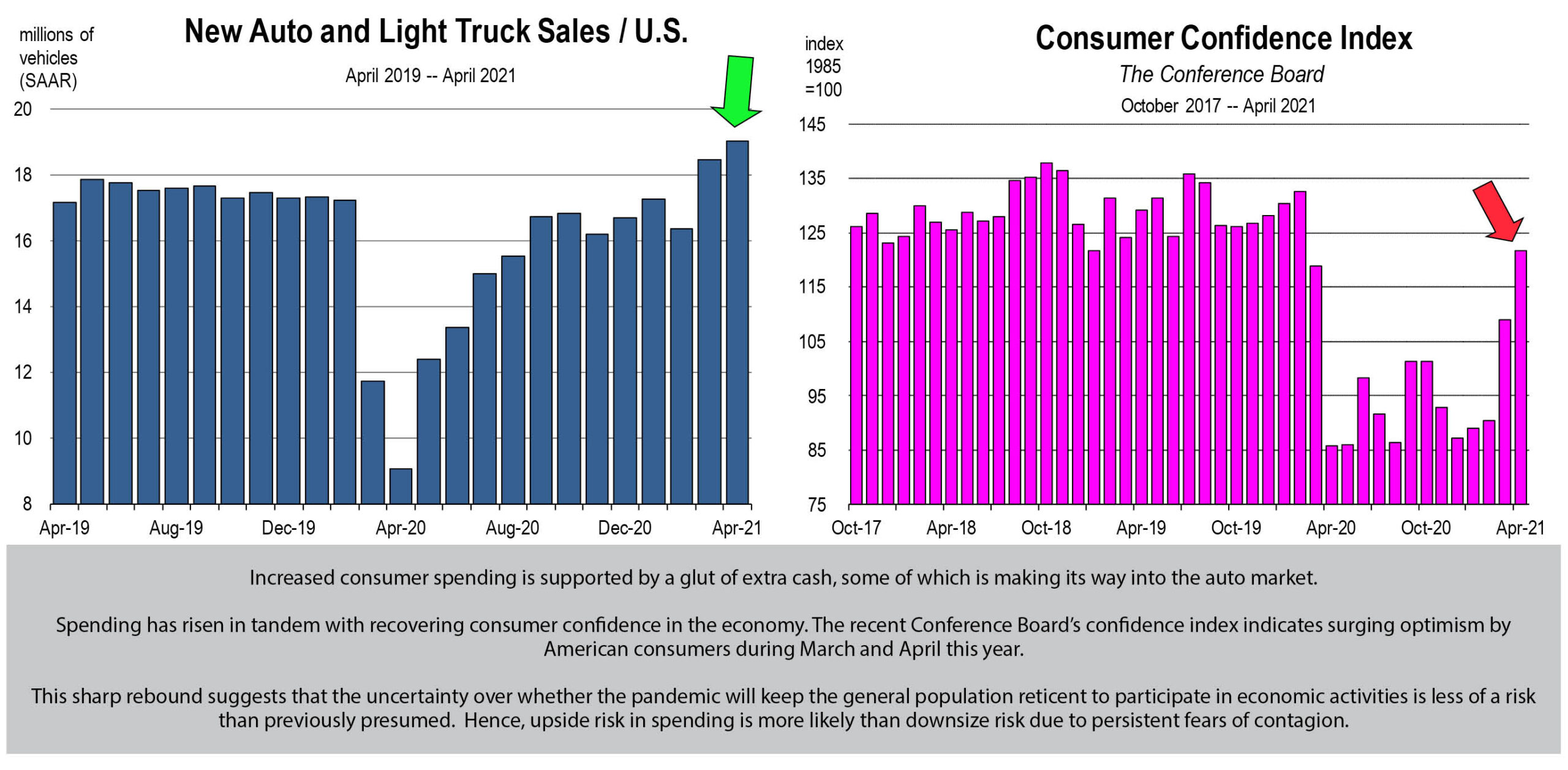

While air passenger travel in California has recovered 66 percent, passenger travel nationwide has recovered nearly 80 percent, and the clear increase in travel has produced higher hotel-motel occupancy rates.

While air passenger travel in California has recovered 66 percent, passenger travel nationwide has recovered nearly 80 percent, and the clear increase in travel has produced higher hotel-motel occupancy rates.

Travel related price increases are very likely catchup from the steeply discounted prices offered a year ago when no one was traveling anywhere.

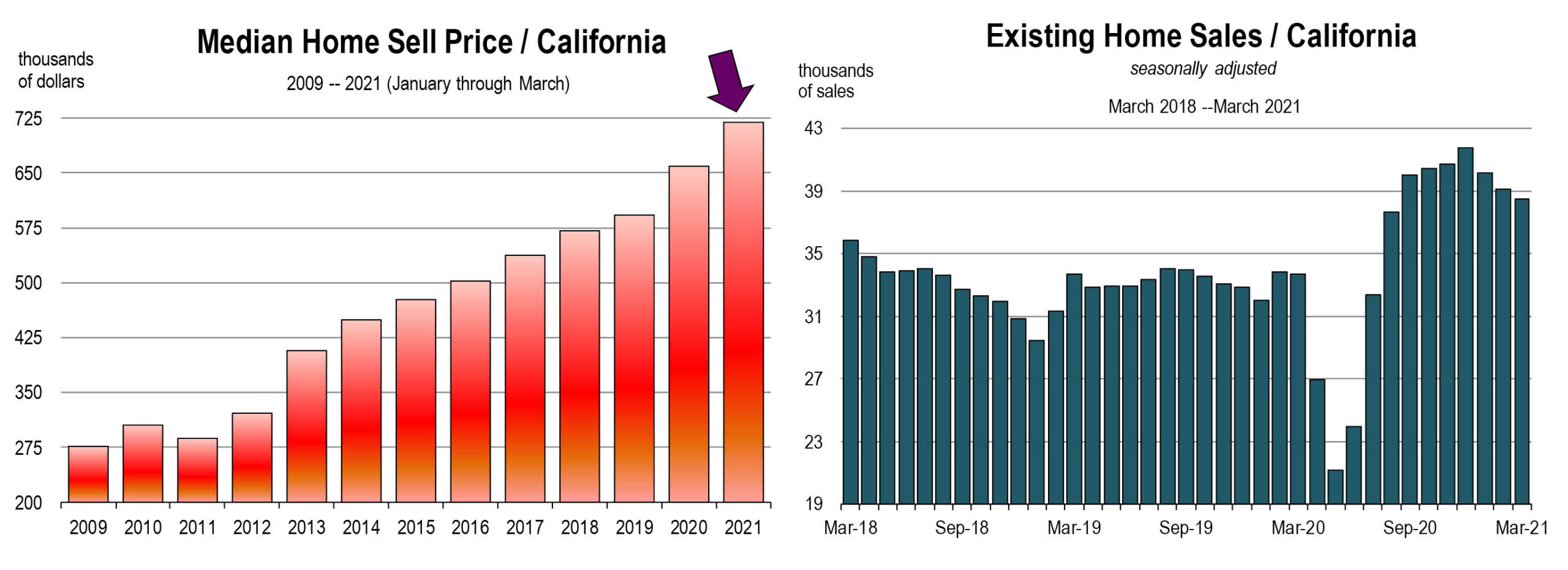

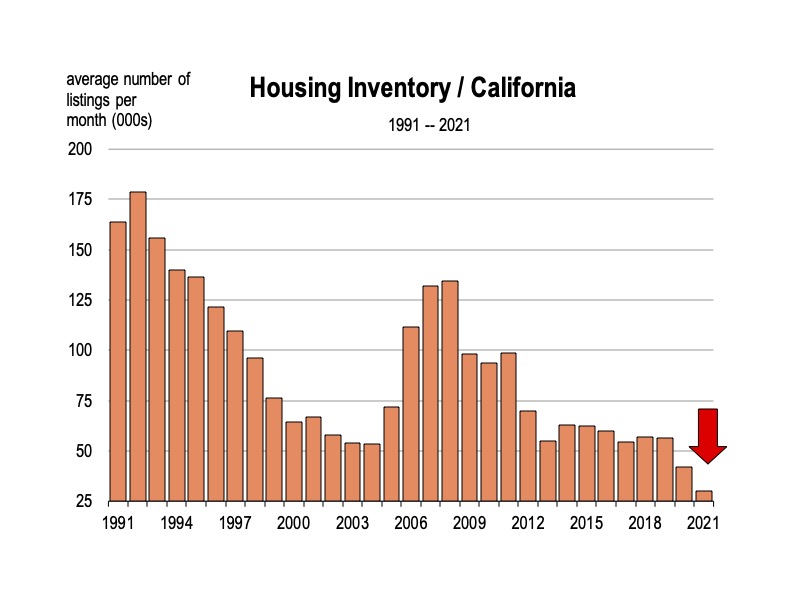

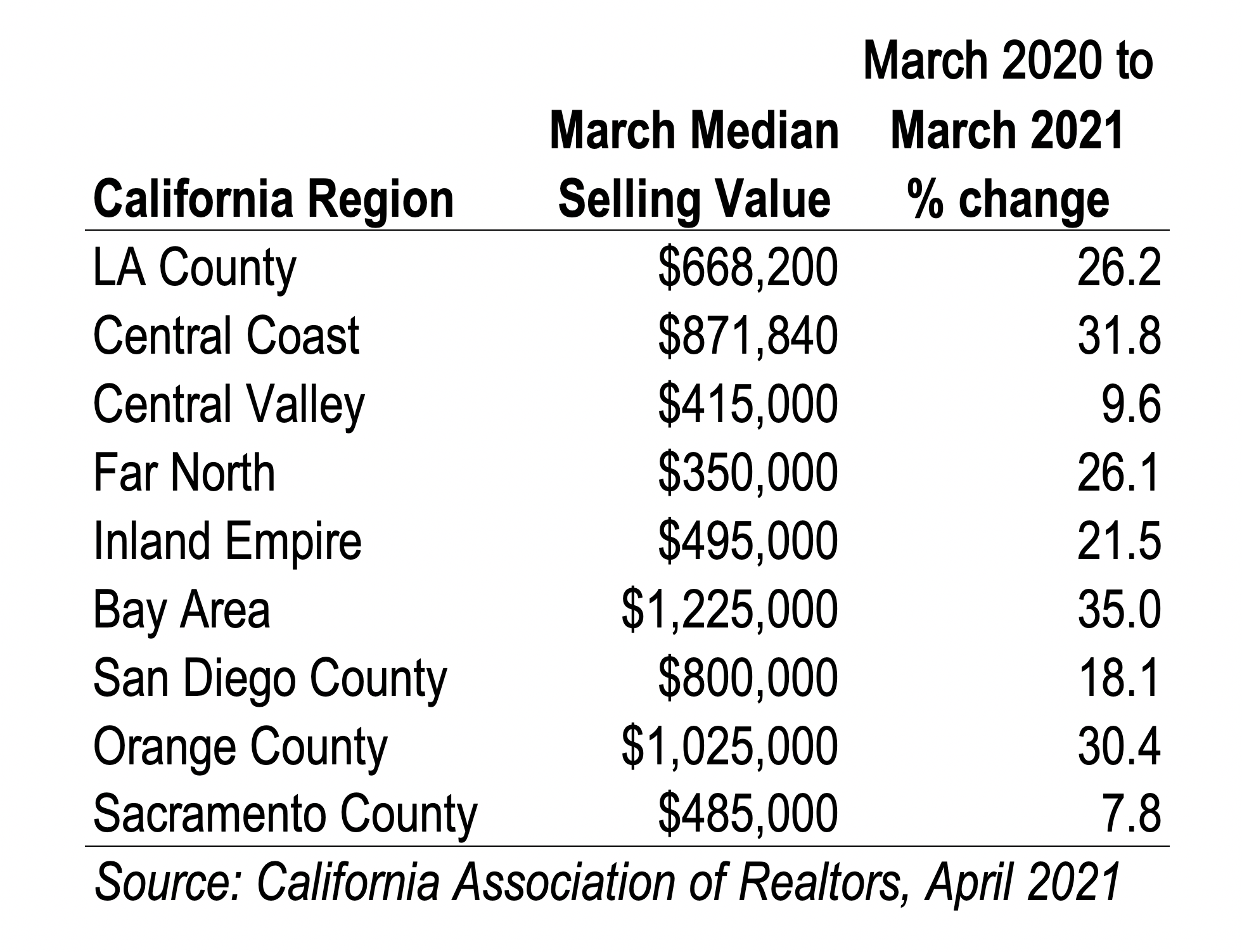

Travel related price increases are very likely catchup from the steeply discounted prices offered a year ago when no one was traveling anywhere. Only 1.16 million homes were on the market in April, a 20 percent drop from a year ago, according to the National Association of Realtors. In California, over the last 6 months, inventory levels have declined to their lowest on record.

Only 1.16 million homes were on the market in April, a 20 percent drop from a year ago, according to the National Association of Realtors. In California, over the last 6 months, inventory levels have declined to their lowest on record. What will be different?

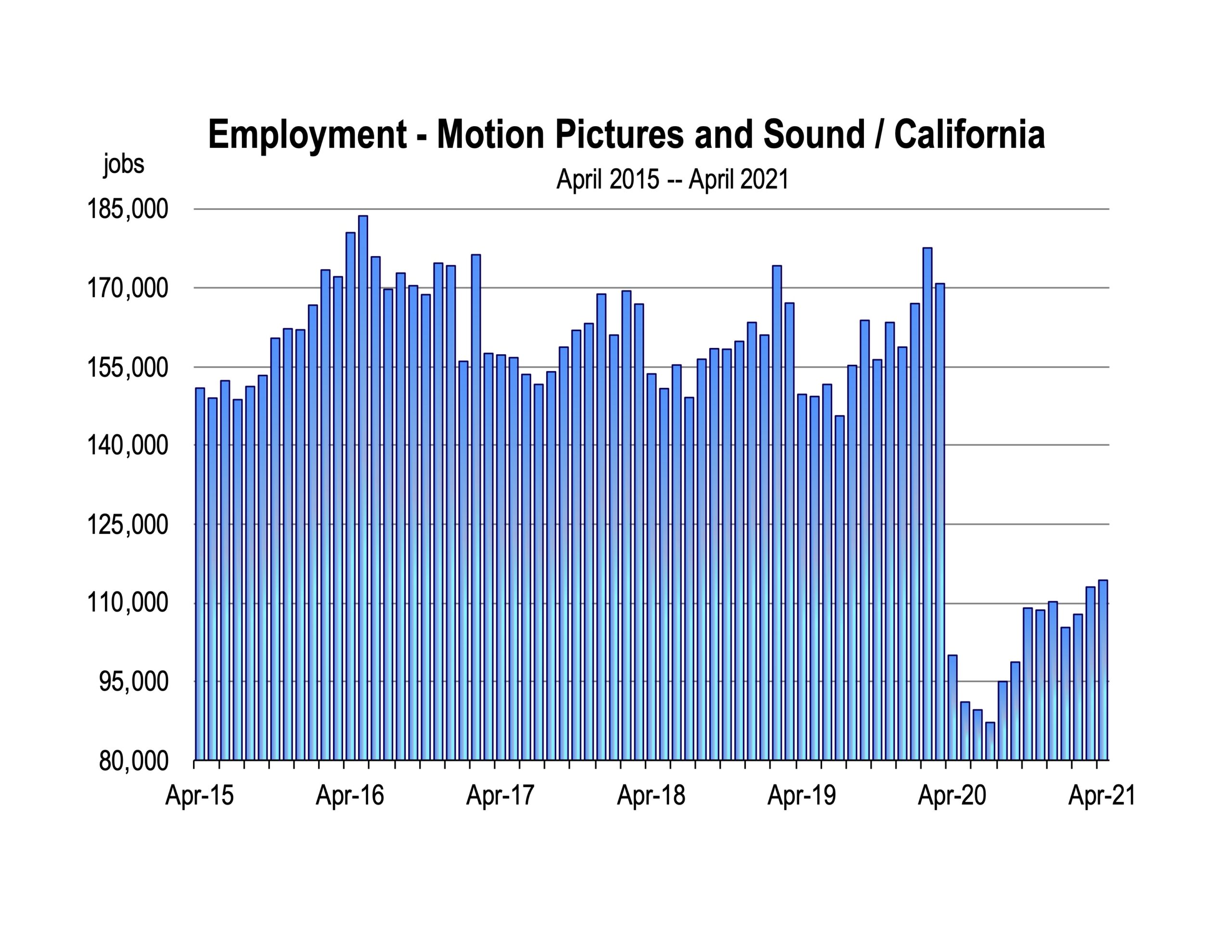

What will be different? As the labor force rebounds, so will jobs in food services, hospitality and entertainment. As international travel resumes, larger gains are expected.

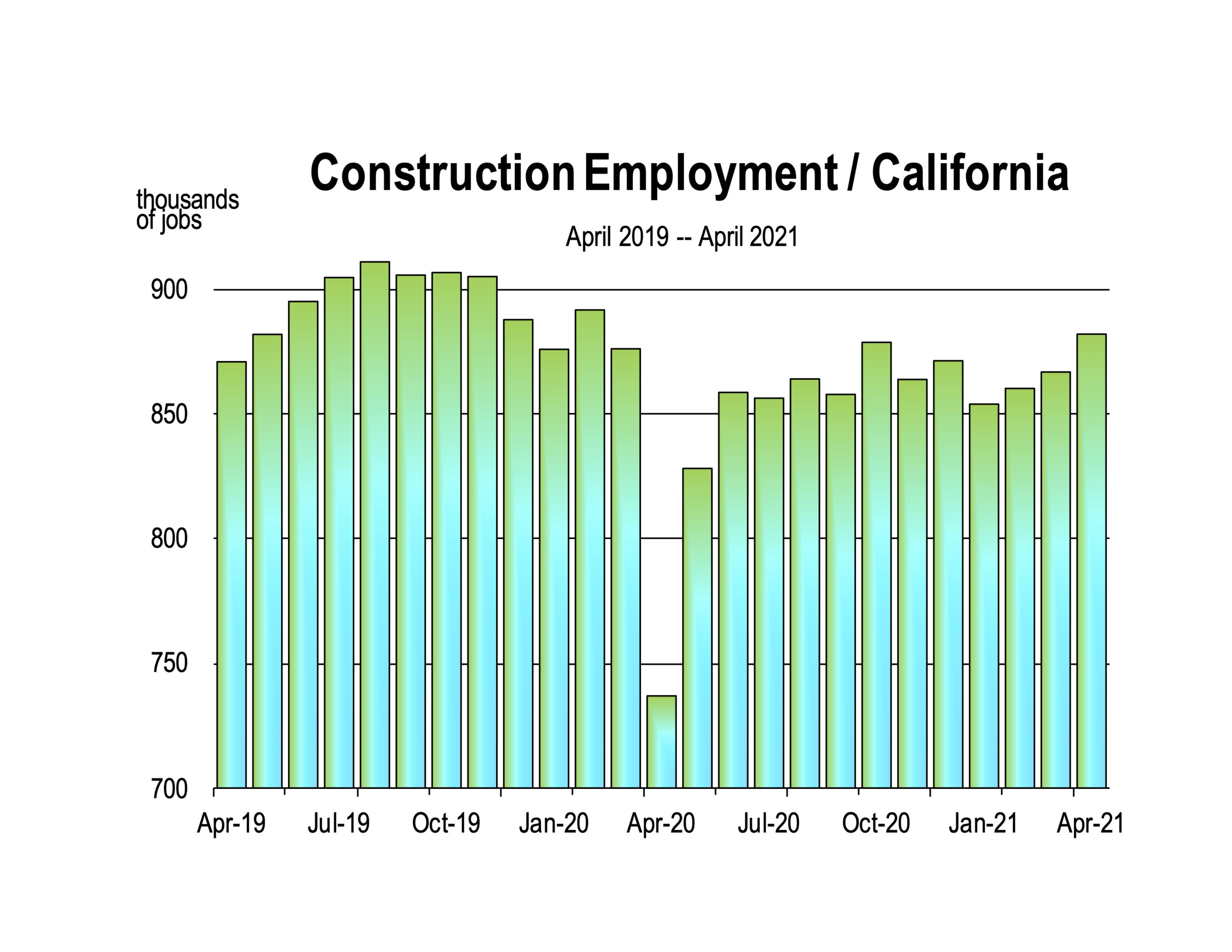

As the labor force rebounds, so will jobs in food services, hospitality and entertainment. As international travel resumes, larger gains are expected. New construction is underway all over Los Angeles, including LAX. The high-speed rail project continued through the pandemic and employs more workers now than at any other time. Large multi-family building projects have resumed in San Francisco and Sacramento. In downtown Los Angeles, they never stopped.

New construction is underway all over Los Angeles, including LAX. The high-speed rail project continued through the pandemic and employs more workers now than at any other time. Large multi-family building projects have resumed in San Francisco and Sacramento. In downtown Los Angeles, they never stopped. A return to normal

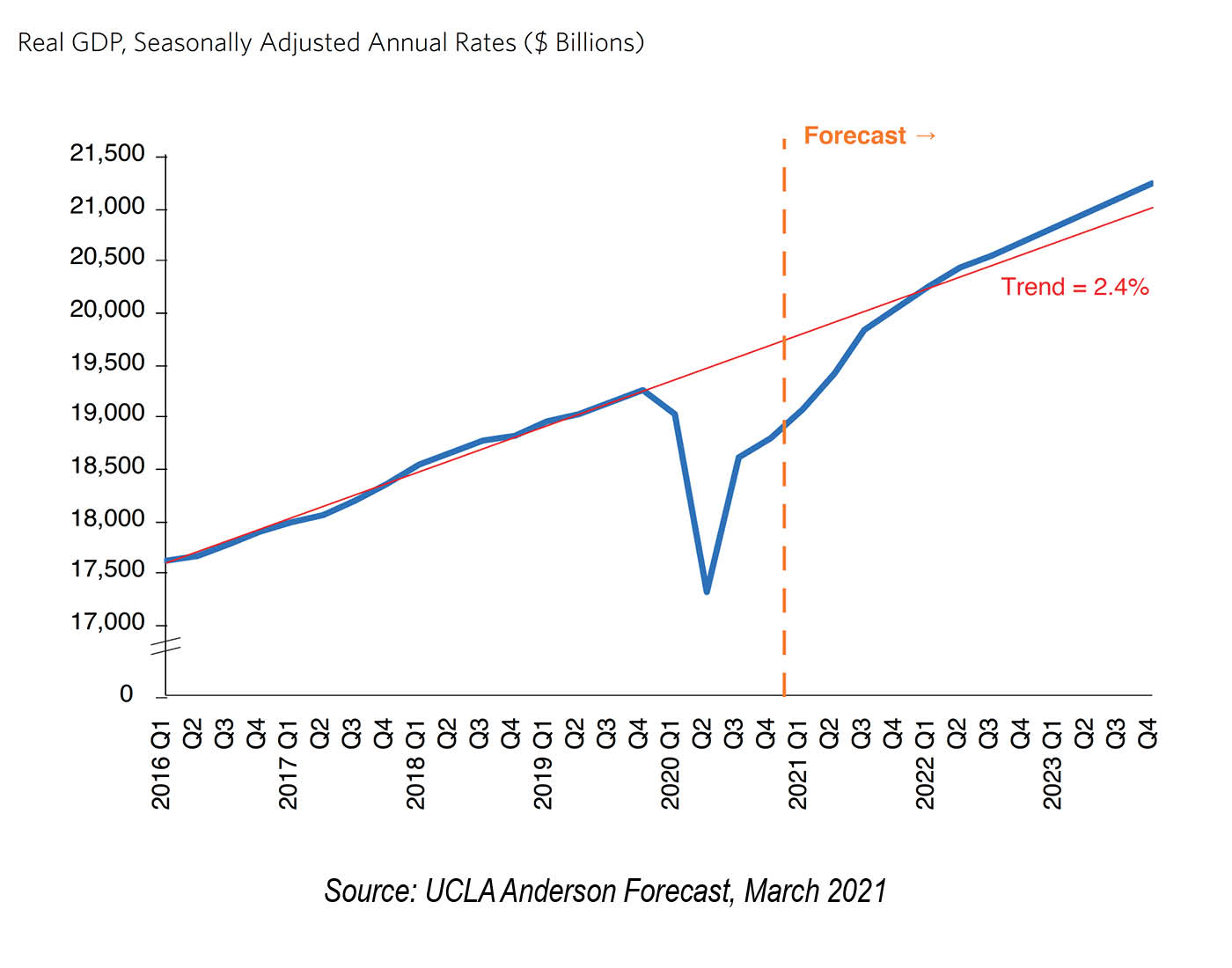

A return to normal Early spring and it’s all good news at this point. Though the improvement in the U.S. economy this year was expected, the actual levels of growth are better than anticipated.

Early spring and it’s all good news at this point. Though the improvement in the U.S. economy this year was expected, the actual levels of growth are better than anticipated.

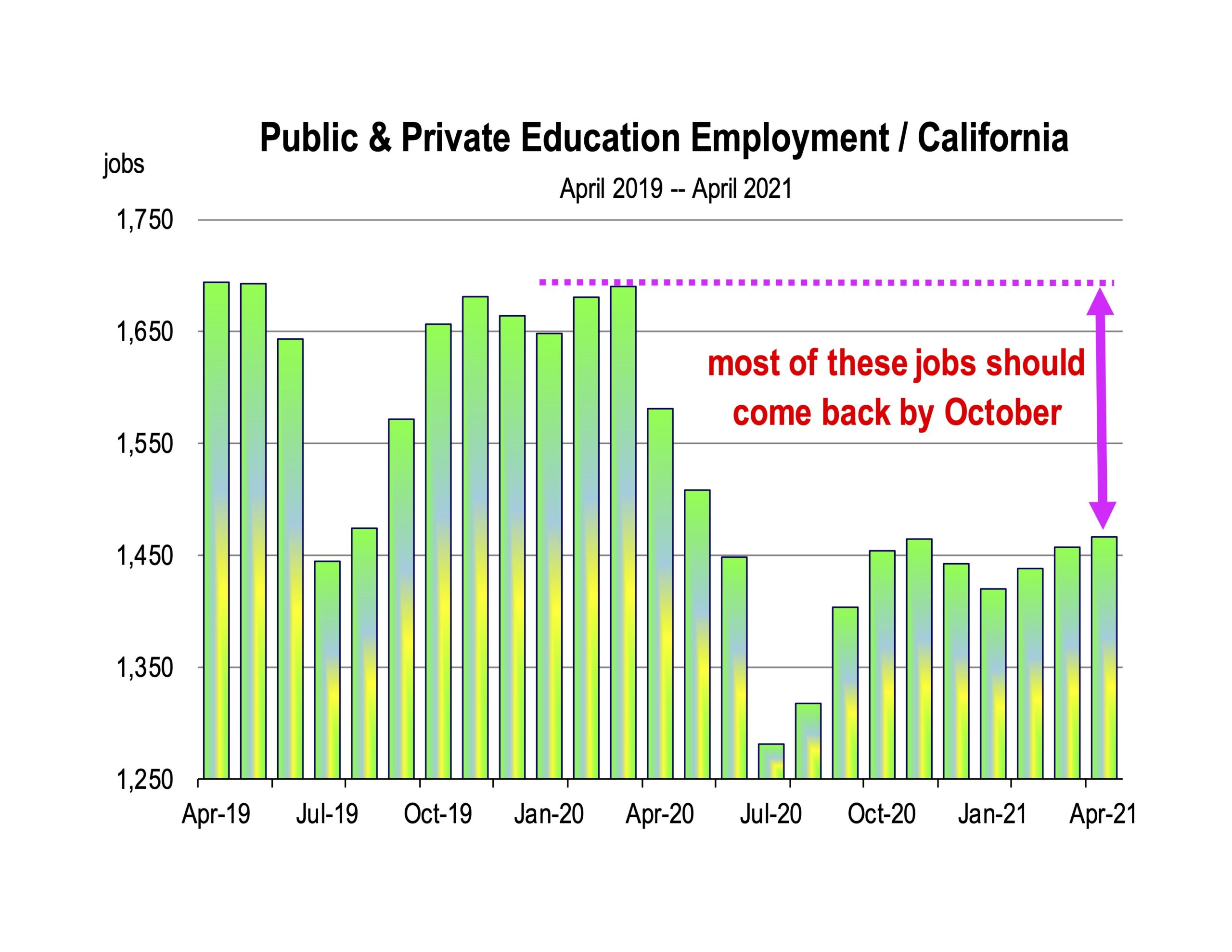

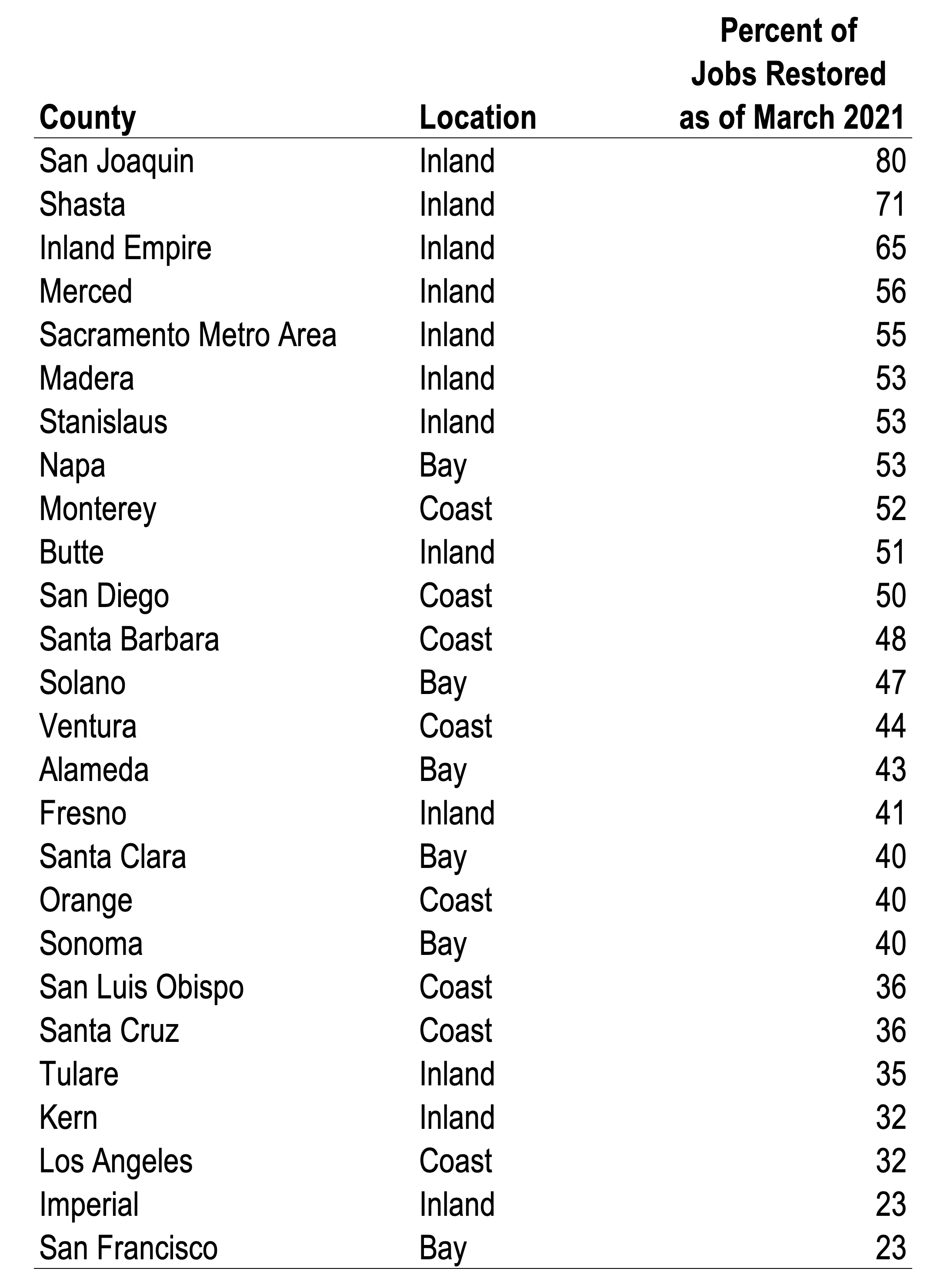

Through April 2021, the recovery is geographically uneven across the state, with inland counties reinstating their workforces faster than coastal counties or the Bay Area.

Through April 2021, the recovery is geographically uneven across the state, with inland counties reinstating their workforces faster than coastal counties or the Bay Area. We look forward to June

We look forward to June