By Mark Schniepp

June 2016

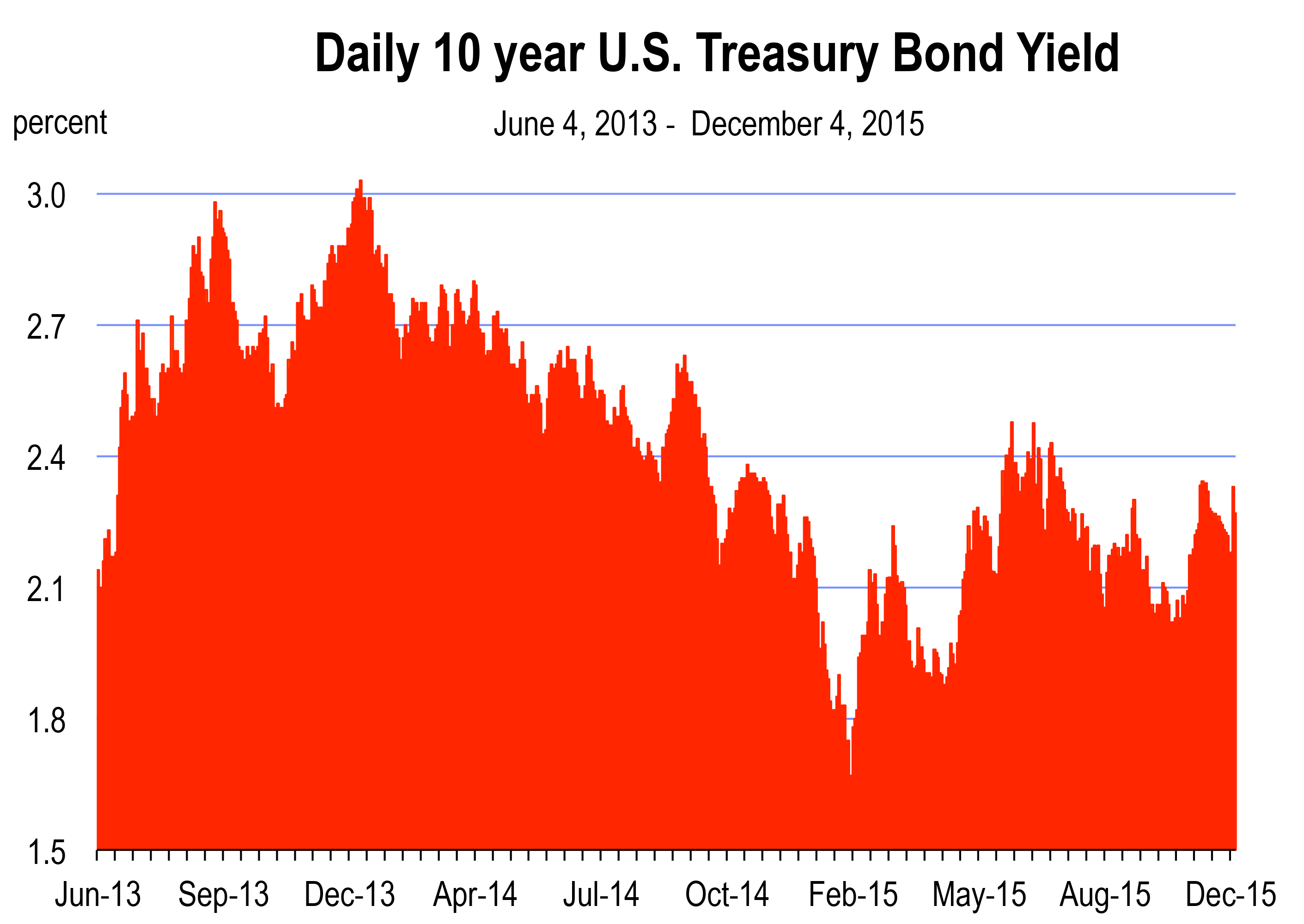

Interest Rates

They were supposed to go higher in 2016—not sharply higher but noticeably higher nonetheless.

They were supposed to go higher in 2016—not sharply higher but noticeably higher nonetheless.

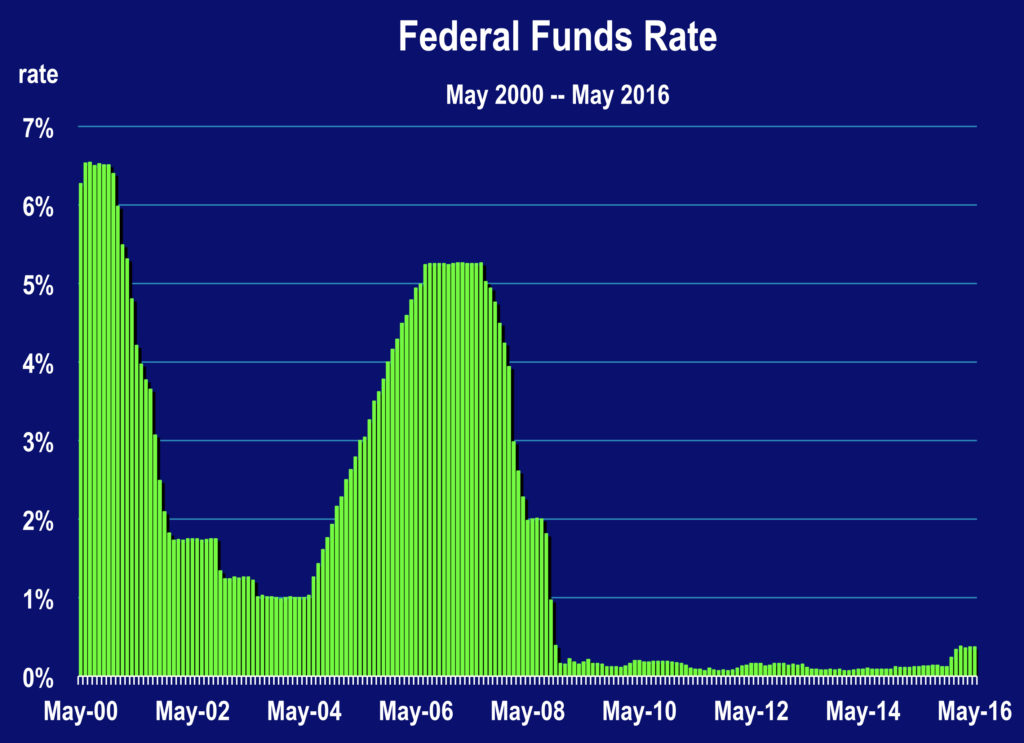

As you may recall, the Fed raised the federal funds and discount rates last December. This was the first such lift in rates since 2006. The conventional wisdom based on their remarks was that rates would be raised in a gradual fashion throughout 2016 and 2017.

But worries about the slowdown in China spooked the stock market at the beginning of the year and the Dow tumbled 1,900 points during the first 3 weeks of January. The U.S. manufacturing sector was sliding and durable goods orders were shaky. So the Fed held off raising rates in March. It’s now June and they meet on the 15th. Another rate hike is now called for but wait, the employment report for May that just came out last Friday was a huge downer. Is that going to dash (postpone) another opportunity to push rates higher?

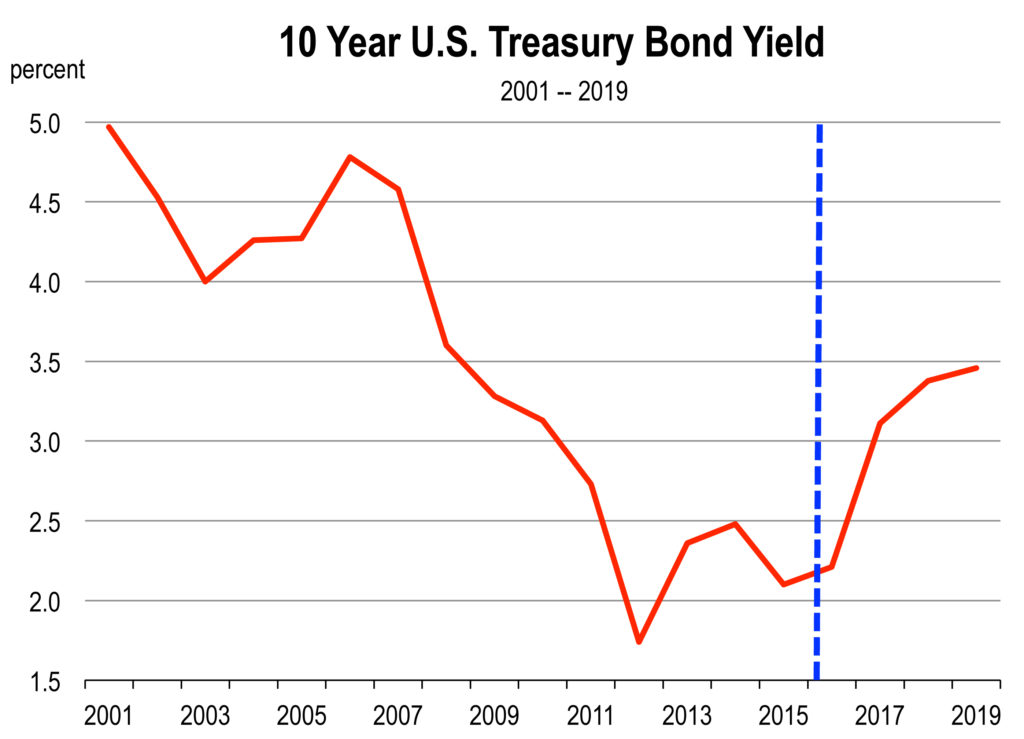

Perhaps…. or perhaps not. With the 10 year Treasury Bond yield falling to 1.64 percent on June 10, just a few days before the Fed meets, bond traders certainly don’t think the Fed will make another move. And one of the continued reasons cited is that as we get closer to the election this year, policy moves by the Fed will be interpreted as political, and I think they’d like to avoid that. But next week is far enough away from November and that’s why it’s a good option.

The Actual Rate Hike Itself Doesn’t Matter but Rates Need to be Raised

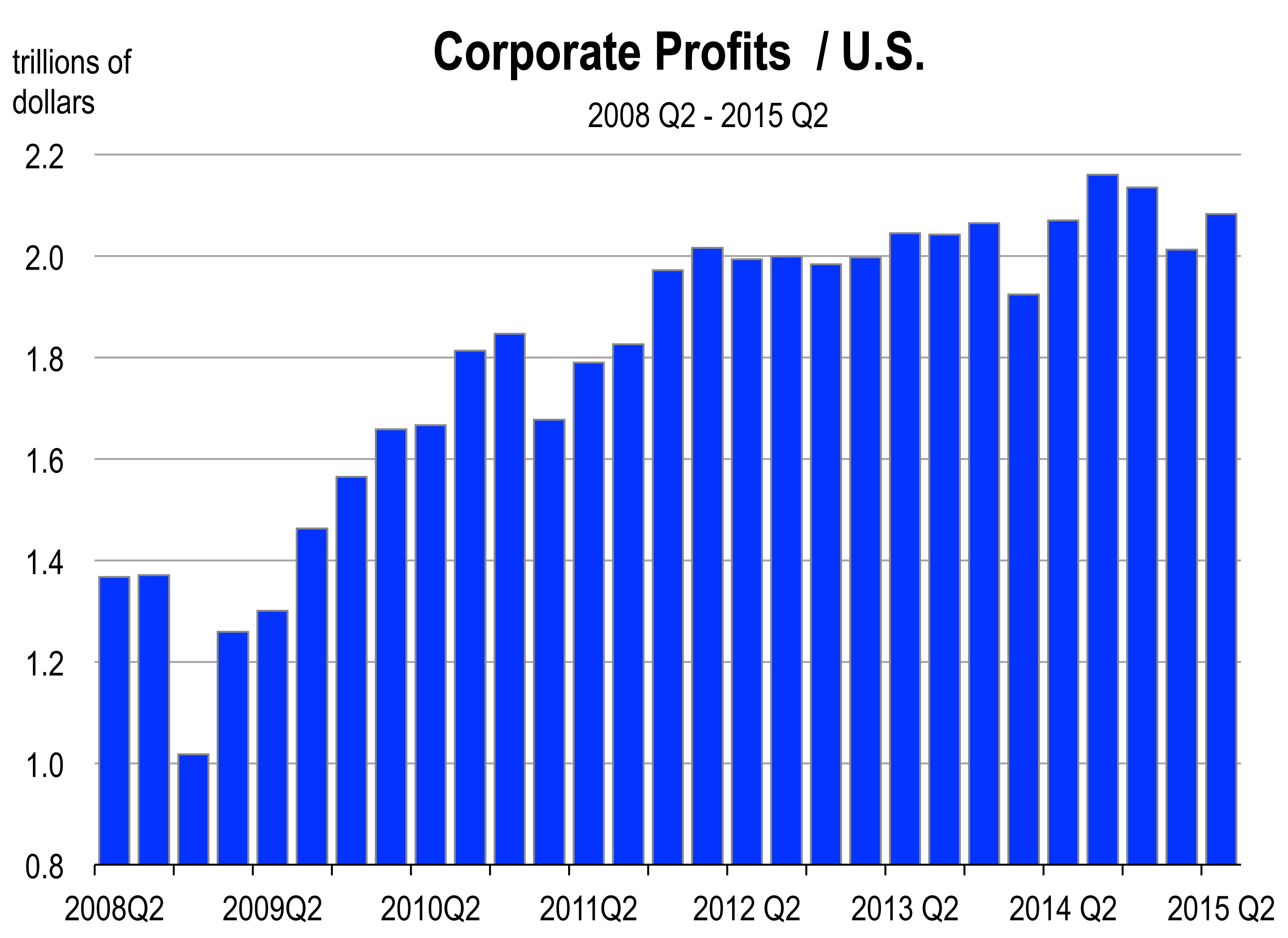

But it really doesn’t matter because another ¼ point hike in rates won’t impact much of anything. As the Fed has announced, a quarter point increase would be negligible but is a sensible first step to ensure the Fed stays ahead of inflation. Inflation remains on the radar screen and the Fed risks roiling world markets and pushing up the value of the dollar.

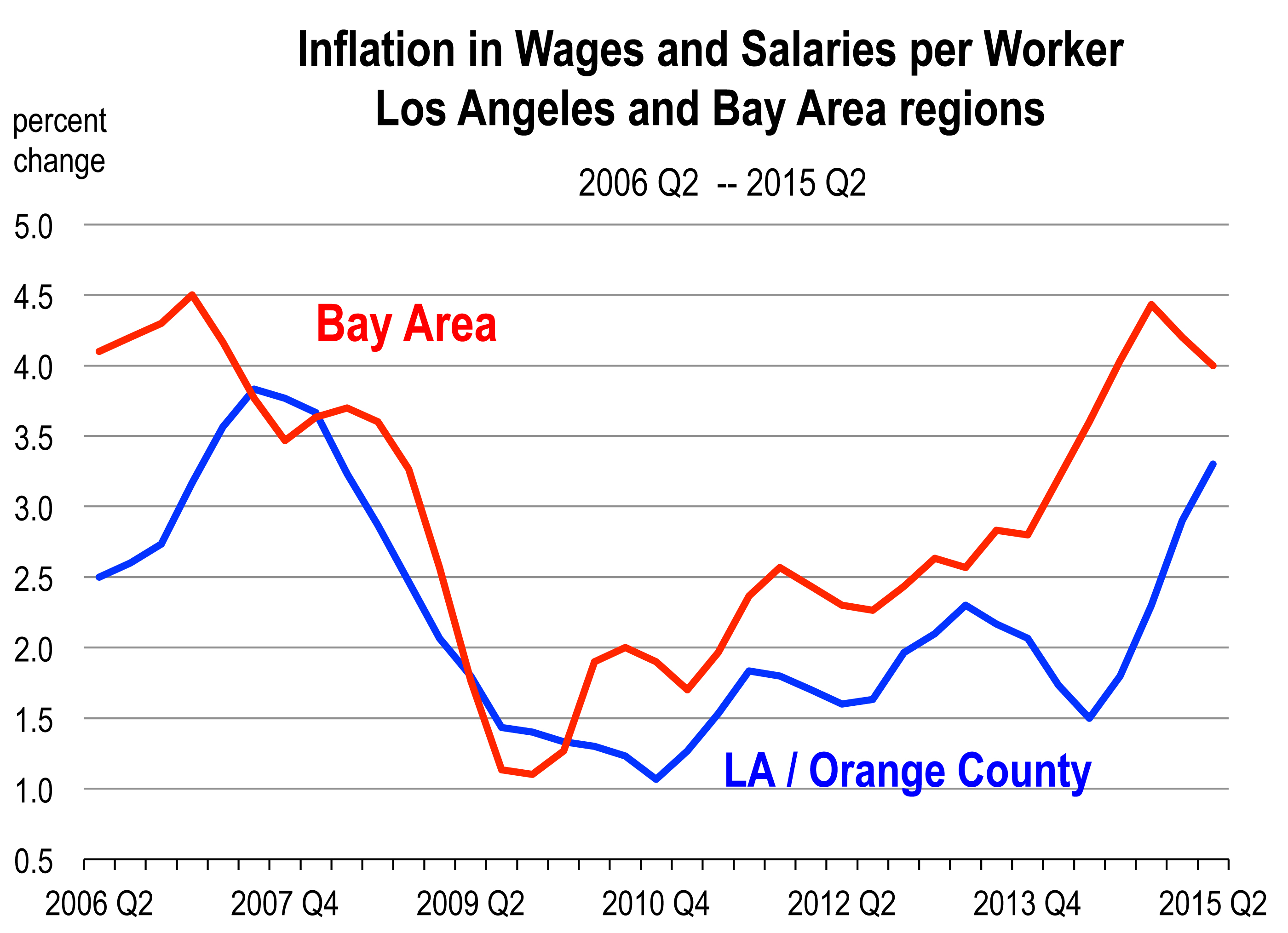

With the economy on the verge of full employment, there is growing evidence of wage and salary inflation, and that will translate into higher general price inflation than what we observe today.

With the economy on the verge of full employment, there is growing evidence of wage and salary inflation, and that will translate into higher general price inflation than what we observe today.

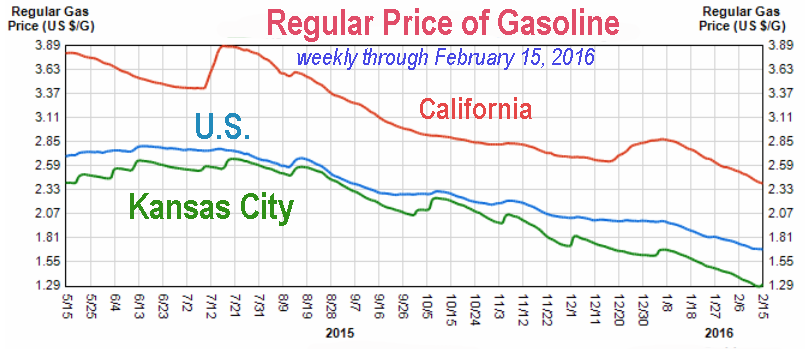

With oil prices rising again, you probably are noticing slightly higher gasoline prices every week. There’s also a likelihood that your healthcare premiums will rise this year or next. And housing costs are clearly moving higher, for home buyers and for renters.

Higher expected inflation should push all market rates higher this year, unless those expectations are dashed because of offsets, such as a slower growing economy either here or abroad from our dominant trading partners.

Our forecast of inflation for 2016 is higher, and higher still in 2017. All the more reason why rate hikes are necessary, let alone warranted. The uncertain outlook for global growth should not stand in the way of the Fed resuming its path toward normalization of rates next week.

What is the Forecast for Rates Over the Next 18 Months?

Our forecast 18 months ago was for much higher rates today. But Europe got in the way, and then China. Now it’s the employment report, the presidential election, or whatever….

We are still sticking to a higher forecast of rates because the Fed wants to raise rates, the Fed needs to raise rates, and the market will push rates higher as inflation becomes more apparent.

____________________________________________________________________________________

Upcoming Event

Entrepreneur Economic Forecast Conference / Los Angeles and Ventura Counties

September 8, 2016

Westlake Hyatt

7:30 am to 10:45 am

Speaker topics will include:

How long can the current expansion last?

What about interest rates and inflation?

The 2016 El Nino fizzled; can we tolerate another year of drought?

What are the recession risks going into 2017?

Is Ventura County still lagging its peers?

Has commercial real estate peaked?

Online registration will be available July 1st

The California Economic Forecast is an economic consulting firm that produces commentary and analysis on the U.S. and California economies. The firm specializes in economic forecasts and economic impact studies, and is available to make timely, compelling, informative and entertaining economic presentations to large or small groups.

![]()

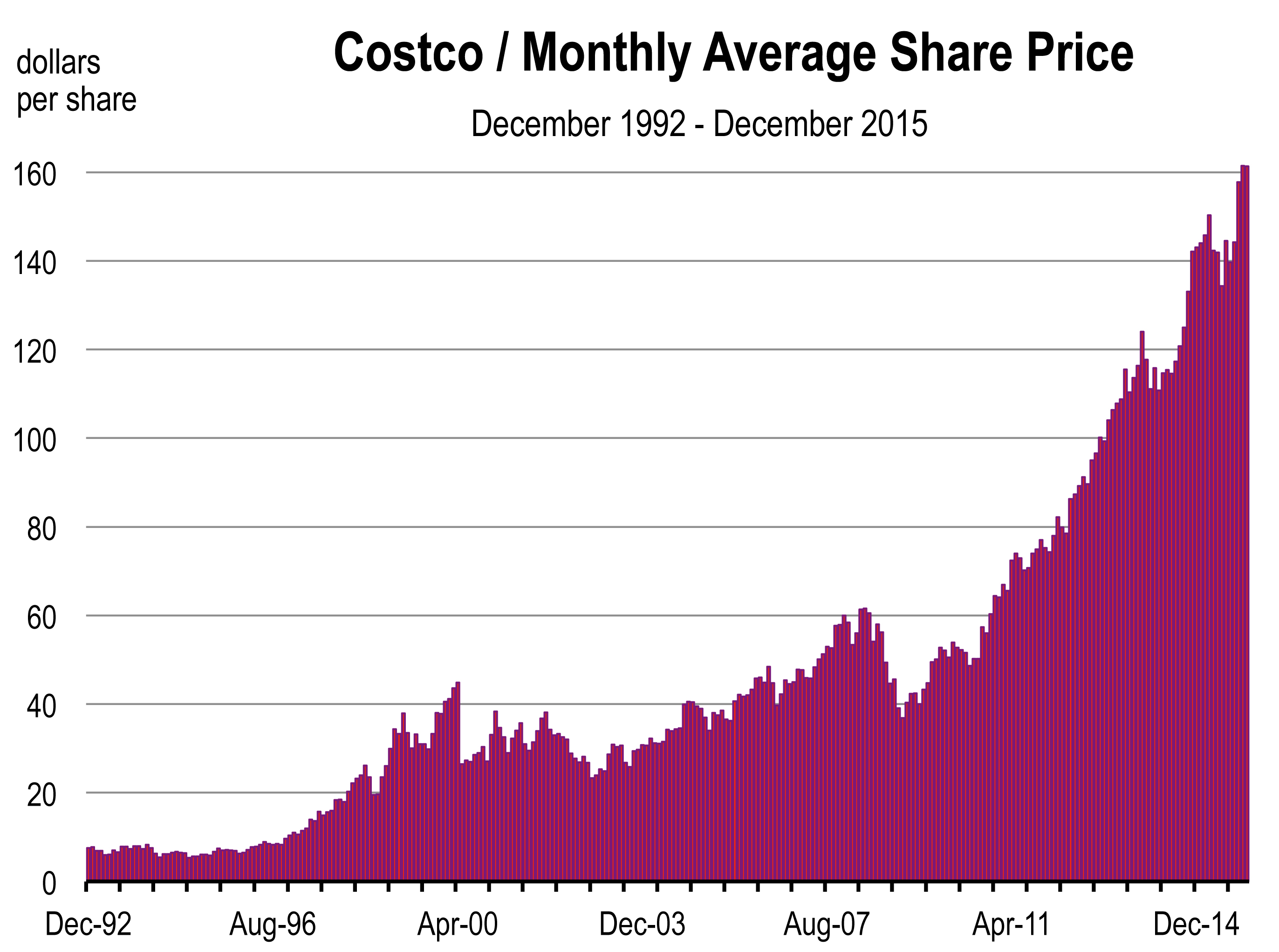

Home prices continue to rise this year, especially in the California coastal markets. Home sales are running at a similar pace as last year—not too hot and not too cold.

Home prices continue to rise this year, especially in the California coastal markets. Home sales are running at a similar pace as last year—not too hot and not too cold. I have addressed the Millennials many times in these monthly reports. But let me reiterate what we are seeing or not seeing regarding them and the housing market:

I have addressed the Millennials many times in these monthly reports. But let me reiterate what we are seeing or not seeing regarding them and the housing market:

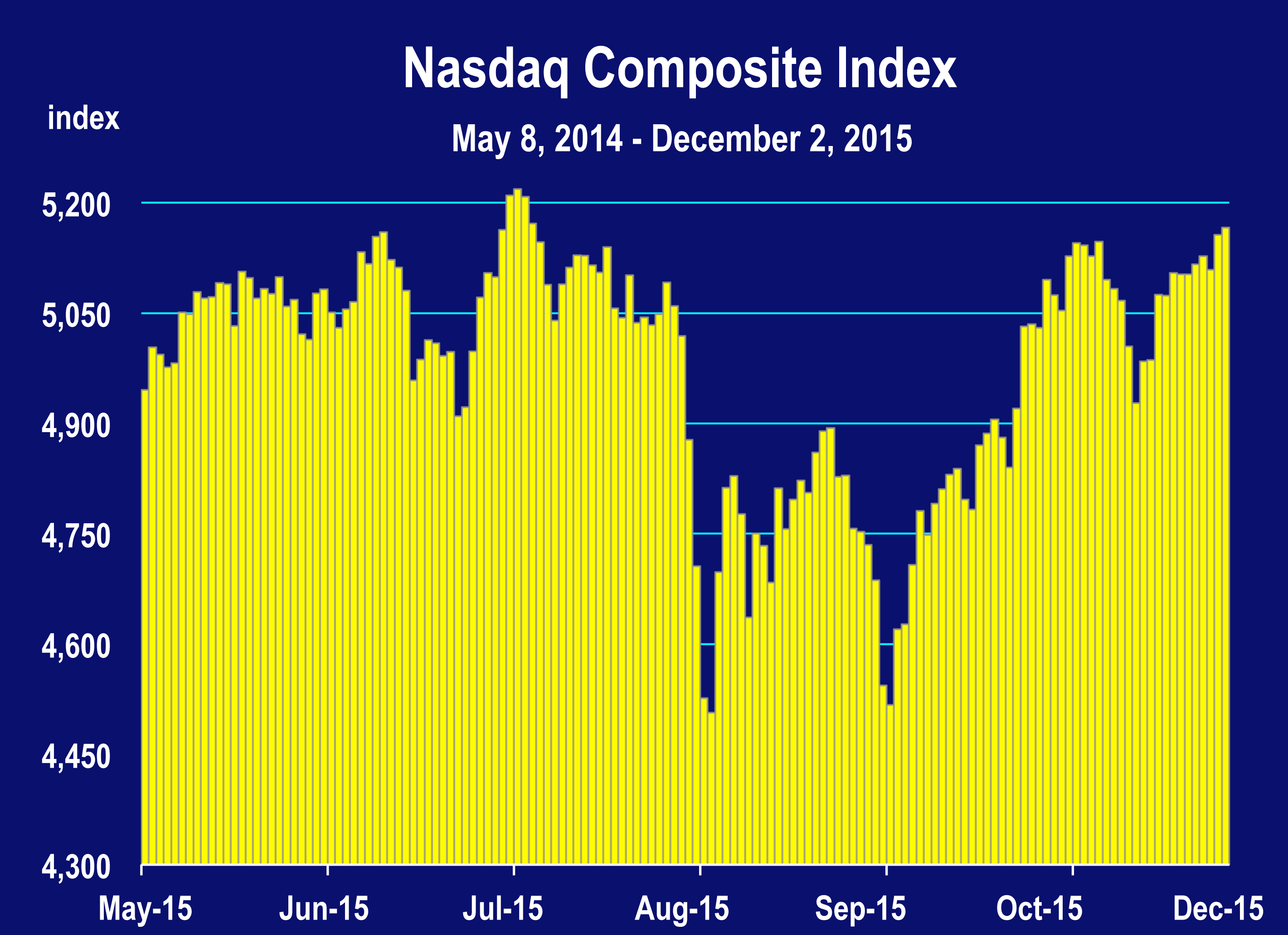

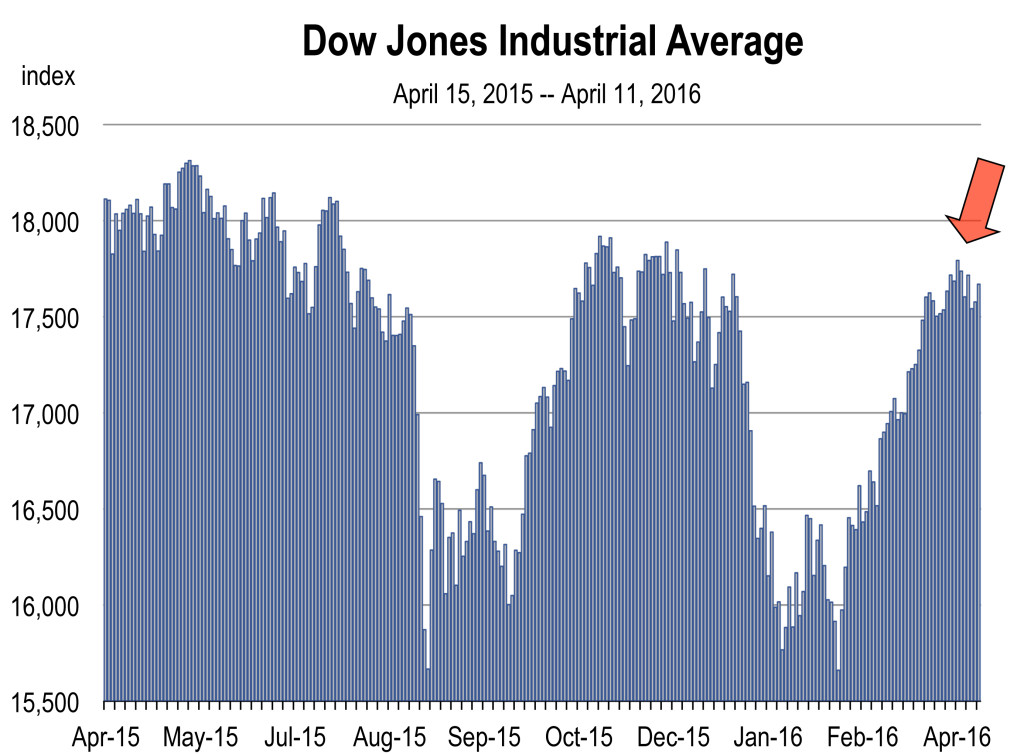

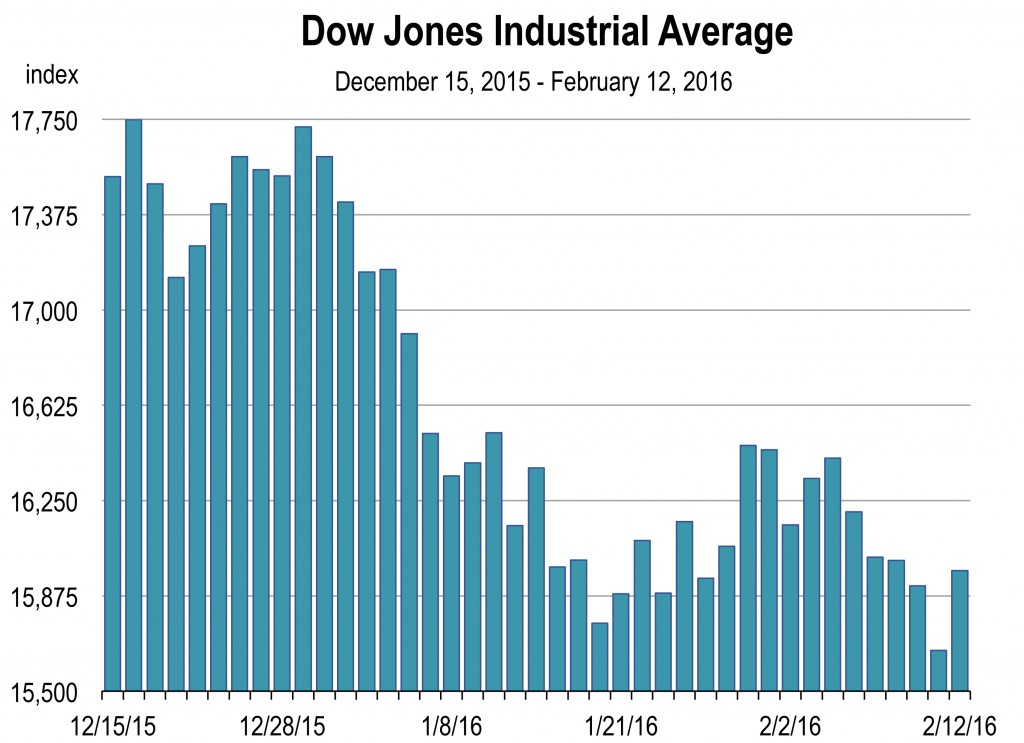

The Stock Market is Grinding its Way Back

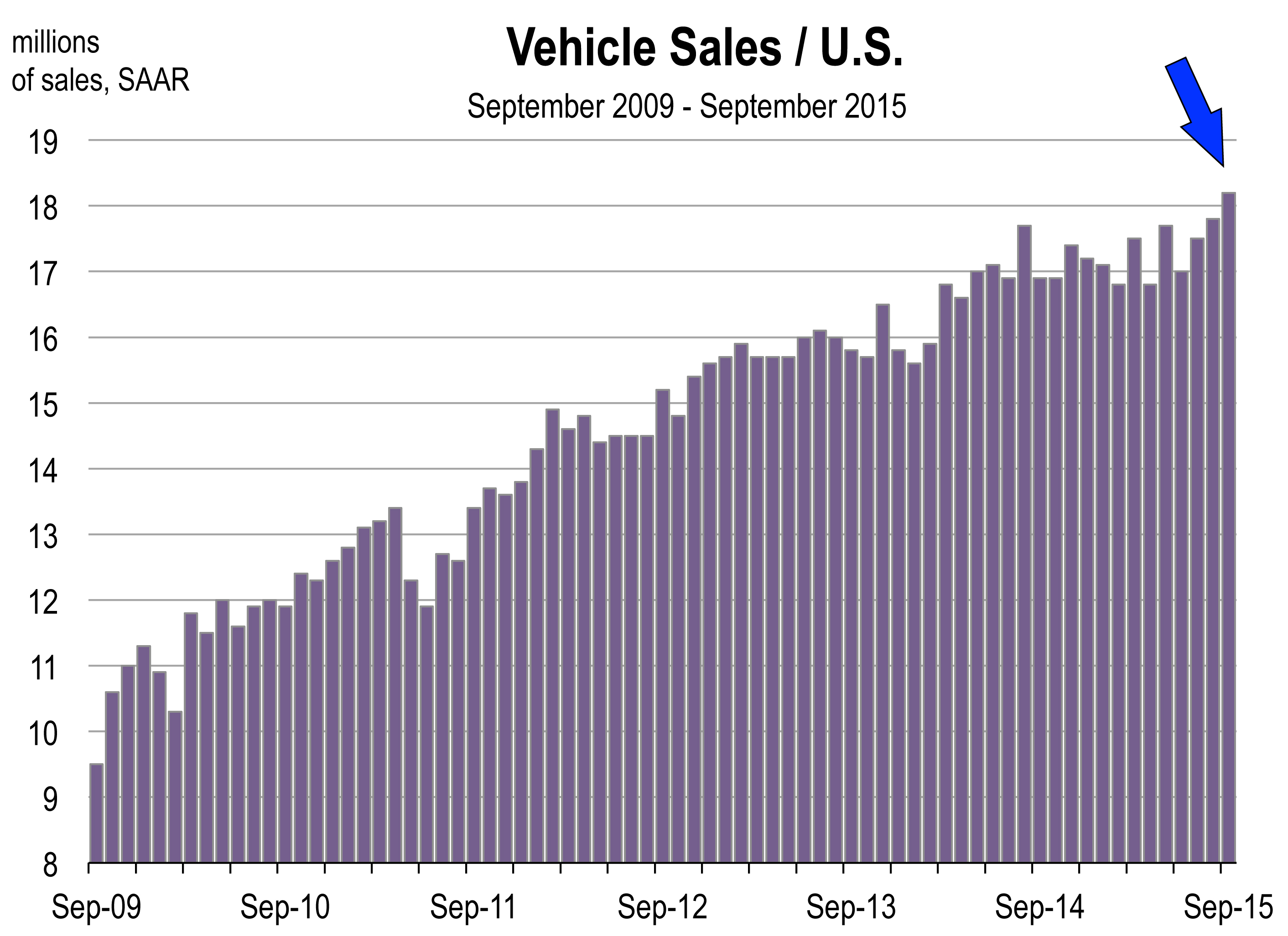

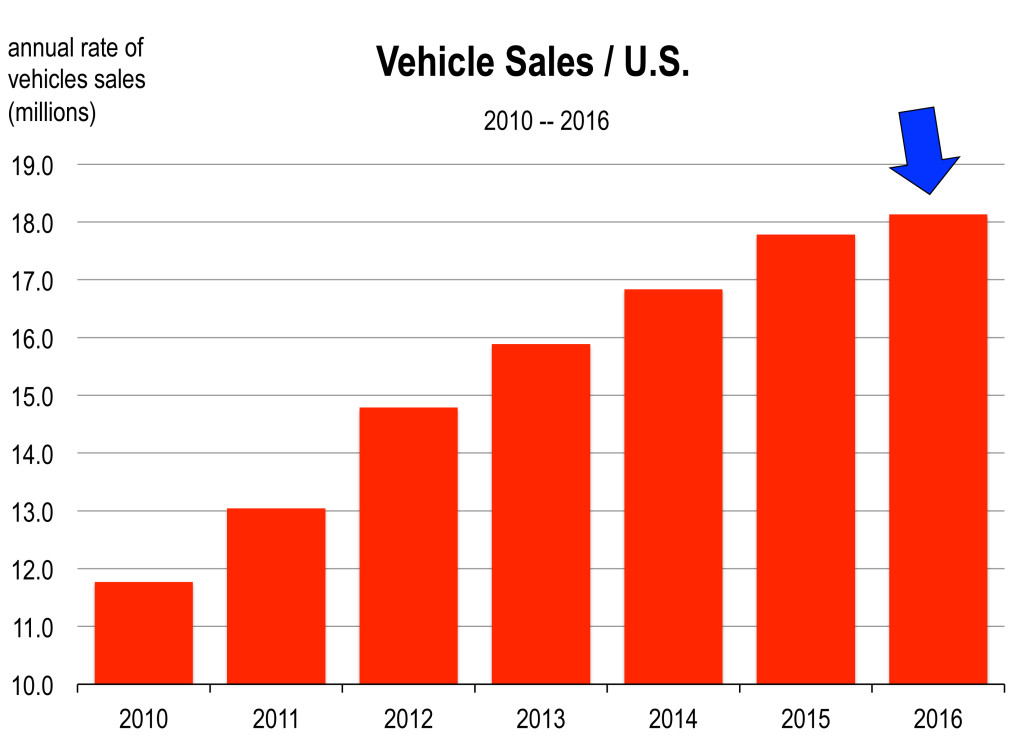

The Stock Market is Grinding its Way Back Americans are buying more cars at a near record pace. There are more vehicles on the road than ever before and traffic remains tough. The seasonally adjusted annualized pace of 17.5 million units in February was the strongest in 15 years. All the gains over the past year have been in the light truck segment thanks to persistently low gasoline prices.

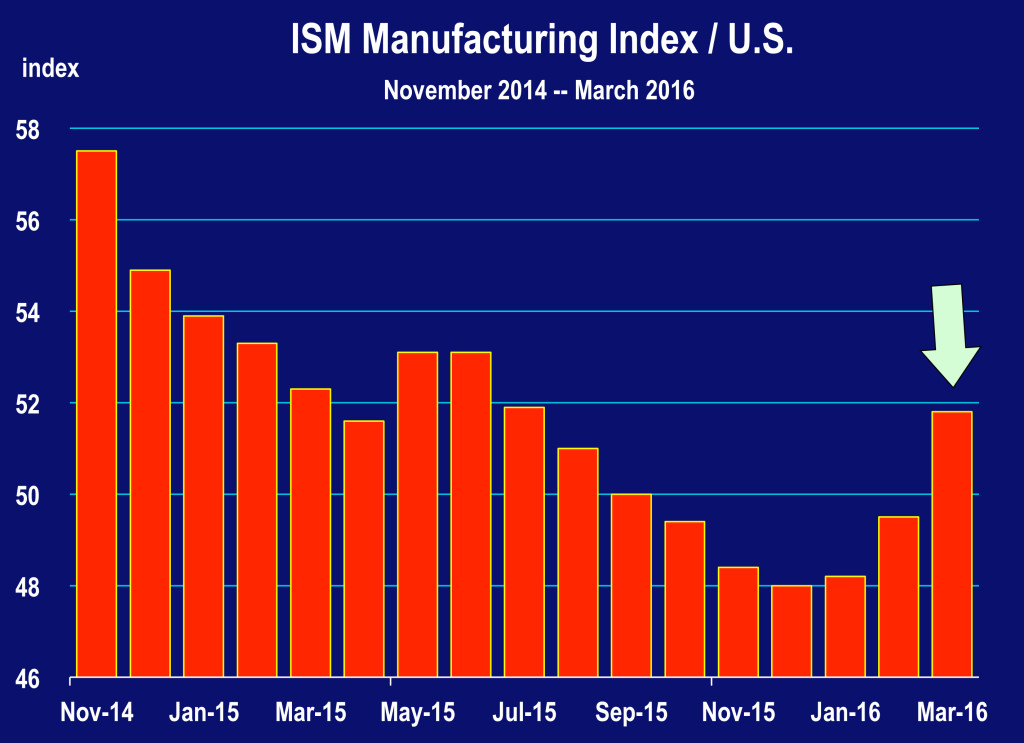

Americans are buying more cars at a near record pace. There are more vehicles on the road than ever before and traffic remains tough. The seasonally adjusted annualized pace of 17.5 million units in February was the strongest in 15 years. All the gains over the past year have been in the light truck segment thanks to persistently low gasoline prices. Manufacturing Rising Again

Manufacturing Rising Again A higher stock market leads to more spending by consumers because of the wealth effect. Retail sales, which have been dragged lower in recent months by falling gasoline prices, should move higher going forward, especially as the U.S. economy approaches full employment and average earnings move higher.

A higher stock market leads to more spending by consumers because of the wealth effect. Retail sales, which have been dragged lower in recent months by falling gasoline prices, should move higher going forward, especially as the U.S. economy approaches full employment and average earnings move higher. An exodus of big employers. Almost every business and government agency that remains in the controlled region struggles with recruiting and retaining workers who cannot afford to live nearby. Firms end up defecting from the region or downsizing and opening operations in uncontrolled areas where access to a larger labor force (and more available and affordable housing) is less challenging.

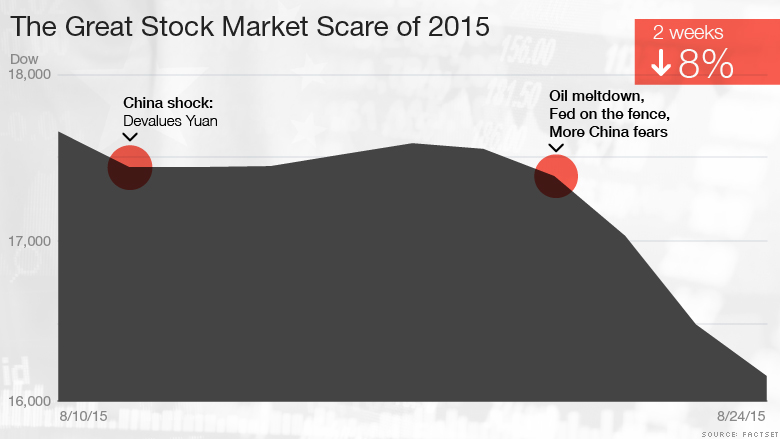

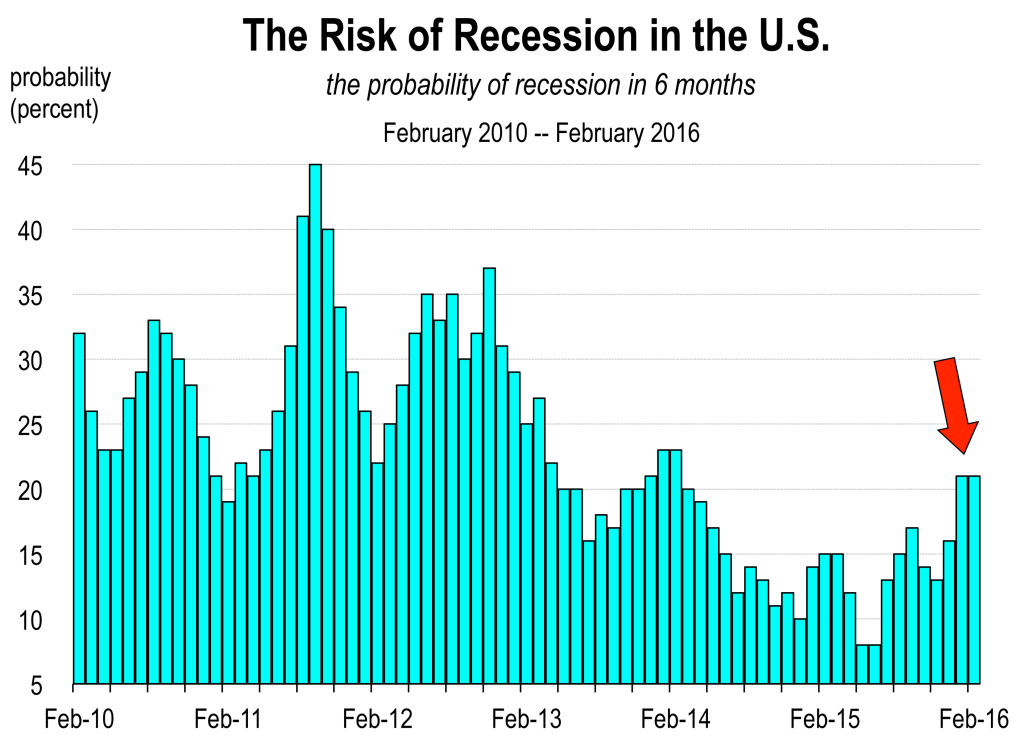

An exodus of big employers. Almost every business and government agency that remains in the controlled region struggles with recruiting and retaining workers who cannot afford to live nearby. Firms end up defecting from the region or downsizing and opening operations in uncontrolled areas where access to a larger labor force (and more available and affordable housing) is less challenging. OK, the market is now down 10 percent from where it stood at the turn of the year. This is a repeat of what happened in August. Why? Is this the early warning signs of the next recession?

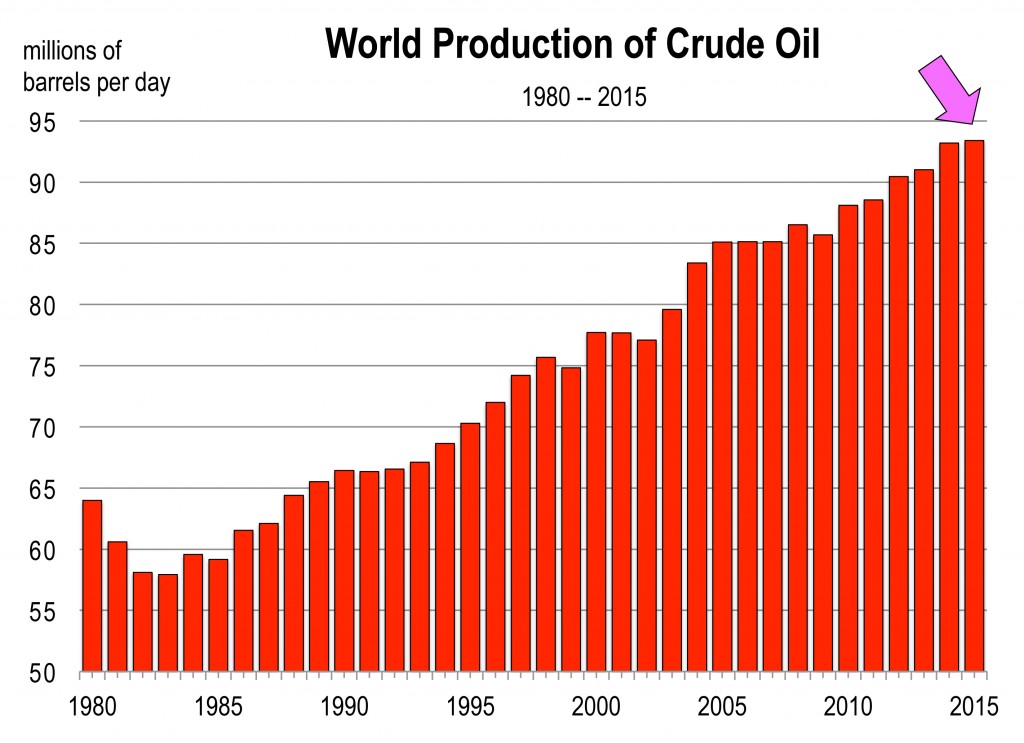

OK, the market is now down 10 percent from where it stood at the turn of the year. This is a repeat of what happened in August. Why? Is this the early warning signs of the next recession? The oil price collapse is due simply to increased supply (mostly by the U.S.) and decreased demand forces. Demand for oil globally began tapering off, driven most importantly by a slowdown in China’s economy. Until 2010, China had maintained an average growth rate of more than 10 percent annually for over 30 years. This high growth scenario started to slow in 2010. Currently (2016) the current GDP growth target set out by Chinese authorities is 7 percent, and many have questioned how much further growth could slow in the second largest economy in the world.

The oil price collapse is due simply to increased supply (mostly by the U.S.) and decreased demand forces. Demand for oil globally began tapering off, driven most importantly by a slowdown in China’s economy. Until 2010, China had maintained an average growth rate of more than 10 percent annually for over 30 years. This high growth scenario started to slow in 2010. Currently (2016) the current GDP growth target set out by Chinese authorities is 7 percent, and many have questioned how much further growth could slow in the second largest economy in the world.

The Chinese stock market is now in a bear market for the second time in 7 months. And U.S. investors are interpreting China’s problems as poison for the U.S. Why?

The Chinese stock market is now in a bear market for the second time in 7 months. And U.S. investors are interpreting China’s problems as poison for the U.S. Why? Source: LA Times, December 27, 2015, page C1

Source: LA Times, December 27, 2015, page C1 Source:

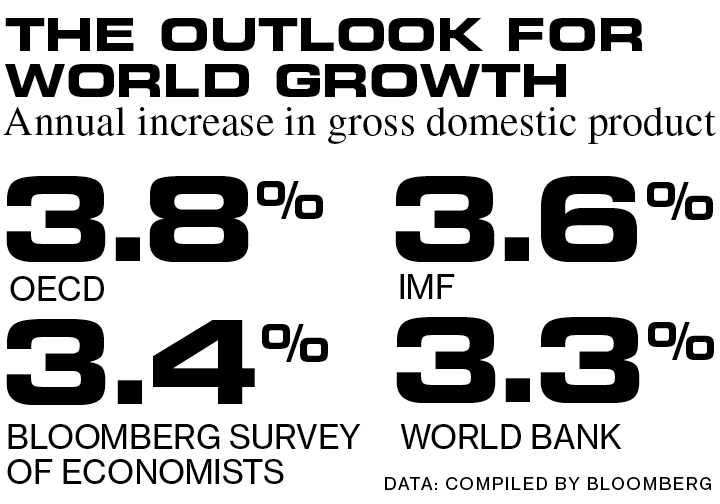

Source:  Source: Economist Intelligence Unit, The Economist, December 30, 2015

Source: Economist Intelligence Unit, The Economist, December 30, 2015