Mark Schniepp

October 2024

The Immigration Surge

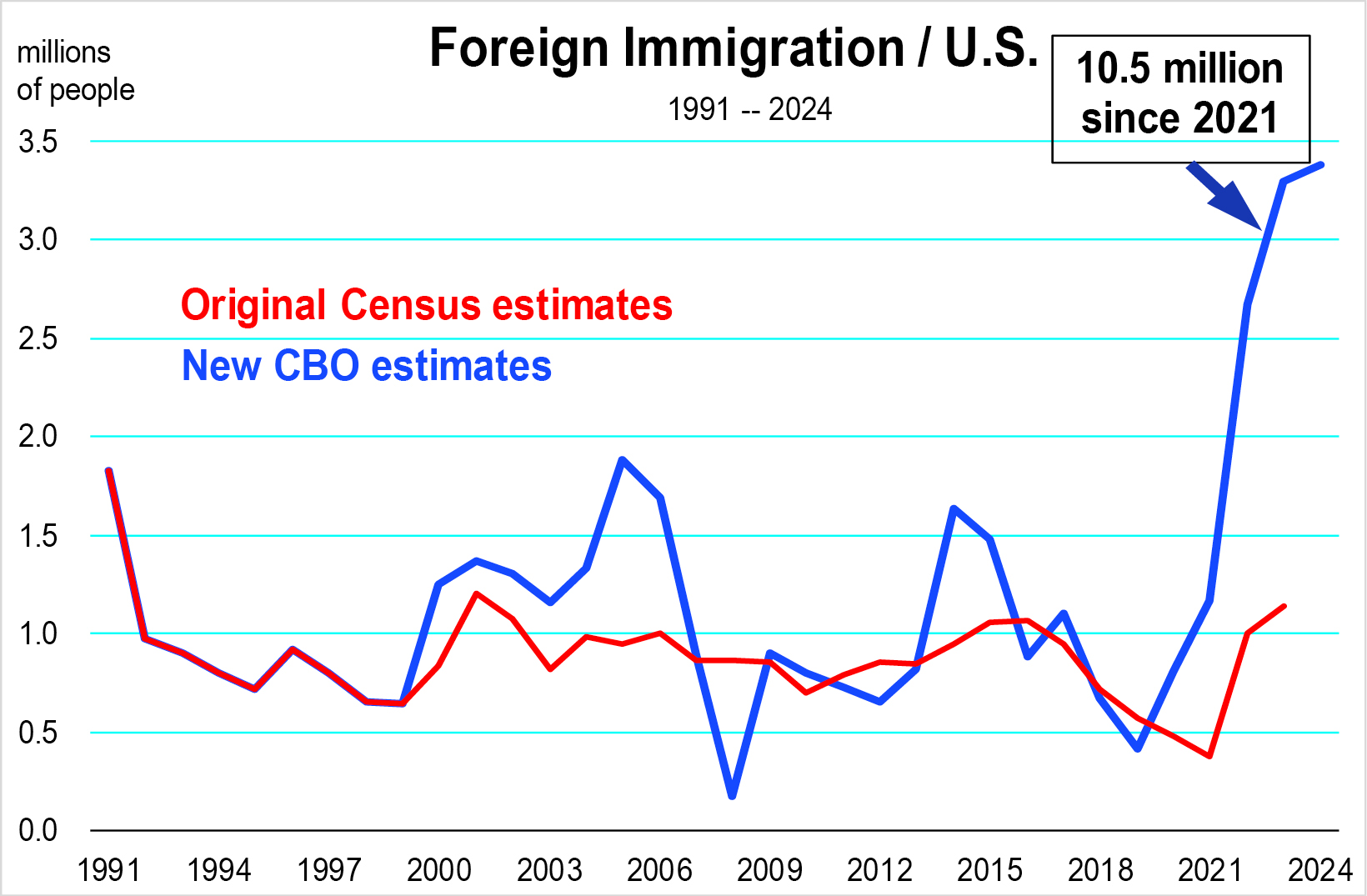

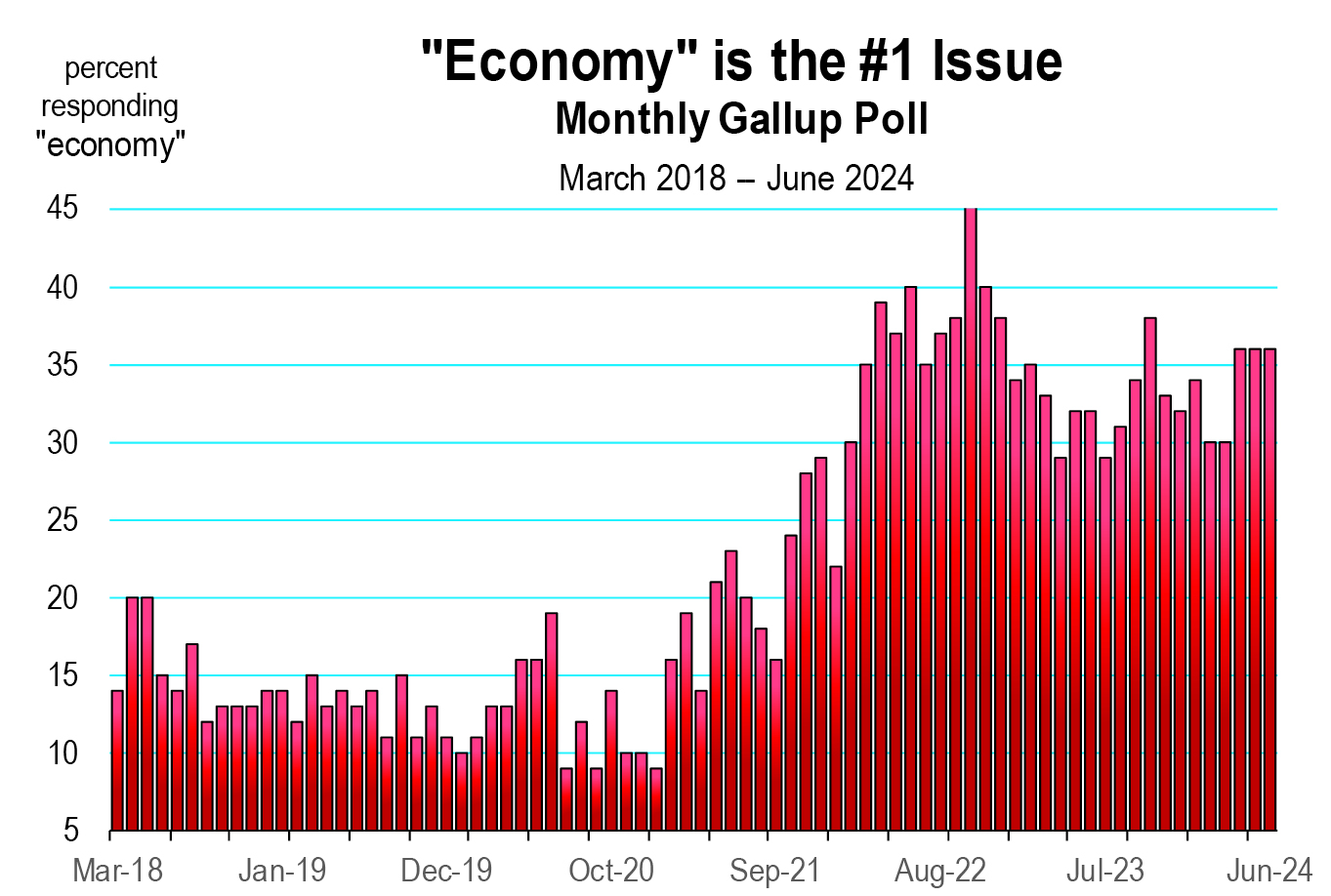

The immigration issue has now jumped to the most important problem cited by Americans, surpassing inflation and the general economy.[1] If you’ve watched any TV in the last 2 years, you’ve seen hordes of people from all over the world massed at southern border ports of entry.

The volume of immigrants coming through these ports of entry was originally dismissed simply as pent-up immigration from pandemic closed borders. The official Census record did not report much change in the flow of immigration over the last 3 years. However, in January of this year, the Congressional Budget Office reported revised numbers of immigrants for calendar years 2021, 2022, and 2023. The total is 7.1 million. The current estimate for 2024 will be lower than 2023 at 2.8 million “encounters” that will bring total 2021 to 2024 immigration to 10 million.[2] The revised numbers which represent an immigration surge is the largest volume of immigrants per year in the history of the U.S.

And this does not include the 530,000 immigrants that have flown into the U.S. since January 2023 as part of the Cuban-Haitian-Nicaraguan Parole Process, a program where DHS receives immigrants on charter flights from these three countries into 50 different international airport destinations in the U.S.[3] The House Committee on Homeland Security has deemed this an unlawful process of alien admission to the U.S.[4]

Moreover, the Department of Homeland Security unofficially estimated “got-aways” at 600,000 in FY 2022, with likelihood that the number is higher in FY2023. Anyway you slice up the data, it appears that a total volume approaching twelve million migrants have entered the U.S. since 2021.

The changes in U.S. immigration policy under the Biden administration have meaningfully modified procedures on how migrants are encountered and either admitted or denied at border crossings.

Who are the Recent Migrants ?

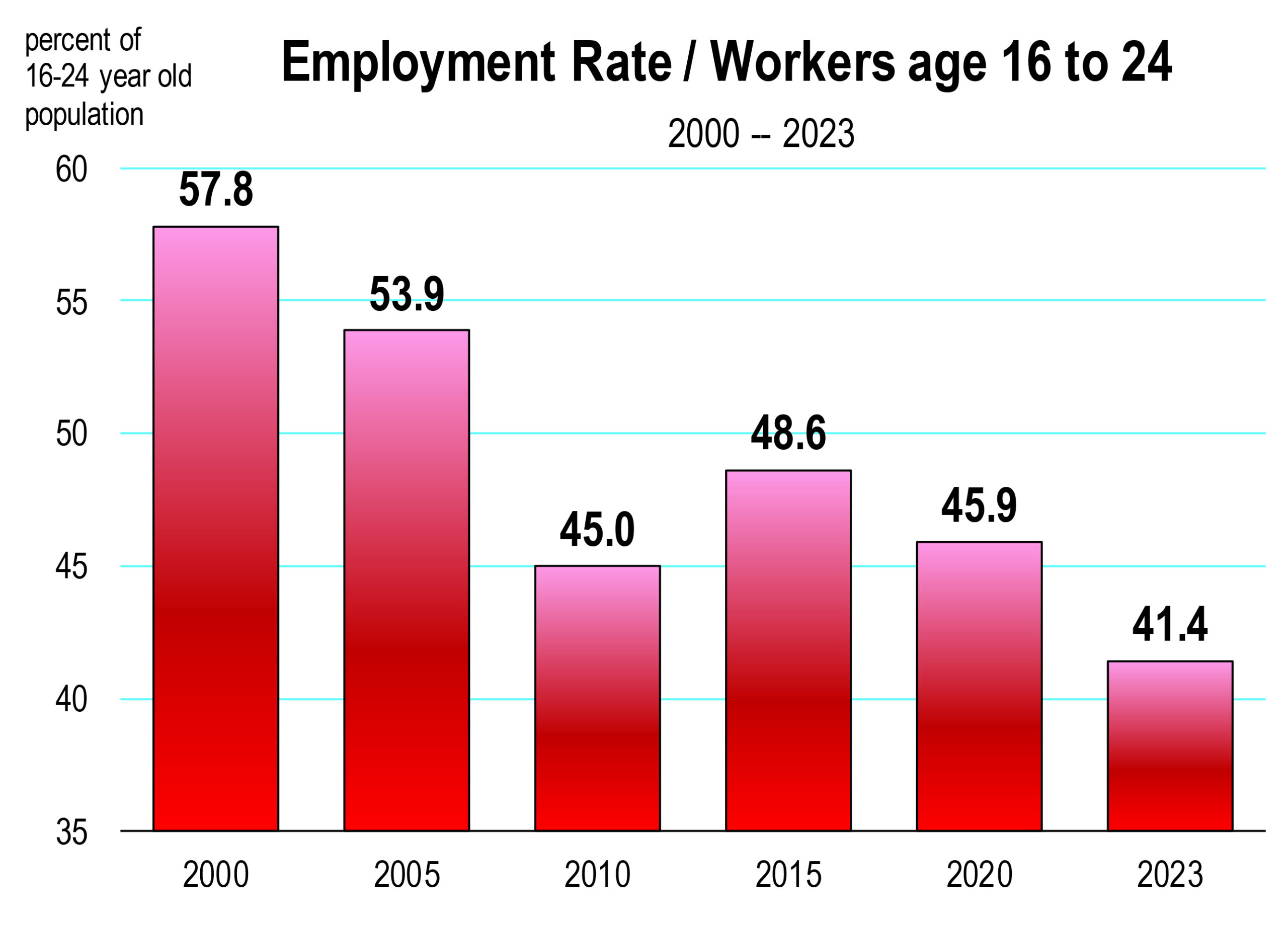

More information about these migrants has surfaced this year in scholarly papers.[5] While immigrants wait for their asylum court dates, they enter the labor force and work because most of them are working age between 18 and 64. Their median age is 28. Compared to the native born population, 78 percent of migrants are in the labor force whereas only 60 percent of the native born population are of working age or want to work. The median age of the  native born population is 37.

native born population is 37.

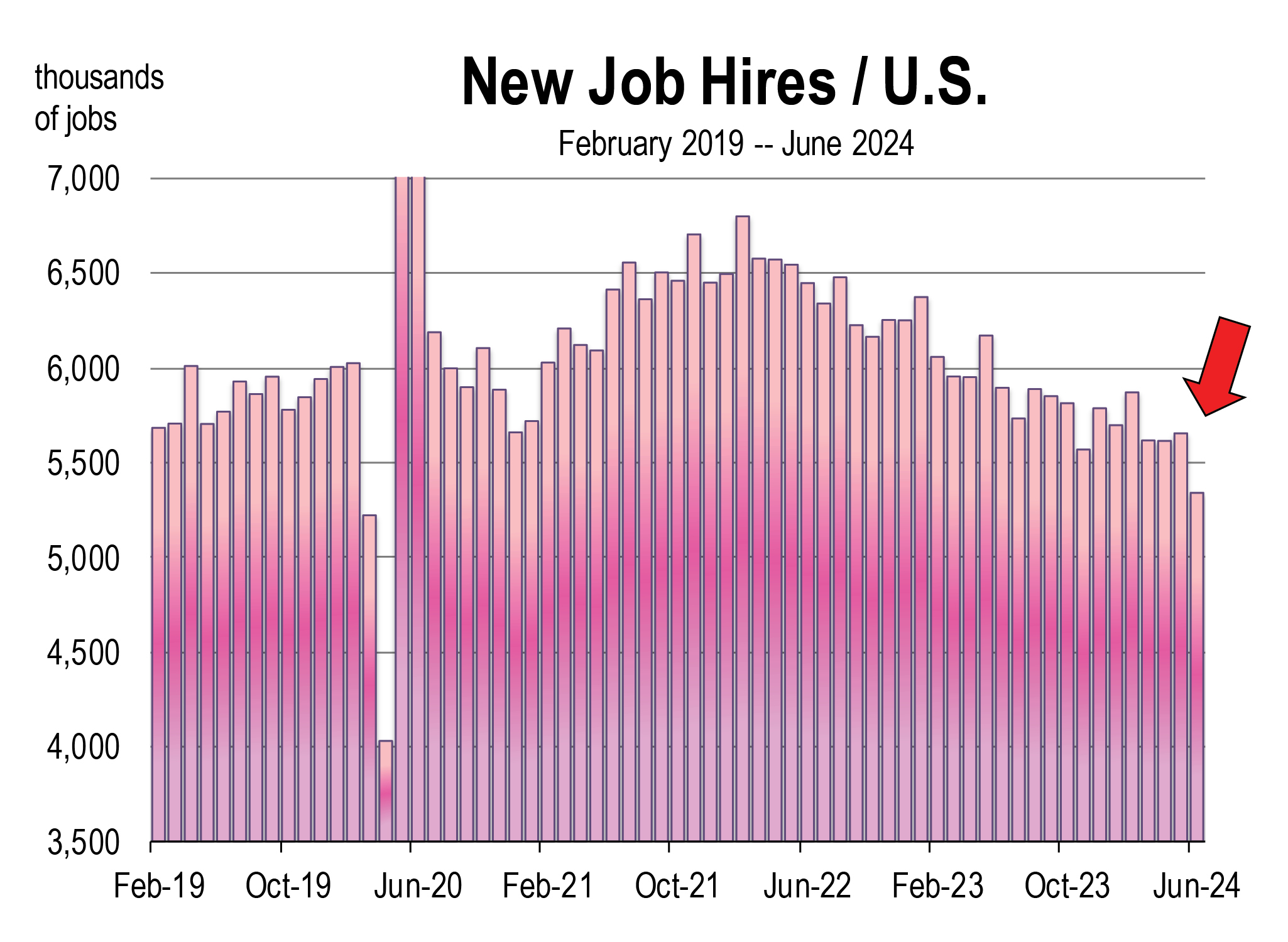

The surge in potential workers from immigration would naturally push the unemployment rate higher as they entered

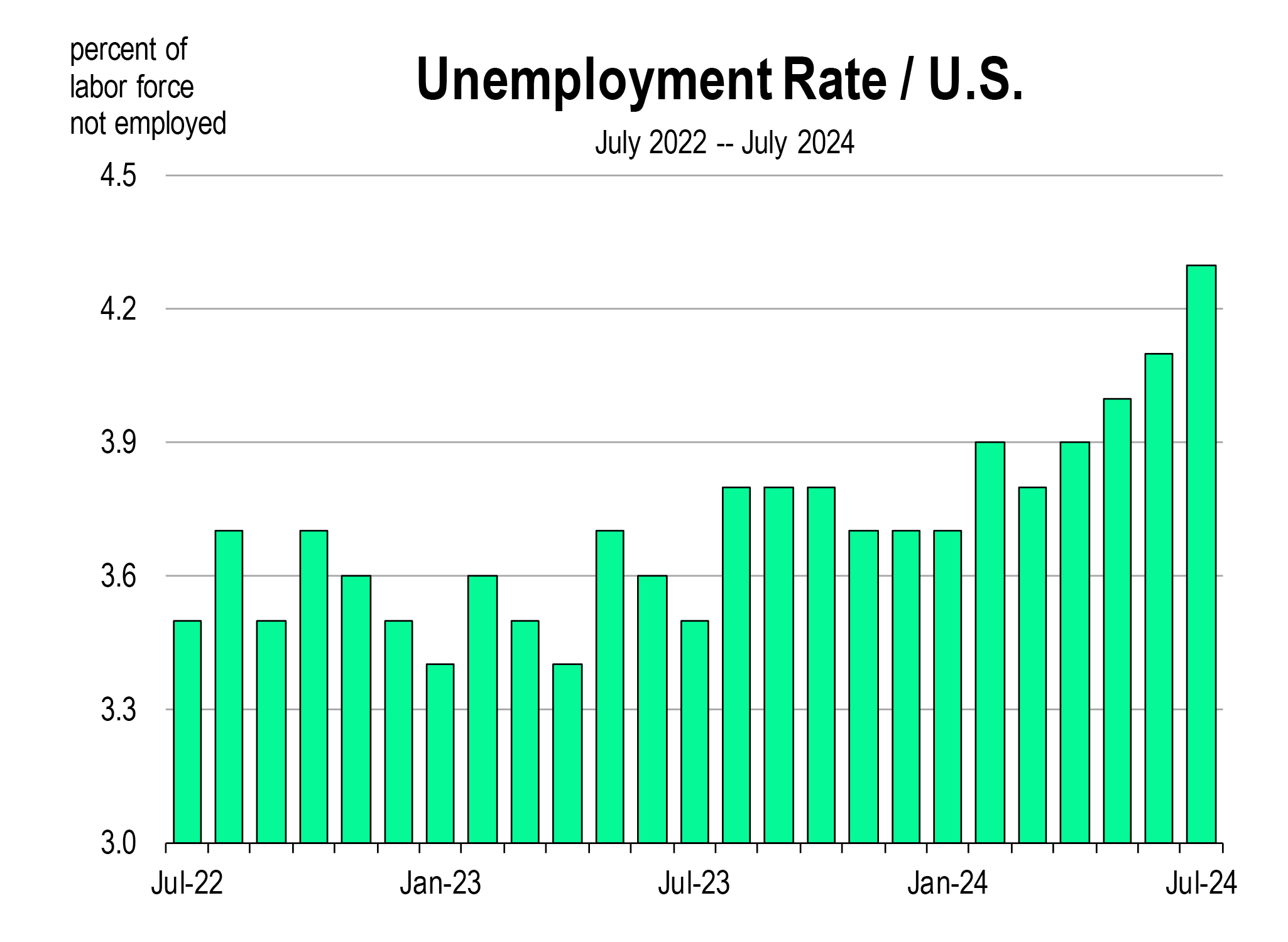

the labor force more rapidly than they became employed. Sure enough, Immigrants who have arrived since early 2020 face higher jobless rates than the broader population. Unemployment for recent immigrants averaged 8.2 percent over the May-June-July 2024 period, versus 4.2 percent for American-born workers and 3.5 percent for earlier immigrant cohorts. Overall unemployment has crept up over the last 18 months, from 3.6 percent in March 2023, to 4.2 percent in August of this year, largely due to the swelling numbers of immigrants looking for jobs.

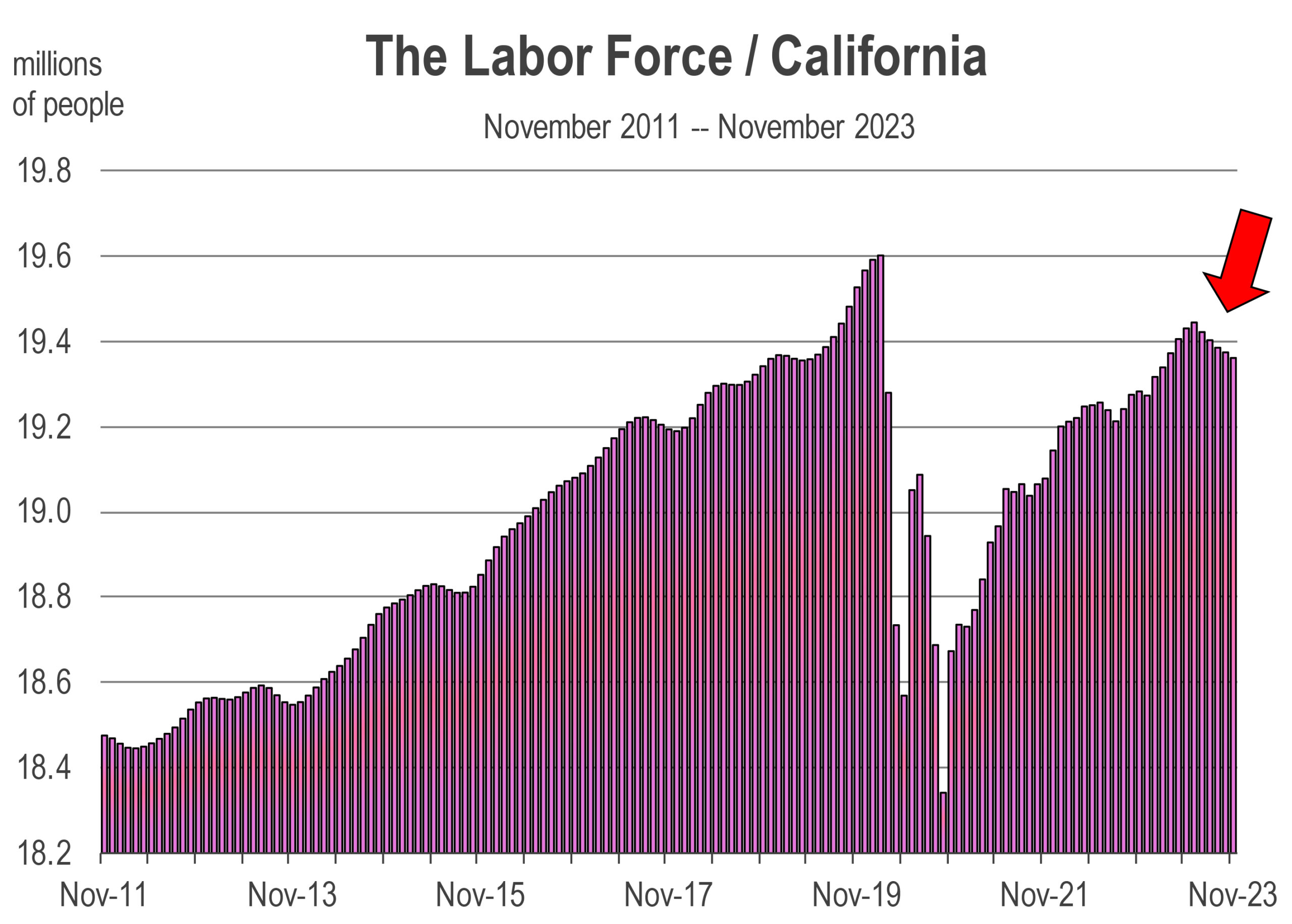

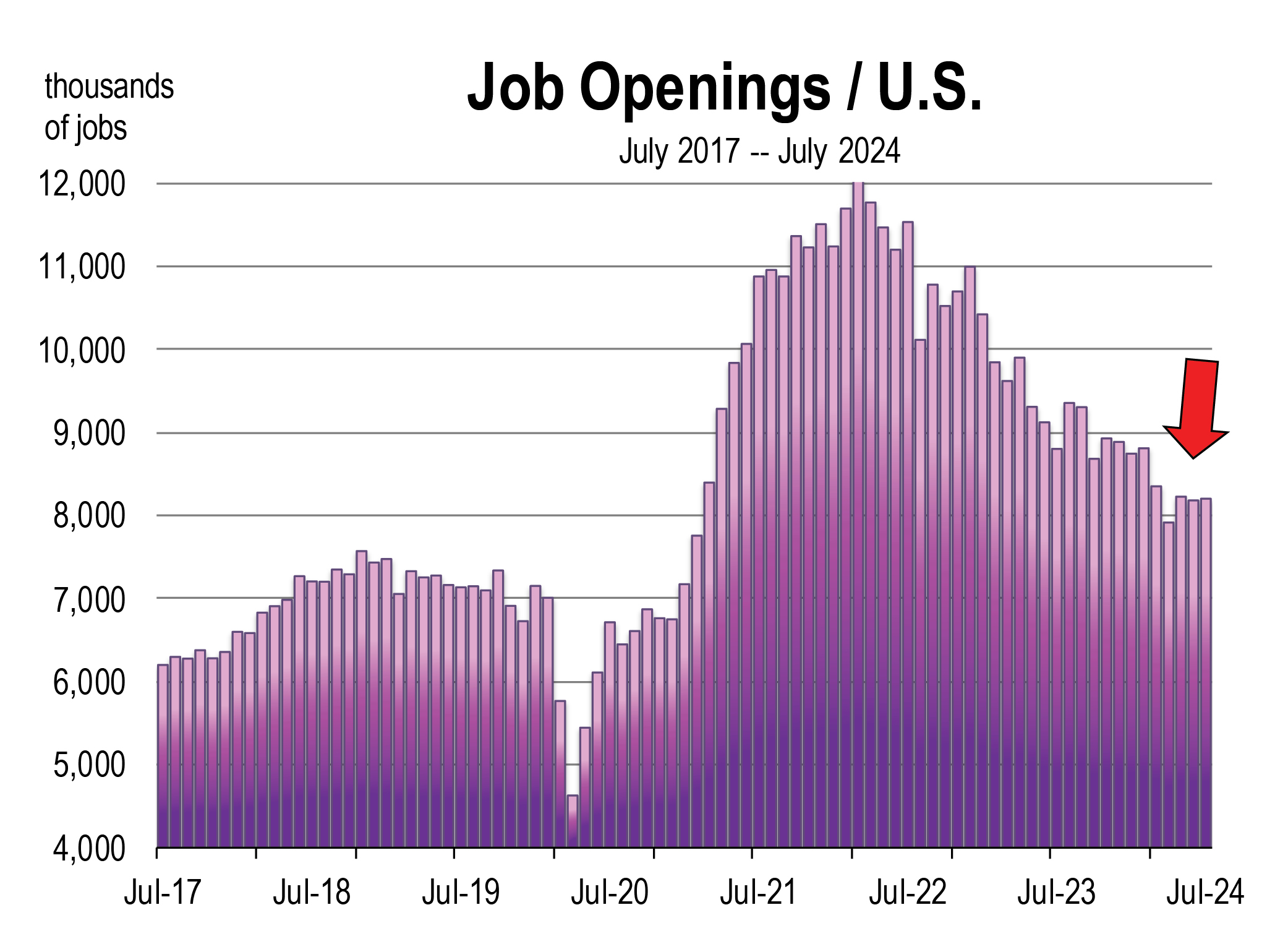

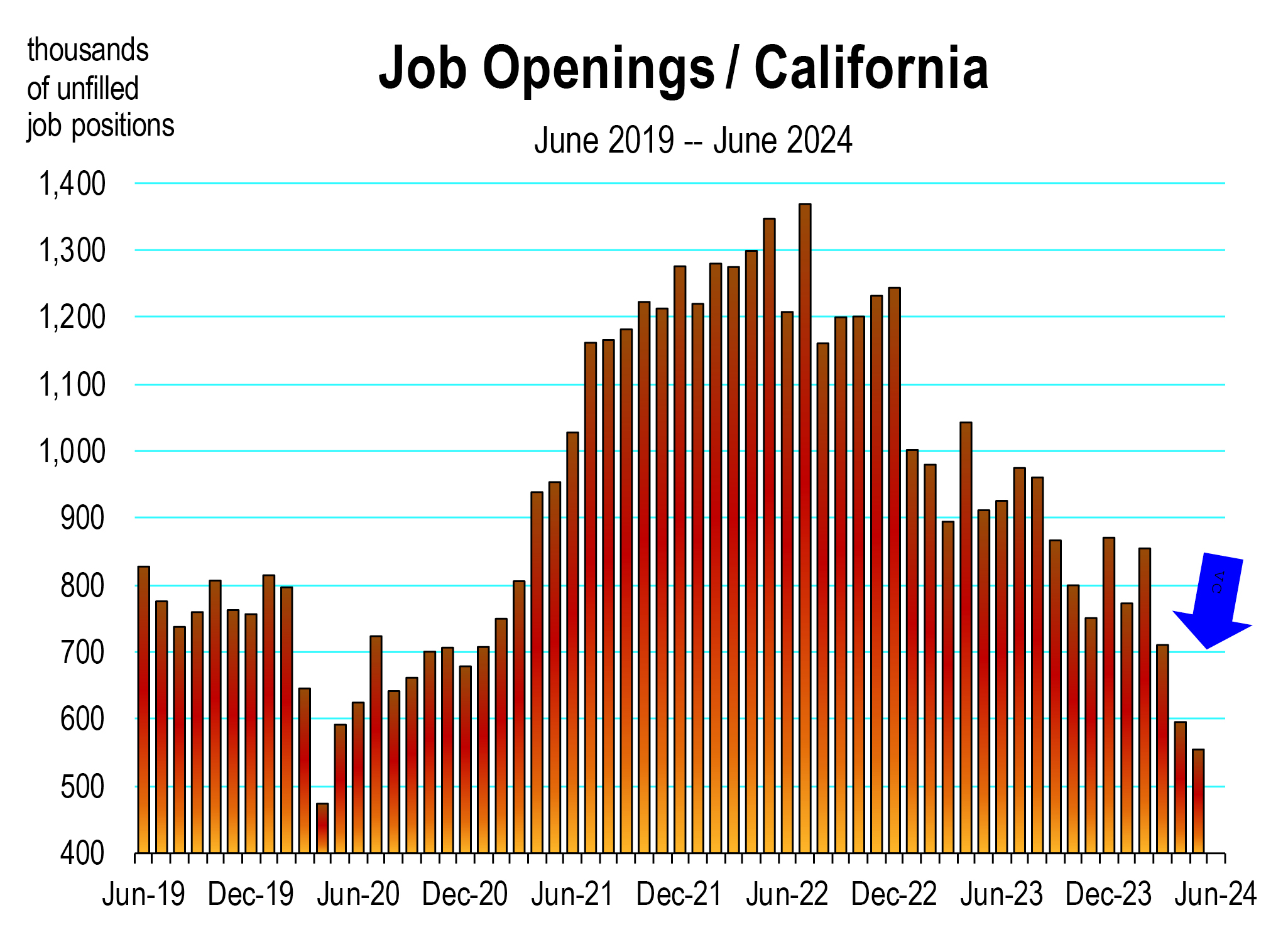

It is true that these workers have alleviated the severe staffing shortages in particular industries in the post pandemic  period. They have contributed significantly to the decline in job openings, which have fallen sharply in California. However, the rate of unemployment in California has gradually moved higher since 2022, and among all 50 states, is

period. They have contributed significantly to the decline in job openings, which have fallen sharply in California. However, the rate of unemployment in California has gradually moved higher since 2022, and among all 50 states, is

the highest with the exception of Nevada. The rising unemployment rate is not necessarily due to a softening of the labor market. It is due to a surge in the labor force that can be linked directly to the recent influx of immigrants.

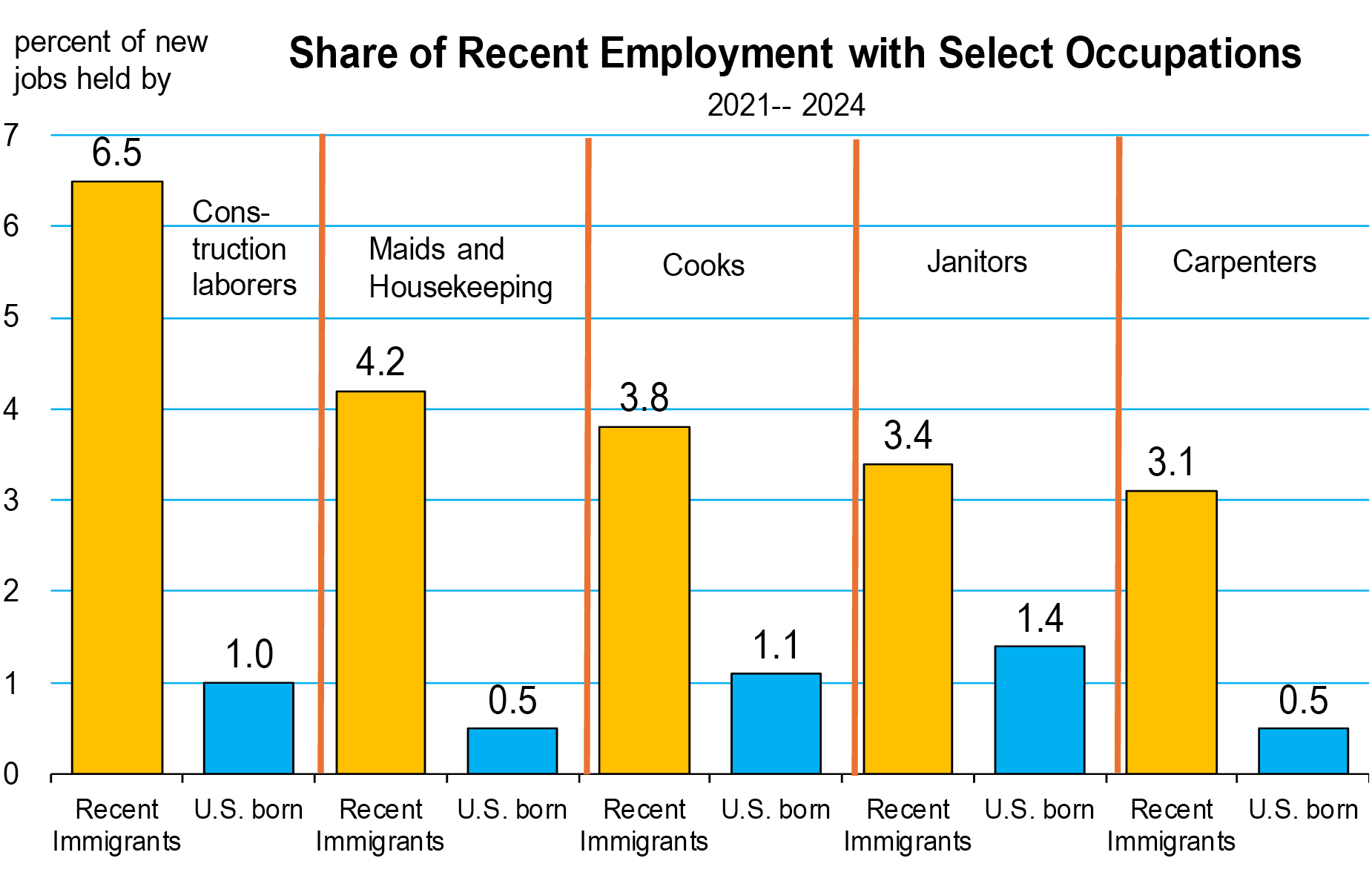

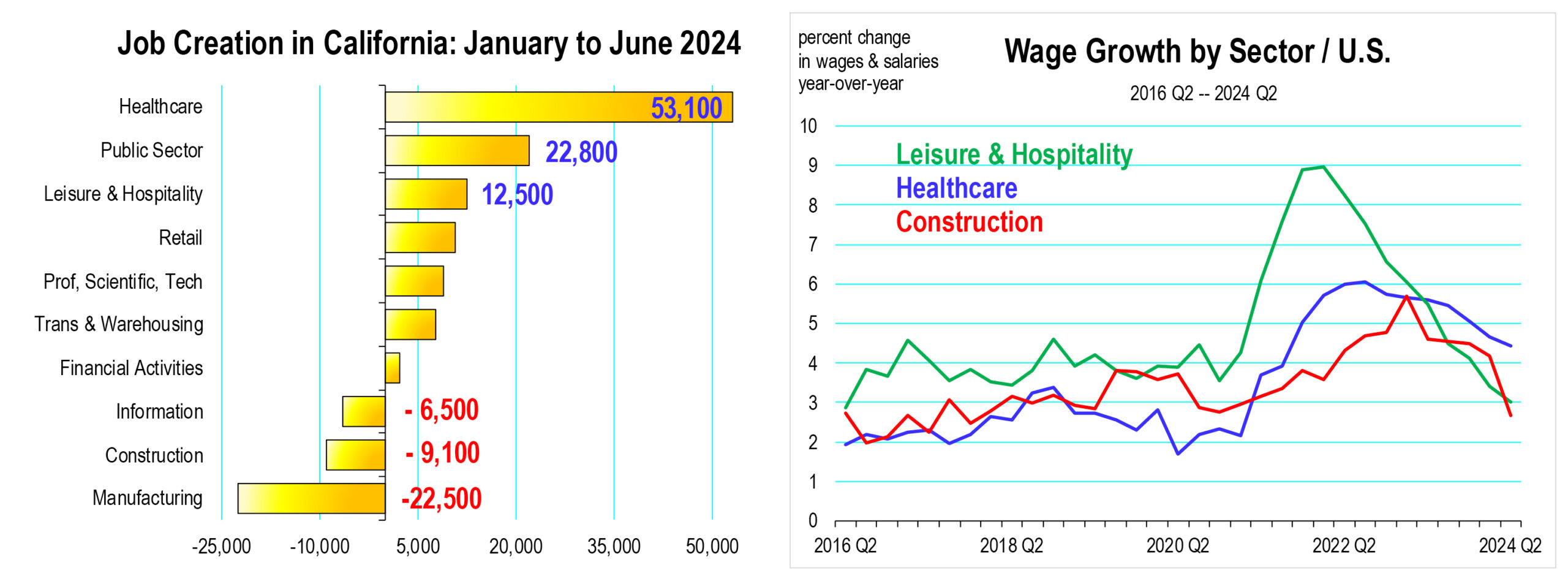

An outsize share of post-2020 immigrants are working in low-paying jobs. The most-common occupations, according to the census data: construction laborers, maids and housecleaners, and cooks.

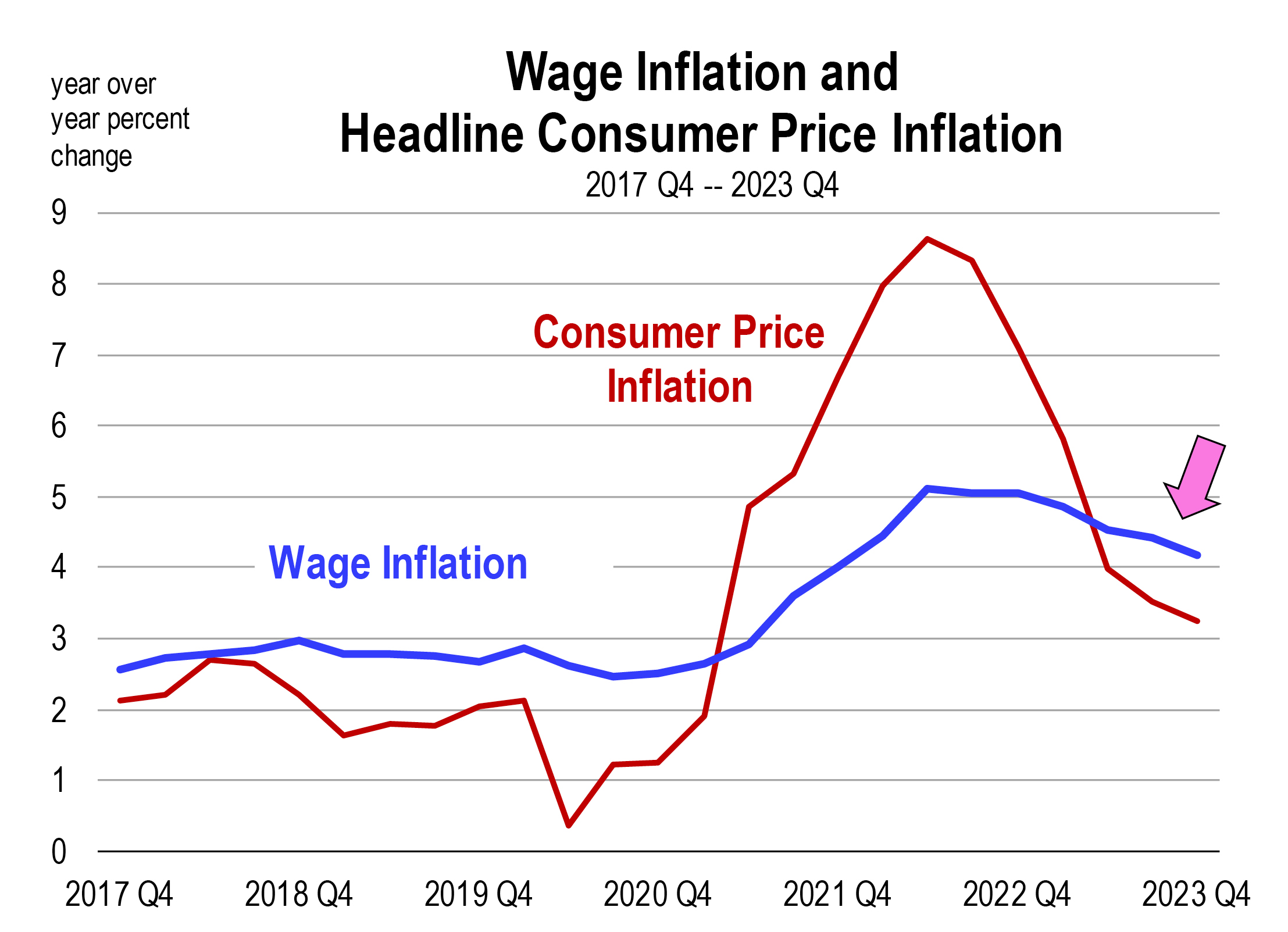

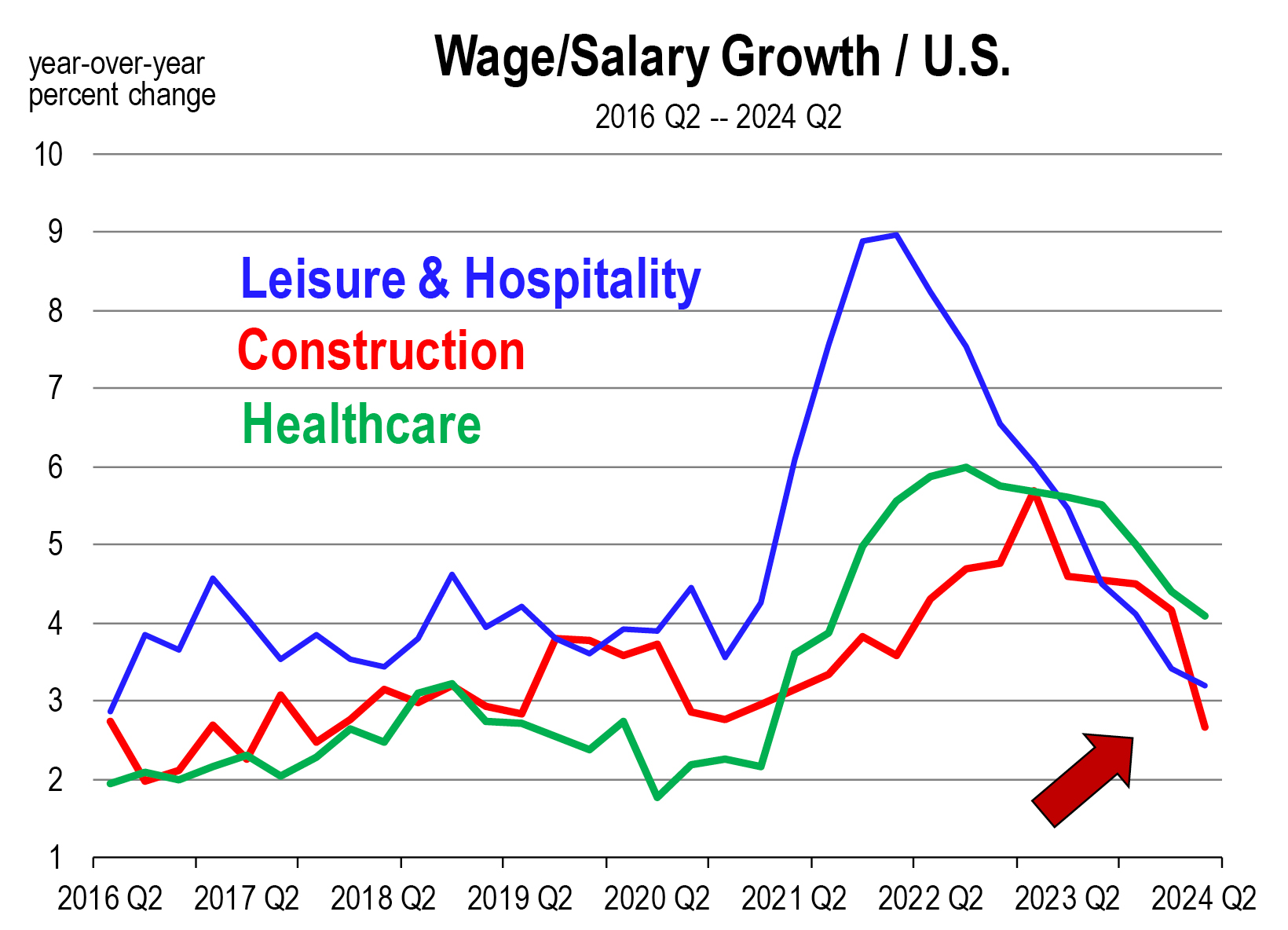

Furthermore, the influx of immigrant workers that has helped fill job openings also dampened wage growth across the affected industries in the state. Because of the tight labor markets in 2022, wage growth averaged 6-7 percent. Now it has moderated to between 3 and 4 percent, falling sharply in migrant-intensive industries which include construction and leisure & hospitality.

A meaningful data revision is likely coming

Population growth in California which has been reported as negative by Census, has more than likely been positive since 2021, as more net migrants from the southern border have and are being diverted into California. Census has simply not caught up with the migrant surge at the border. The wage and salary data appear to confirm this. The Wall Street Journal reported that new migrants are living in counties that rely on farm workers, construction services, food and hospitality, and helpers in healthcare (home health aids). This includes Los Angeles County, the Inland Empire, and the Central Valley counties, along with San Diego, Orange, and Ventura Counties.

Unemployment rates are likely higher in these areas with increased population and labor forces than is being reported because the most recent immigrants from 2021 to present cannot be contacted by survey which is the principal mechanism for recording economic data on the resident labor force, workforce, and the number of unemployed.

Is the migration surge a cost or a benefit ?

Many government analysts laud the immigration numbers warning that if rates of entry into the U.S. return to the pre-2021 normal, future economic growth in the U.S. will be insufficient to sustain our current standard of livings. The retirement of the baby boomers and overall aging of the workforce, as well as low and falling birth rates mean population growth will become entirely dependent on immigration by 2040, as deaths of U.S.-born residents will outpace births.

However, what is missing here is a thorough analysis of the costs existing U.S. residents bear as a result of massive immigration and the type of immigration that is being enabled today. While immigrants fill jobs, mostly lower-paying, they also use social services that are often more costly than the payroll and sales taxes that they generate, by working and spending. This includes K-14 education, Medi-Cal, and assistance payments including Calfresh for low income individuals and families. Furthermore, migrants that ultimately find private housing are and will continue to exacerbate the housing crisis in California.

A recent paper by the Center for Immigration Studies prepared for the House Judiciary Committee concluded that:

Illegal immigrants are a net fiscal drain, meaning they receive more in government services

than they pay in taxes. This result is not due to laziness or fraud. Illegal immigrants actually

have high rates of work, and they do pay some taxes, including income and payroll taxes. The

fundamental reason that illegal immigrants are a net drain is that they have a low average

education level, which results in low average earnings and tax payments. It also means

a large share qualify for welfare programs, often receiving benefits on behalf of their U.S.-

born children. Like their less-educated and low-income U.S.-born counterparts, the tax

payments of illegal immigrants do not come close to covering the cost they create.[6]

The issue regarding the alleged need for more immigration to sustain U.S. GDP growth may be entirely refuted by the coming era of AI that is just ahead of us. With more automation in both the workplace and in the thinkspace, will we actually need more workers? Robots are already replacing maids at hotels. iPads have replaced waiters at restaurants. It is likely that the size of the workforce will ultimately shrink as more mundane and repetitive jobs are mechanized, and more AI tools can substitute for jobs in education, professional services, customer services, manufacturing, warehousing, transportation, and retail trade.

A bigger fear may be how we actually find jobs for lower skilled workers. Immigration has been the backbone of the U.S. labor force for more than 100 years. However, we need to consider a more discerning immigration policy that will admit newcomers who will pay their way and fill jobs that will be necessary in the evolving economy of today.

1Gallup, Most Important Problem, monthly survey of Americans, https://news.gallup.com/poll/1675/most-important-problem.aspx

2An “encounter,” previously known as an apprehension, includes all people who are either stopped by the Border Patrol or who turn themselves in. Most migrants simply approach the Border and indicate they intend to seek asylum.

3U.S. Customs and Border Protection, “CBP releases August 2024 Monthly Update,” September 16, 2024, https://www.cbp.gov/newsroom/national-media-release/cbp-releases-june-2024-monthly-update

4https://homeland.house.gov/2024/04/30/new-documents-reveal-airports-used-by-secretary-mayorkas-to-fly-hundreds-of-thousands-of-inadmissible-aliens-into-u-s-via-chnv-mass-parole-scheme/

5Brookings, Who are the New Immigrants?” Tara Watson and Simon Hodson, September 11, 2024, https://www.pewresearch.org/short-reads/2024/09/27/key-findings-about-us-immigrants/

Pew Research Center, “What the data say about Immigrants to the U.S., by Mohamad Moslimani and Jeffrey Passel, September 27, 2024, https://www.pewresearch.org/short-reads/2024/09/27/key-findings-about-us-immigrants/

Wall Street Journal, “How Immigration Remade the U.S. Labor Force,” by Paul Kieman, September 4, 2024.

6Center for Immigration Studies, “The Cost of Illegal Immigration to Taxpayers,” by Steven Camarota, Director of Research, January 2024, page 1

The California Economic Forecast is an economic consulting firm that produces commentary and analysis on the U.S. and California economies. The firm specializes in economic forecasts and economic impact studies, and is available to make timely, compelling, informative and entertaining economic presentations to large or small groups.

![]()

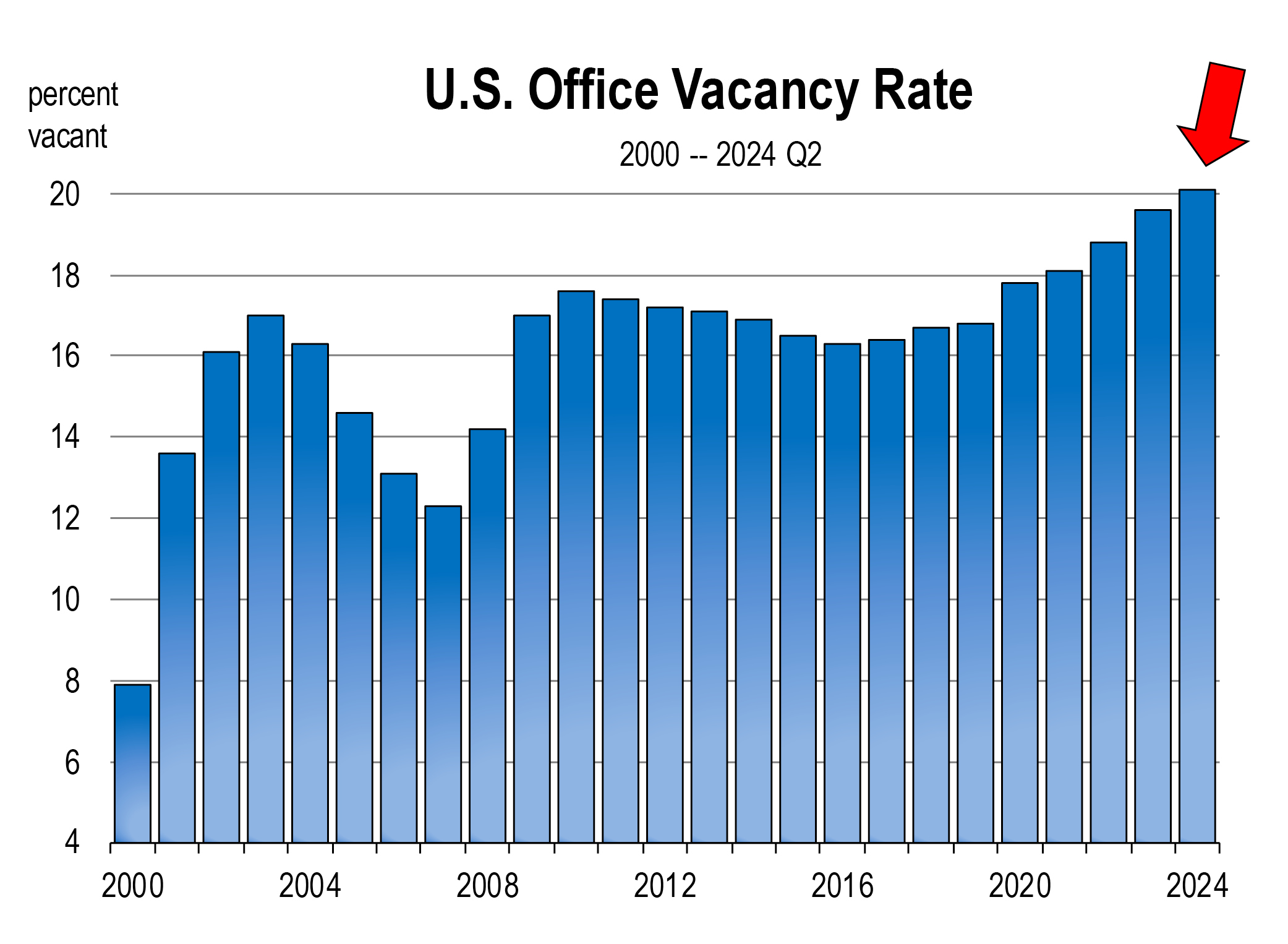

The issue for rising vacancy in the office market is typically that office using employment has contracted as part of a broader based employment decline. Consequently, companies cut back on space to cut costs and “weather the downturn”. That’s not the case this time. We have near record levels of employment in office using sectors. The problem is that many of these workers are not using the office, and are instead working from home.

The issue for rising vacancy in the office market is typically that office using employment has contracted as part of a broader based employment decline. Consequently, companies cut back on space to cut costs and “weather the downturn”. That’s not the case this time. We have near record levels of employment in office using sectors. The problem is that many of these workers are not using the office, and are instead working from home.

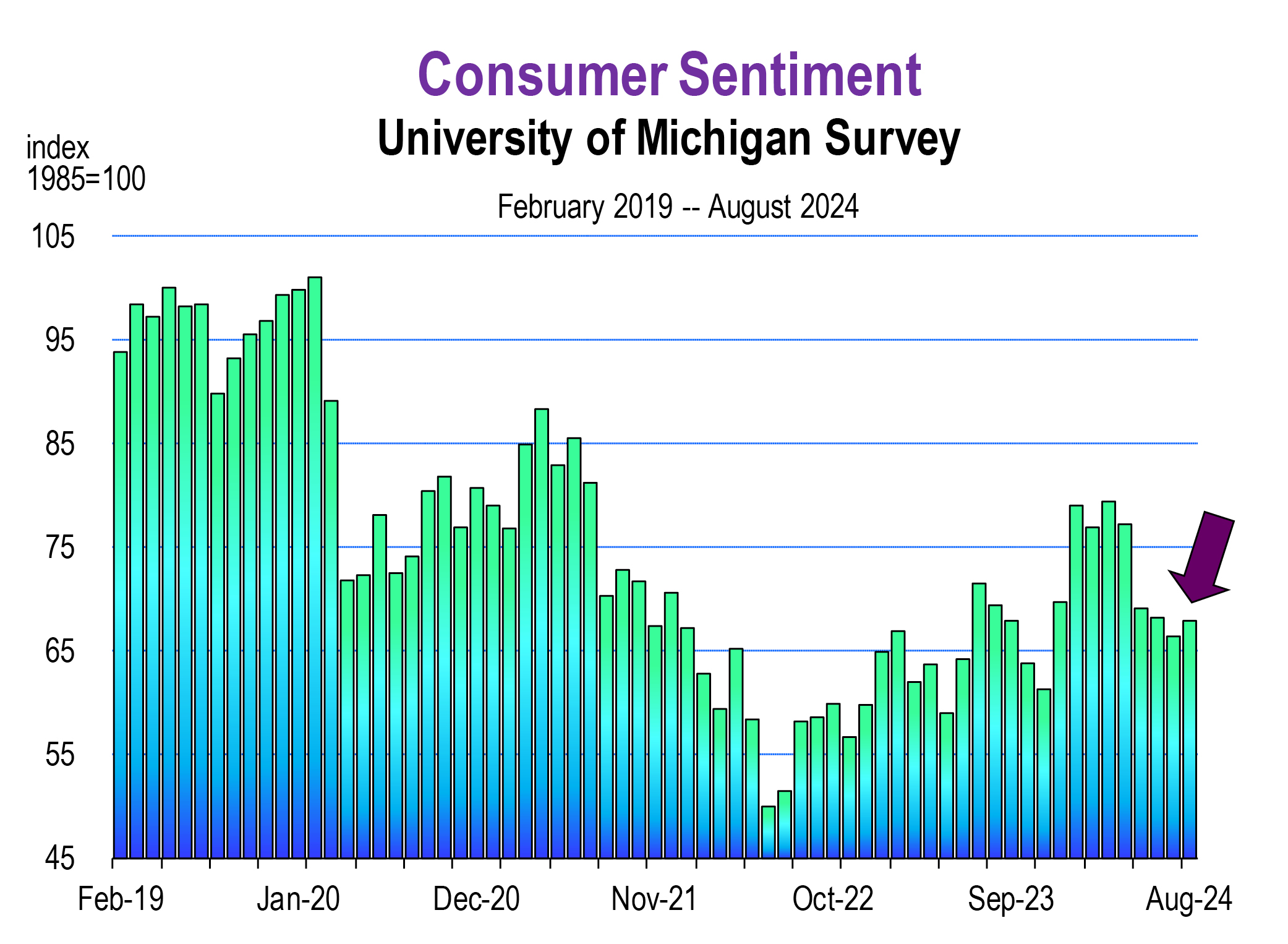

Moody’s continued to report the following day that

Moody’s continued to report the following day that