Mark Schniepp

April 2026

Uncertainty

A year ago, tariff hysteria gripped the nation, the stock market, and all the talking heads on TV who predicted carnage and chaos in the form of higher inflation, infuriating the nations we trade with, and interrupting economic growth. Clearly this was politically motivated because none of that happened.

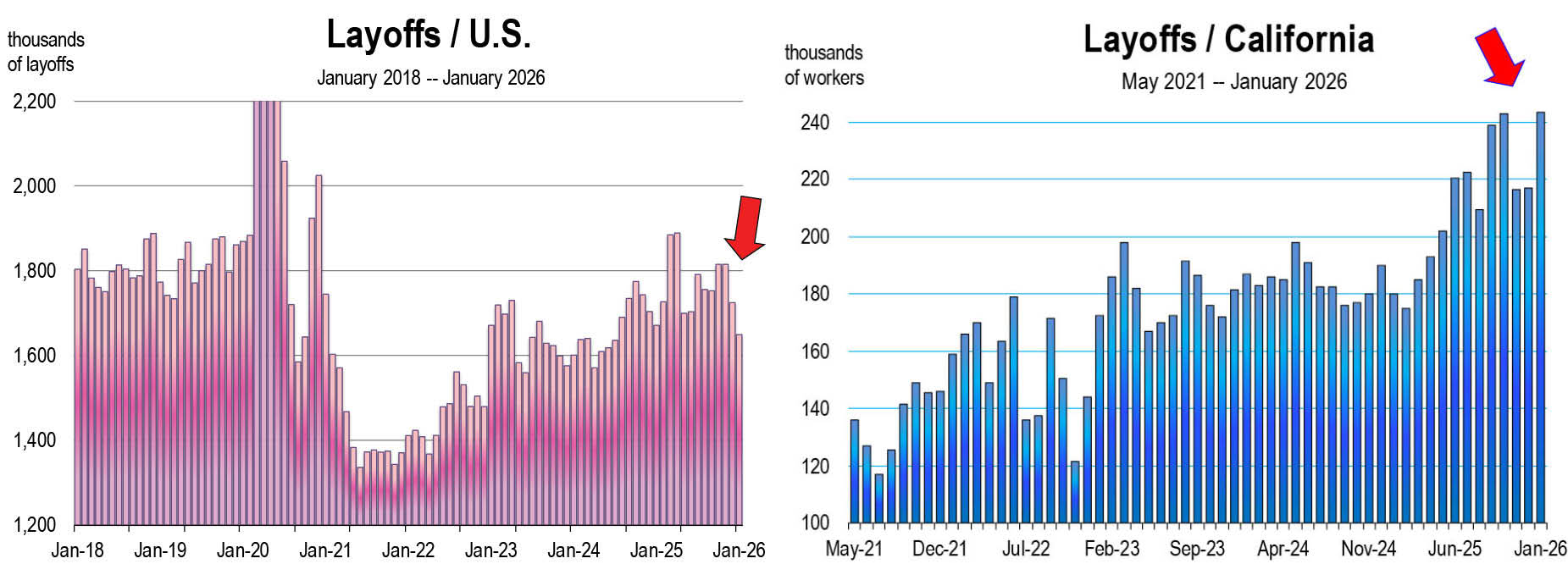

In 2025 the nation (and more severely so, California) experienced an expansion in growth with barely any job creation. So, in spite of the tariffs and weak labor markets, GDP rallied from the investment boom in Artificial Intelligence (AI). Economic growth would have been even more impressive had it not been for the 43-day government shutdown. According to the Bureau of Economic Analysis, this subtracted slightly more than a full percentage point from fourth quarter GDP growth.[1]

Here we are a year later and the new uncertainty of the season is the price of oil, inflation (again), the duration of the Israel-Iran war, and how all of these things together will upset domestic economic growth.

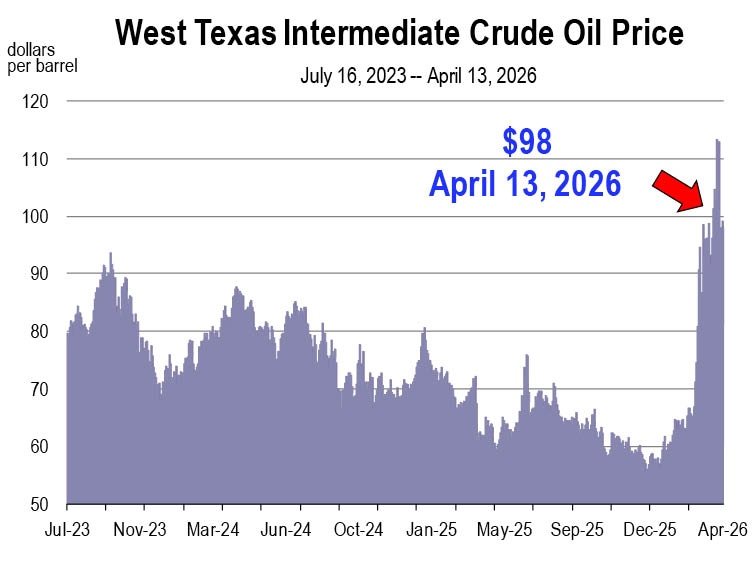

Oil prices have jumped $40 to $50 per barrel since early March, resulting in a $1.50 per gallon bump for gasoline in California. Higher gasoline prices are akin to a tax increase, especially for lower income groups. So, we are all paying a higher tax on gasoline due entirely to the war.

Also due to the war driving up oil prices, the stock market has experienced a 10 percent correction, and interest rates (especially in the 10-year treasury bond and mortgages) have moved noticeably higher. Economists see most of these movements as temporary and prices and rates will very likely revert back to pre-war levels once the Middle East conflict and Strait of Hormuz situation is resolved. No recession is forecast, but both inflation and unemployment rates will increase this year.

inflation and unemployment rates will increase this year.

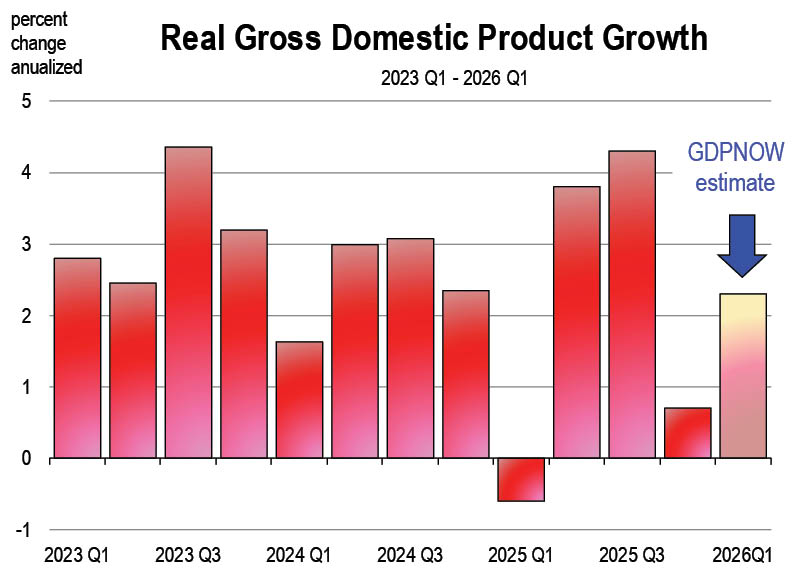

The first quarter estimate for GDP by the Atlanta Federal Reserve’s GDPNOW prediction has ranged from 2.3 to 1.3 percent over the last few weeks. A slowdown in consumer spending and business investment in late March and early April have pushed the estimate down to 1.3 percent.

Inflation

Last year we were correct regarding our skepticism about Tariffs causing higher rates of inflation. The U.S. economy remains predominantly domestically driven, with tariffs having a greater impact on trading partners than on the U.S. economy itself.

Capital markets were nervous at first but settled down. Inflation for the most part simply moved laterally through 2025. If anything, tariffs may have prevented inflation from going lower, but no clear indication on the price level could be detected as tariff-driven.

price level could be detected as tariff-driven.

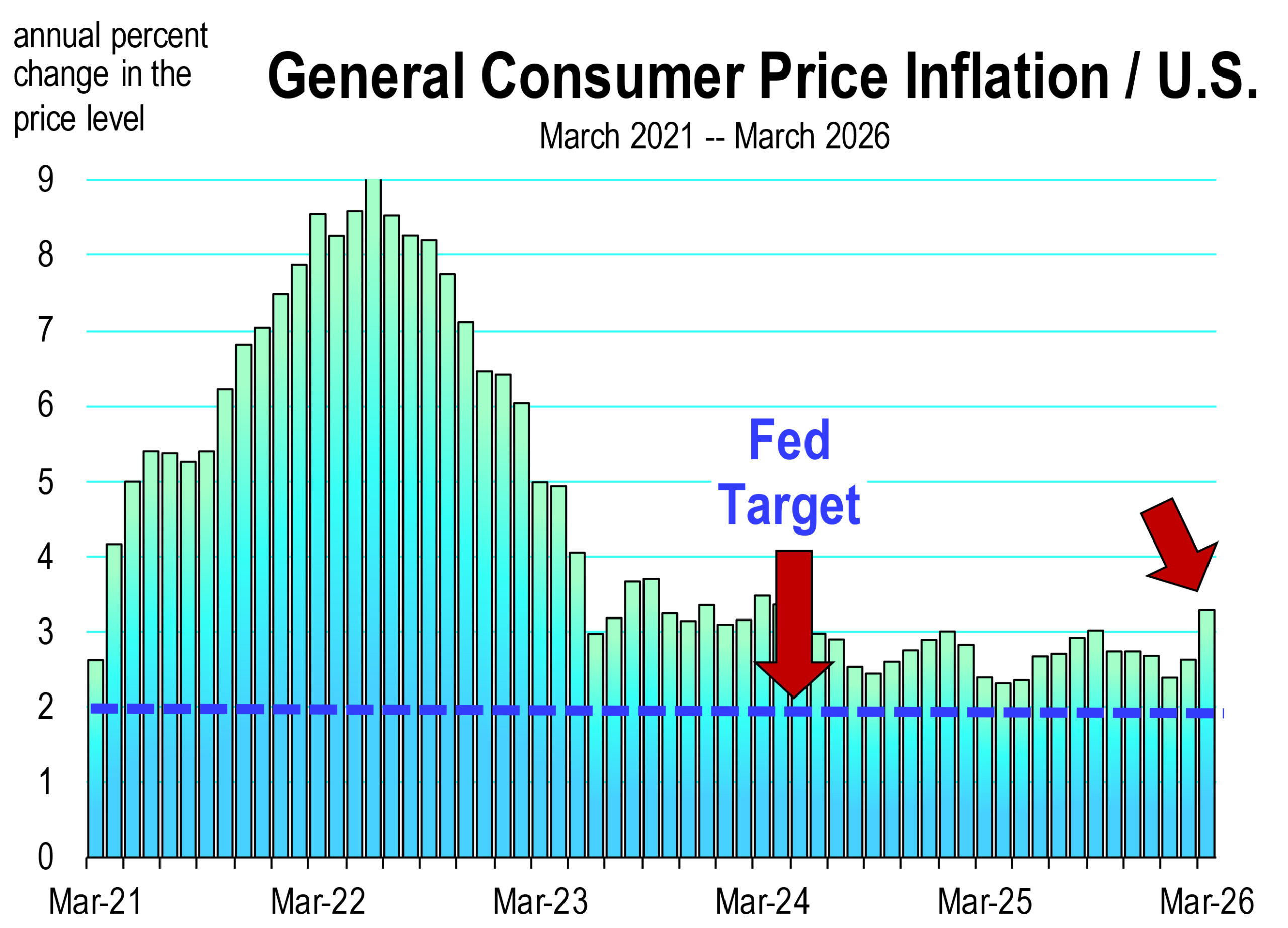

Nevertheless, inflation has missed the Fed’s 2.0 percent threshold for over five years. It was 2.4 percent in both January and February this year and was seemingly making progress toward reaching the target rate later in 2026.

But crude oil prices soared with the onset of the war in early March and have remained sharply higher into April. The effect of this has pushed the headline rate of inflation higher (to 3.3 percent), due principally to higher gasoline prices but indirectly through other prices now being raised by vendors to compensate for their higher fuel costs.

The longer that crude oil prices stay elevated, the longer it will take for gasoline prices to retreat and for pre-war levels of inflation to be restored. More fed cuts, that were anticipated before March, are likely off the table now until at least later in the summer. Inflation is going to remain sticky for awhile and movement toward the Fed target will be delayed further.

Interest Rates and Federal Debt

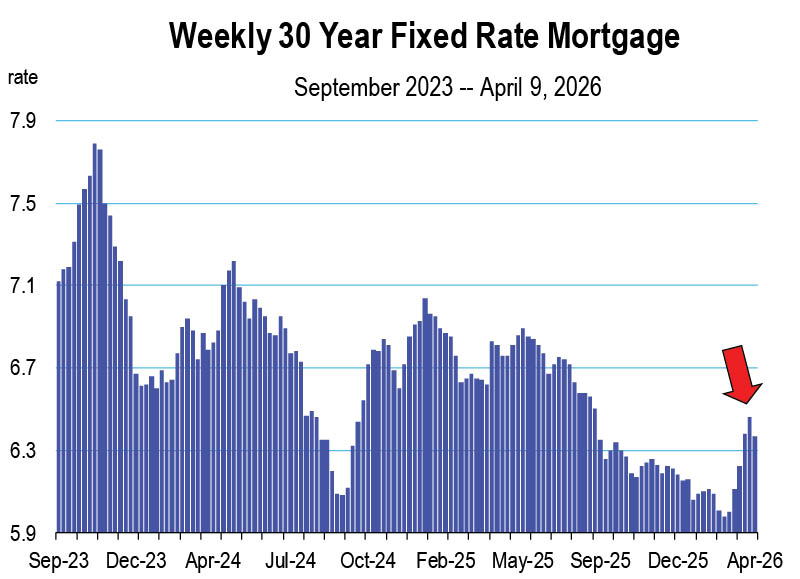

Interest rates rose sharply in March, in sync with oil prices. An inflationary environment does not favor the bond market where interest rates are determined. Consequently, the war is the first issue that needs to be resolved. Combined with lowering inflation, another big issue is the federal debt, which continues to rise. If Congress really wanted to make housing more affordable in this country, they would reduce federal spending so that a potential budget surplus could go toward debt reduction. That would make a meaningful difference in longer term rates, mortgage costs, and a buyer’s ability to purchase a home.

Many economic ills could be resolved with lower inflation, lower levels of debt, and avoiding wars that threaten oil prices, or any globally demanded natural resource.

The Trump administration has asserted that a temporary spike in gasoline prices is worth de-arming Iran of its ballistic missile and nuclear capability. While that may certainly be true, it is just as important, now that their capability has been “de-fanged,” to resolve the matter as fast as possible so that prolonged inflation can be avoided this year.

that their capability has been “de-fanged,” to resolve the matter as fast as possible so that prolonged inflation can be avoided this year.

Optimism Ahead ?

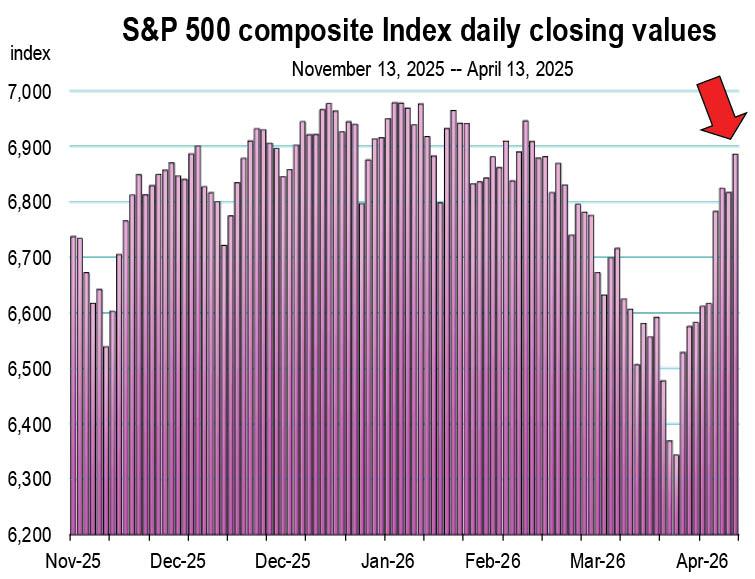

The aggregate effect of war, higher oil prices, possible prolonged inflation and even the mounting federal debt can be summarized by movements in the stock market. Currently, the broader market indices are rallying back and are now break even for the year-to-date. That is an encouraging sign for the current 2026 edition of economic uncertainty.

[1] Analysts using BEA data estimate that the shutdown subtracted roughly 1.15 percentage points from Q4 2025 annualized GDP growth, mainly via a 16.6 percent drop in federal spending. Without the shutdown, Q4 growth would have been around 2.5–2.6 percent instead of the reported 1.4 percent. See: https://www.federatedhermes.com/us/insights/article/government-shutdown-masks-solid-gdp-growth.do

The California Economic Forecast is an economic consulting firm that produces commentary and analysis on the U.S. and California economies. The firm specializes in economic forecasts and economic impact studies, and is available to make timely, compelling, informative and entertaining economic presentations to large or small groups.

![]()

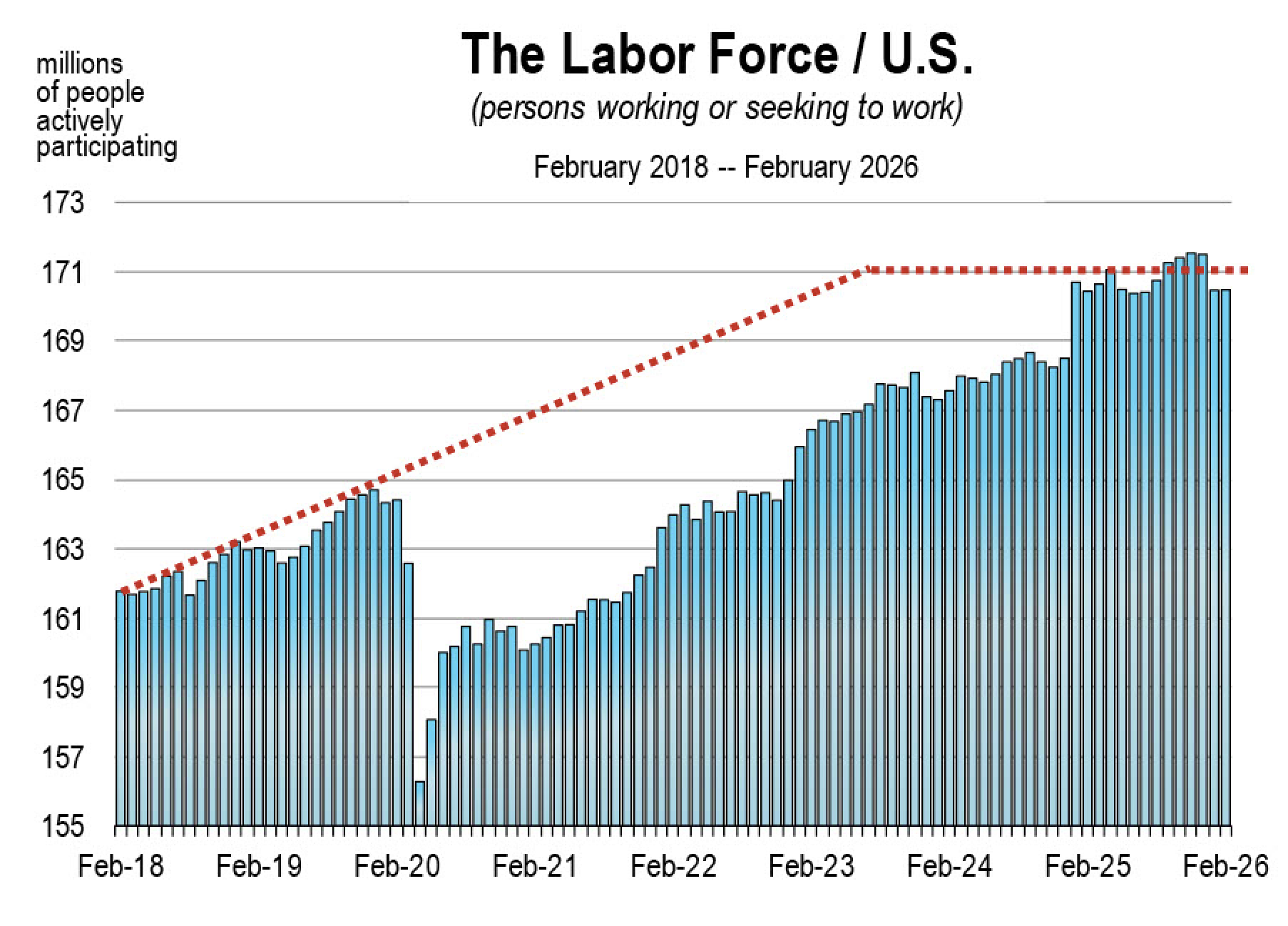

the unemployment rate has only ticked up 0.2 of a percentage point over this time period (to 4.4 percent), a negligible amount. Consequently, despite the lack of job creation, there is not much reported labor force misery. At least not yet.

the unemployment rate has only ticked up 0.2 of a percentage point over this time period (to 4.4 percent), a negligible amount. Consequently, despite the lack of job creation, there is not much reported labor force misery. At least not yet.

Deportations are subtracting from the labor force and limiting its growth. Housing remains a chronic constraint for

Deportations are subtracting from the labor force and limiting its growth. Housing remains a chronic constraint for

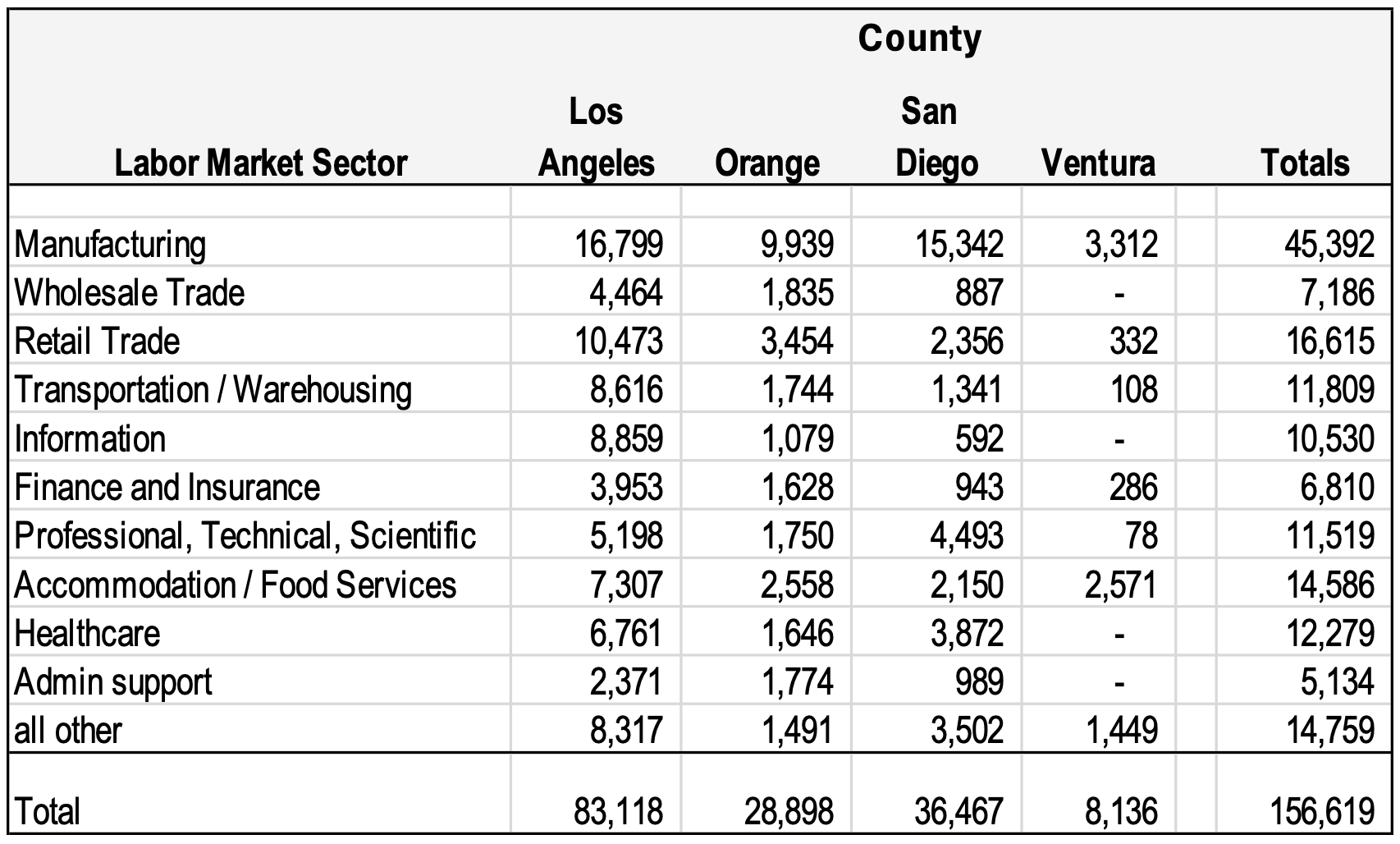

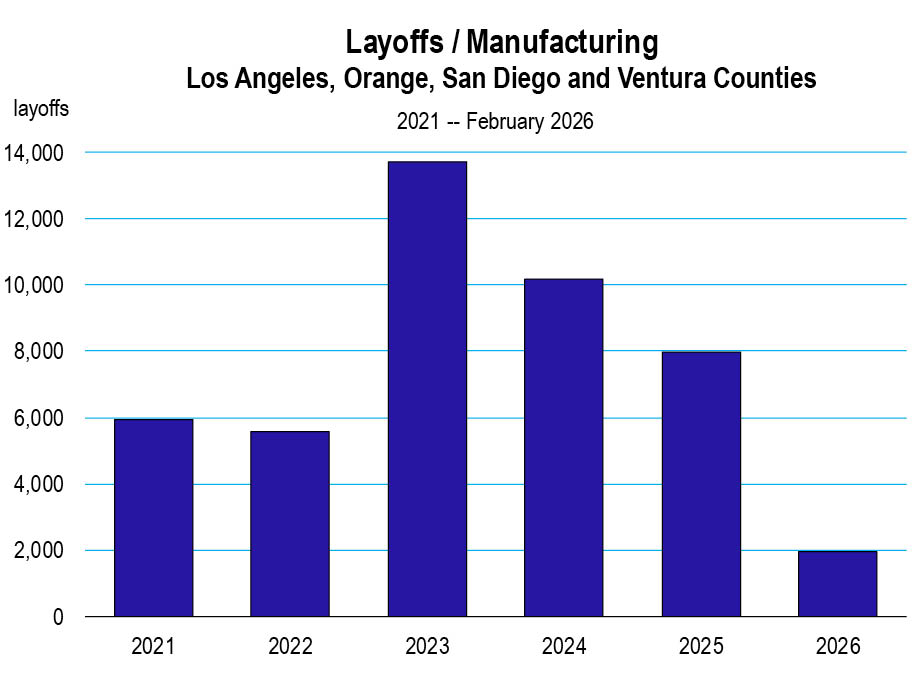

occur in other states. Nevertheless, California will realize some direct and spinoff effects of an expansion in domestic manufacturing activity especially in the advanced technology and defense products. This should result in new job creation by 2028.

occur in other states. Nevertheless, California will realize some direct and spinoff effects of an expansion in domestic manufacturing activity especially in the advanced technology and defense products. This should result in new job creation by 2028.

inflation, tariff uncertainty and aversion, geopolitical anomalies, and labor force availability.

inflation, tariff uncertainty and aversion, geopolitical anomalies, and labor force availability. has boosted productivity and output. This will likely continue in 2026 and over time but the path to those gains may be uneven. With business investment and household spending so dependent on confidence in the potential of AI to increase productivity and reduce costs, any setback could disrupt momentum and expose the underlying drag from tariffs, restrictions of immigration, and other policy changes, which would lower the economy’s potential in 2026.

has boosted productivity and output. This will likely continue in 2026 and over time but the path to those gains may be uneven. With business investment and household spending so dependent on confidence in the potential of AI to increase productivity and reduce costs, any setback could disrupt momentum and expose the underlying drag from tariffs, restrictions of immigration, and other policy changes, which would lower the economy’s potential in 2026. emerged. The “Hamburger Helper” indicator suggests more weakness in the economy than the forecast consensus. Sales of the product are up 15 percent over the last 12 months. Packaged complete meal products like this tend to increase when economic conditions deteriorate because of the savings they offer.

emerged. The “Hamburger Helper” indicator suggests more weakness in the economy than the forecast consensus. Sales of the product are up 15 percent over the last 12 months. Packaged complete meal products like this tend to increase when economic conditions deteriorate because of the savings they offer. through August is at the highest number since the pandemic.

through August is at the highest number since the pandemic. companies as adoption of AI systems in software development, computer board and component design, web development, data analytics, and advanced manufacturing products continues to evolve.

companies as adoption of AI systems in software development, computer board and component design, web development, data analytics, and advanced manufacturing products continues to evolve.

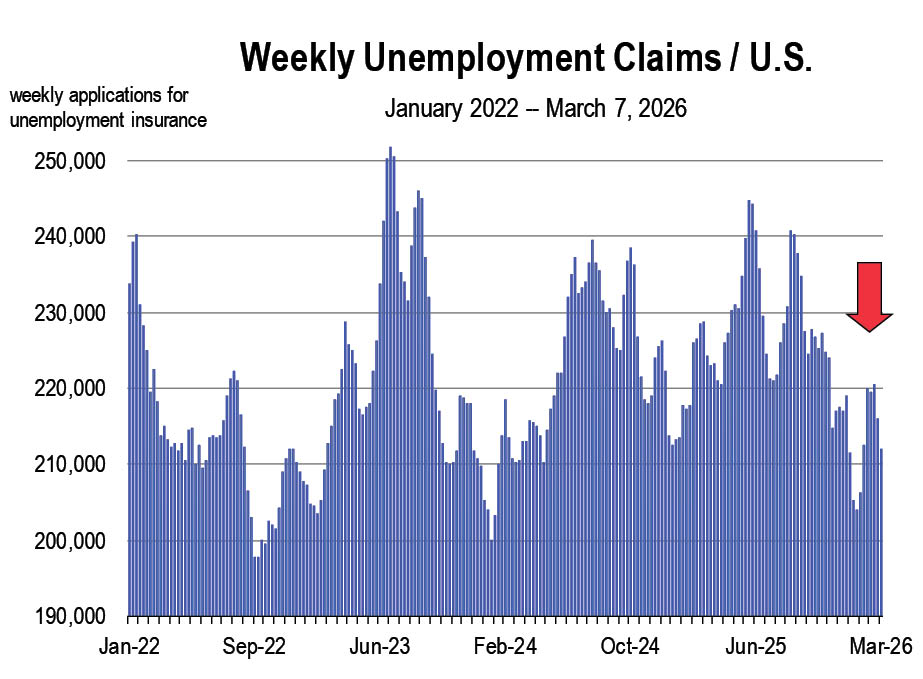

been minor, are the result of more people entering the labor force and outpacing the rate of job creation which remains positive.

been minor, are the result of more people entering the labor force and outpacing the rate of job creation which remains positive. there is still a moderate level of unfilled job openings, which have resulted in relatively high levels of wage growth. Deportations are contributing to this. Over the last year, nominal wages have grown at a rate averaging 4.3 percent, eclipsing inflation.

there is still a moderate level of unfilled job openings, which have resulted in relatively high levels of wage growth. Deportations are contributing to this. Over the last year, nominal wages have grown at a rate averaging 4.3 percent, eclipsing inflation. but still remain low by historical standards.

but still remain low by historical standards.

Inflation is still an issue for the economy. The CPI for June still shows a 2.7 percent inflation rate over the last year. Fortunately, the 2025 calendar year trend for CPI inflation is decidedly down, but we still face tariffed goods coming into the U.S. and especially as the holiday season ramps up. Consumers may substitute successfully enough to avoid tariff inflated priced goods but this circumstance remains a wait and see.

Inflation is still an issue for the economy. The CPI for June still shows a 2.7 percent inflation rate over the last year. Fortunately, the 2025 calendar year trend for CPI inflation is decidedly down, but we still face tariffed goods coming into the U.S. and especially as the holiday season ramps up. Consumers may substitute successfully enough to avoid tariff inflated priced goods but this circumstance remains a wait and see.

market.

market.

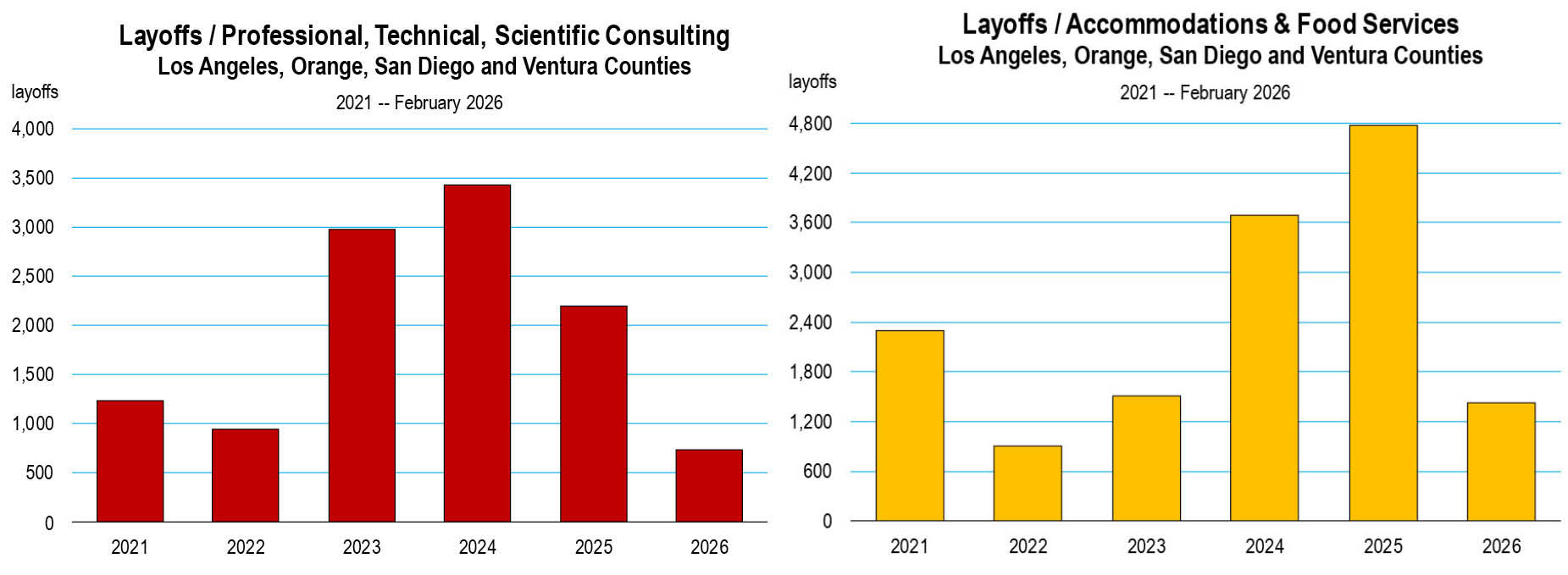

displace. Healthcare is the only private labor market that has consistently created jobs over the last 5 years. But even here, AI is now capable of replacing social workers, therapists, nursing assistants, and laboratory technicians. This will undoubtedly begin to reduce the rate of positive job growth that we’ve been observing in California healthcare since 2020.

displace. Healthcare is the only private labor market that has consistently created jobs over the last 5 years. But even here, AI is now capable of replacing social workers, therapists, nursing assistants, and laboratory technicians. This will undoubtedly begin to reduce the rate of positive job growth that we’ve been observing in California healthcare since 2020.