Mark Schniepp

August 2025

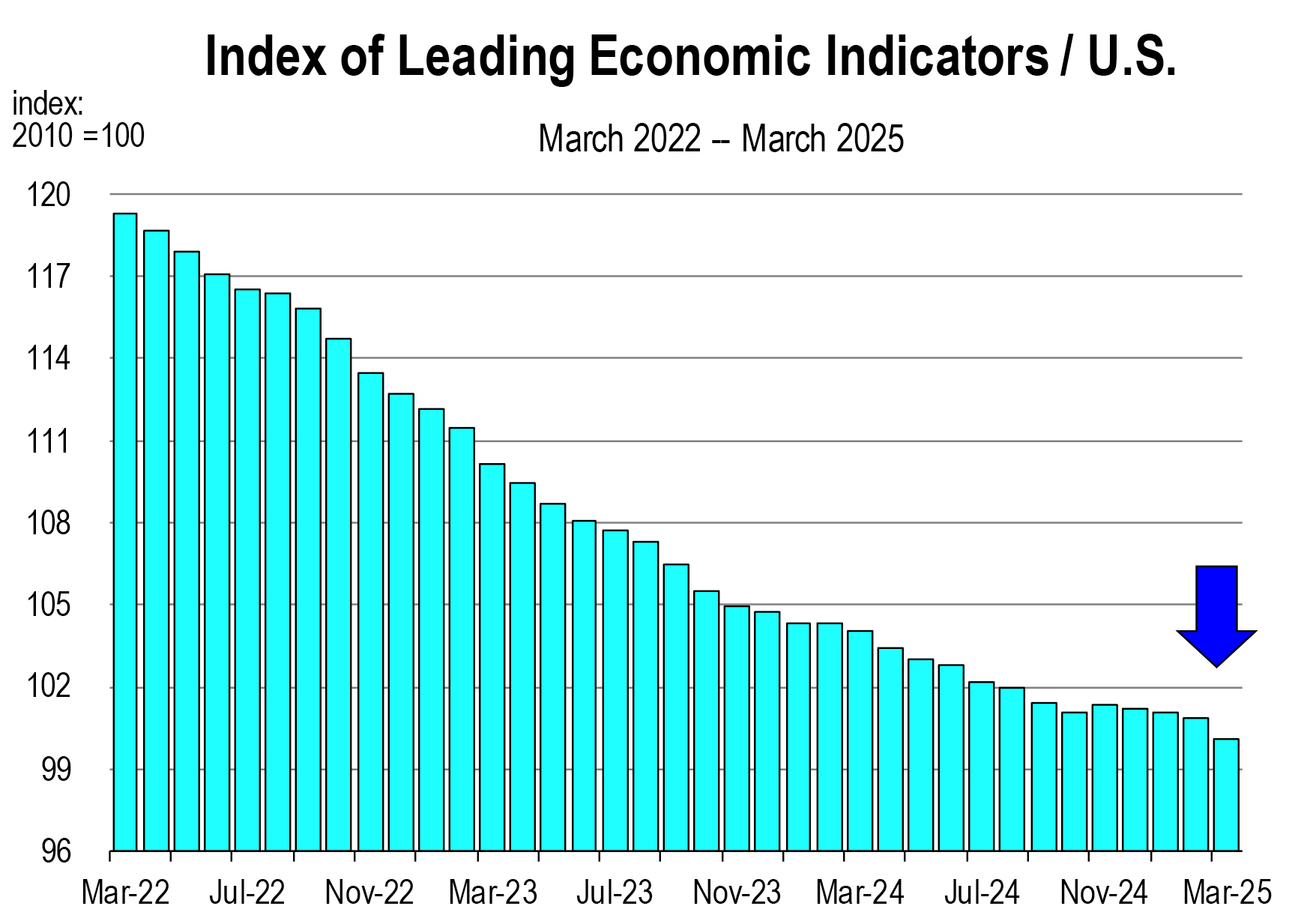

Stronger Growth in Quarter 2 Offset the Quarter 1 Slowdown

We were told by a flurry of the analytical pundits observing the Trump administrations new polices that the proposed tariff regimen (combined with the downsizing of federal government) would crash the equities market, spike inflation, lower GDP and employment growth, resulting in recession, chaos and trauma.

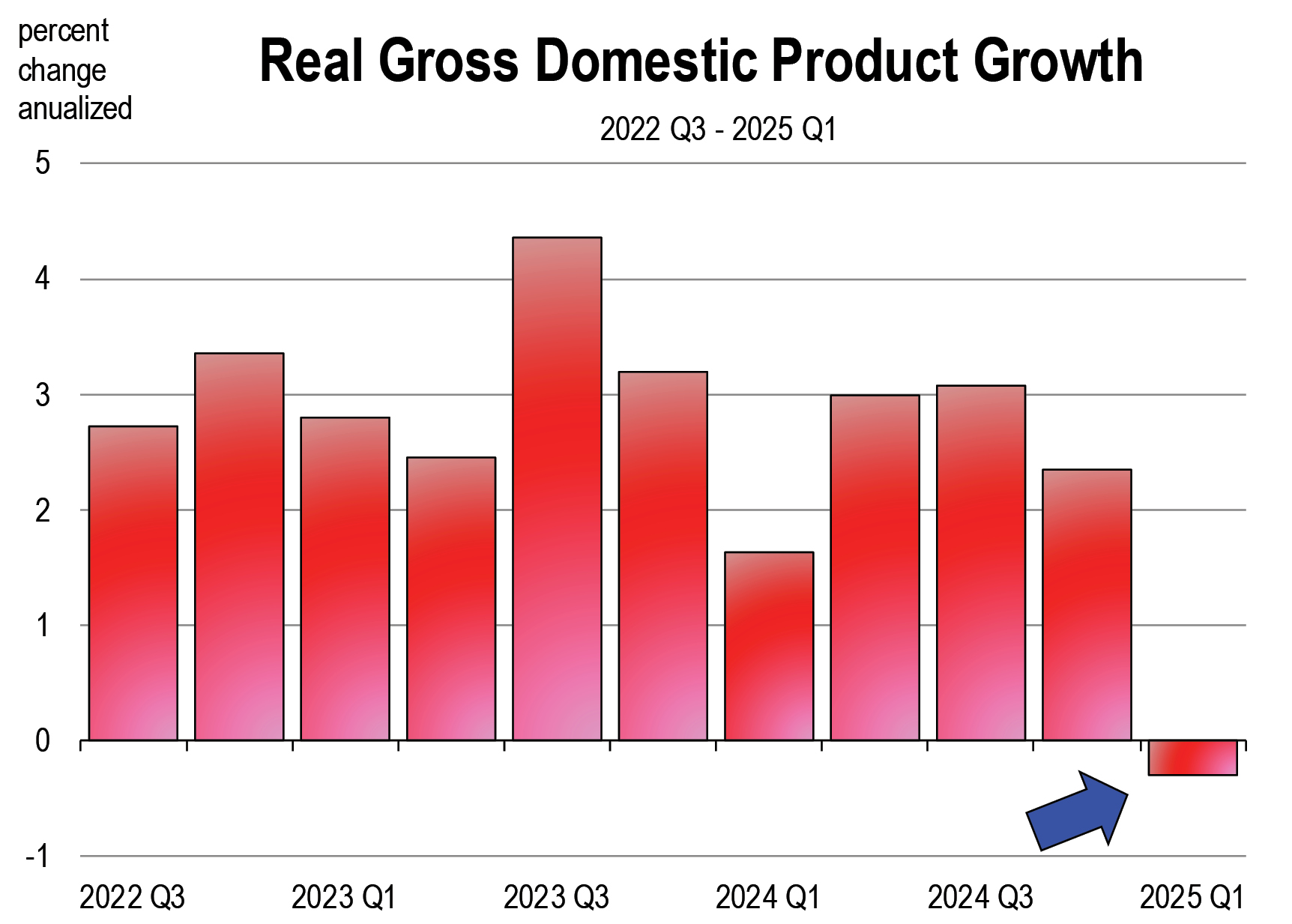

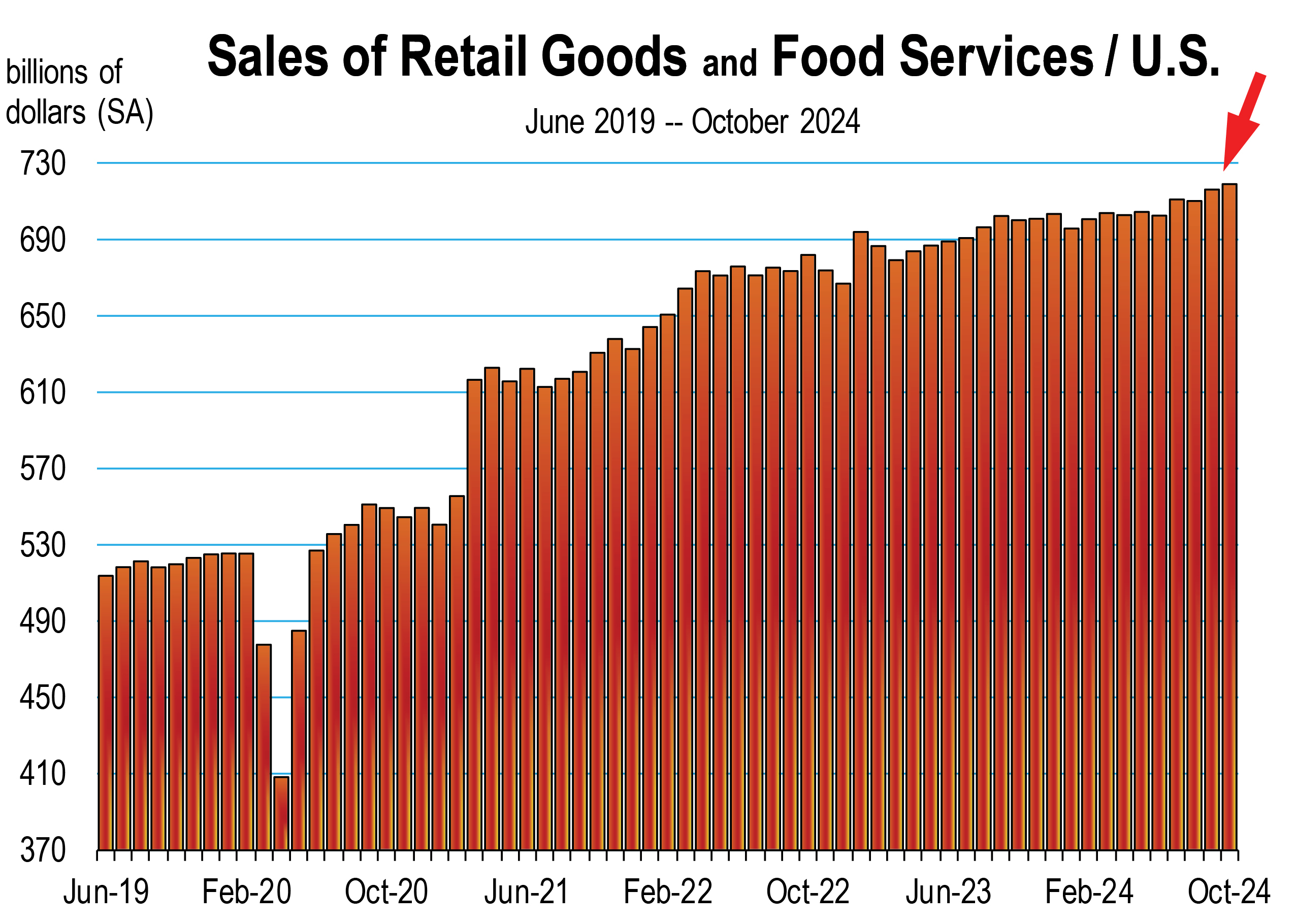

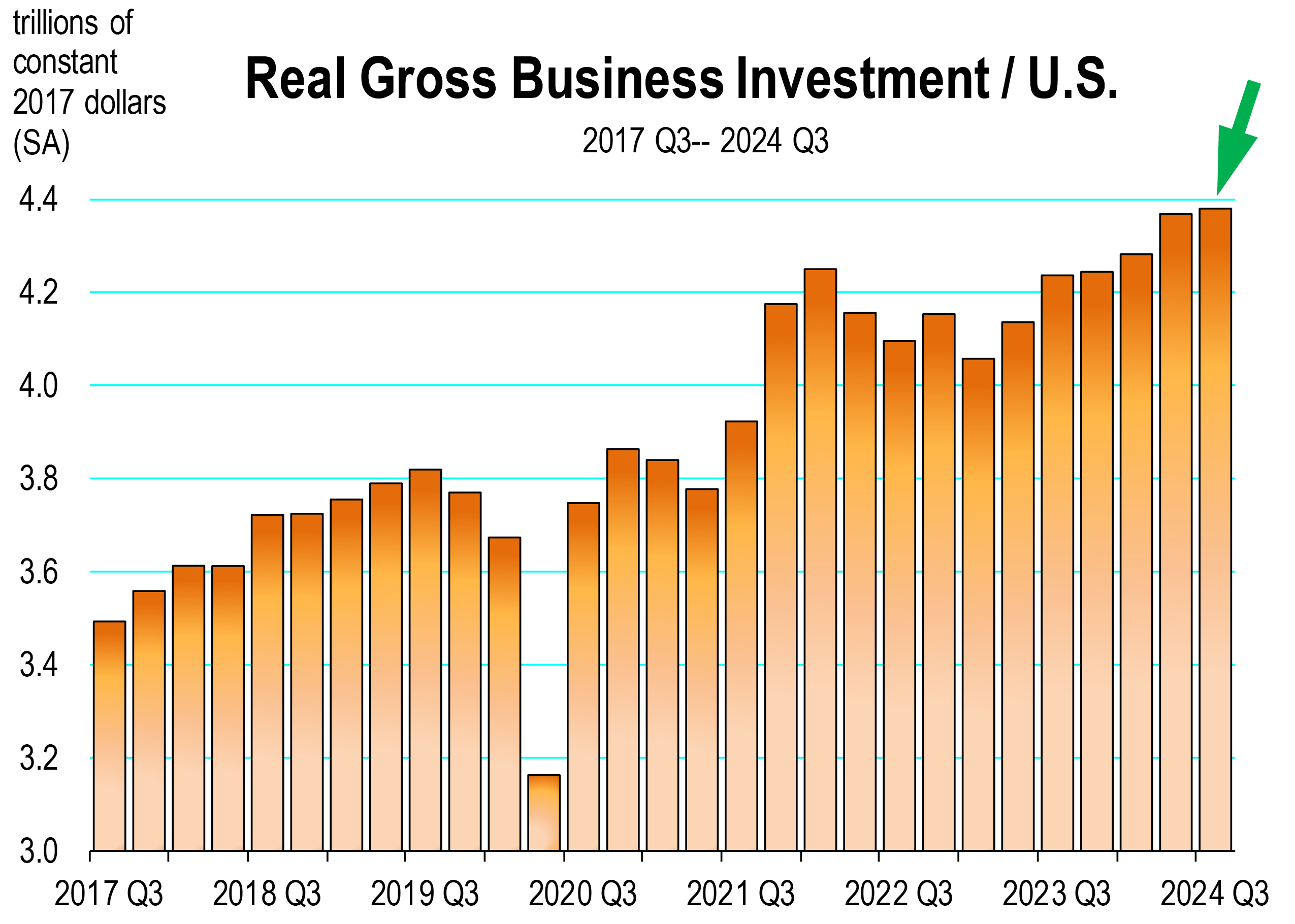

That was last March and April. Fast forward five months to August 2025: the stock market moved to an all time high in July, GDP growth came in at 3 percent for quarter 2, labor markets are stable and creating jobs, and inflation has moved lower. Every indicator that was predicted to move in a negative fashion as a result of Trumpenomics 2.0 has moved exactly the other way.

Now the economy is not entirely out of the woods as there are still concerns and potential downsides on the horizon, but the probability of a meaningful negative outcome this year is less certain today.

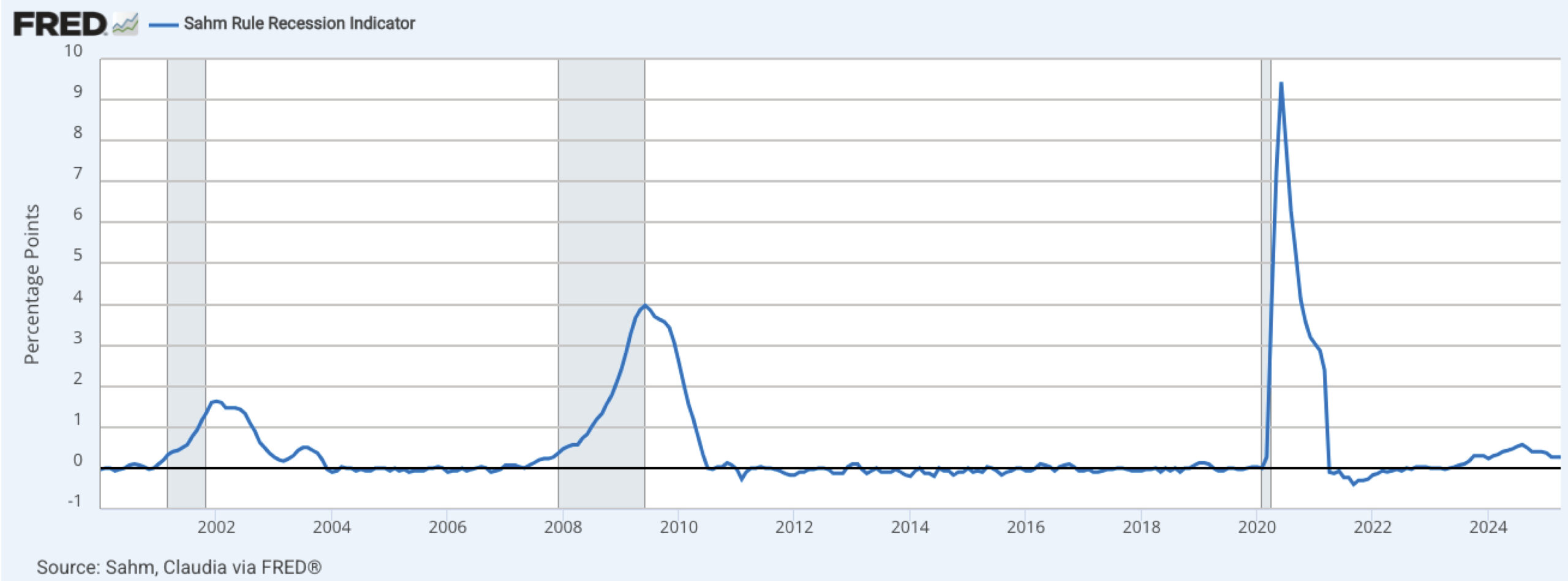

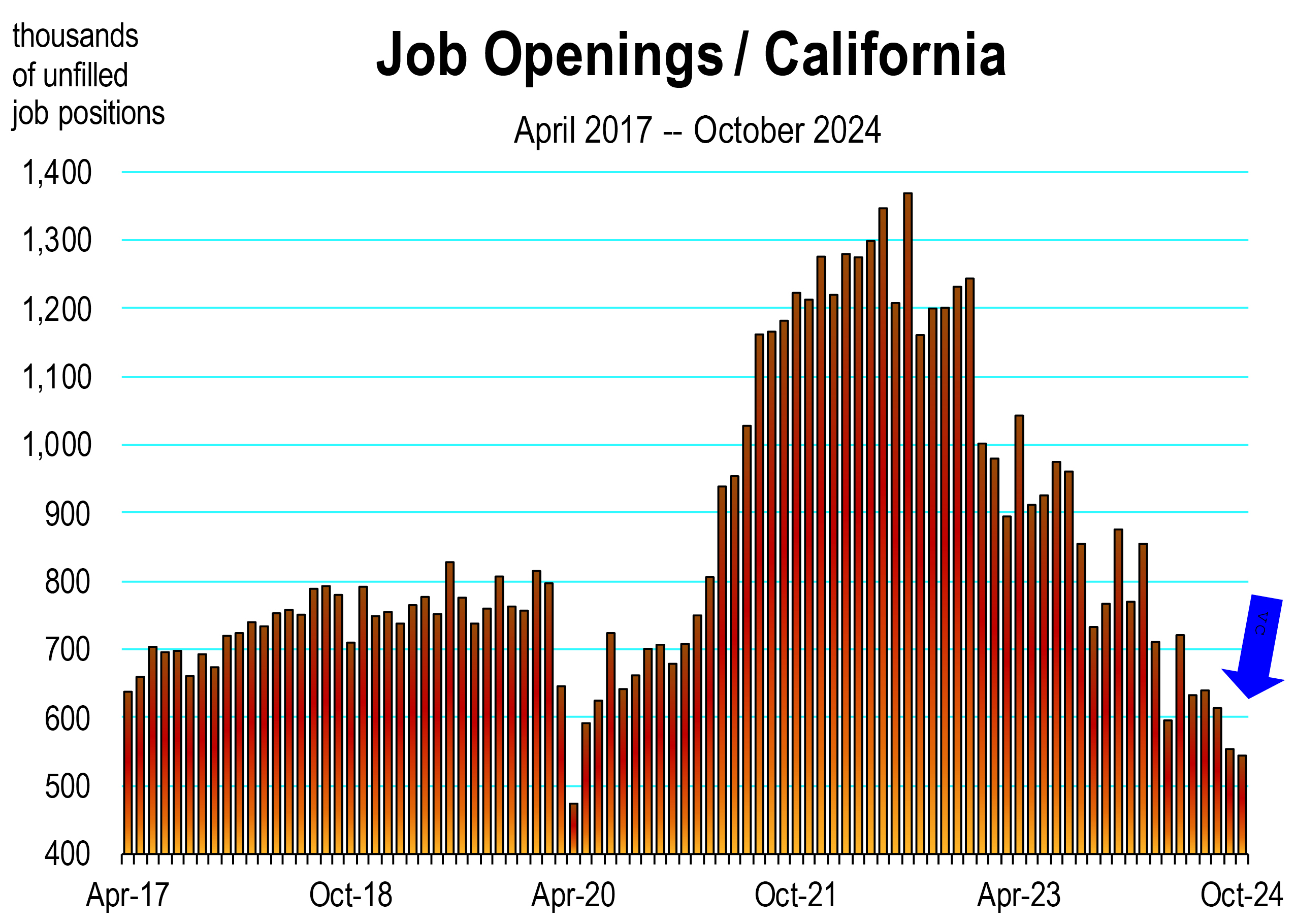

The labor market report for July was weak, although preliminary. Unemployment still remains at 4.2 percent, a level that has generally held steady over the last 13 months. AI appears to be impacting job creation in many industries, as we reported last month in this newsletter series.

Tariffs have been delayed in implementation. Businesses have adopted strategies to mitigate tariff risk, like supply chain diversification or absorbing the tariff cost. Consumers have substituted to other goods or not incurred the higher costs predicted for goods coming from China, Europe, Canada, or Mexico.

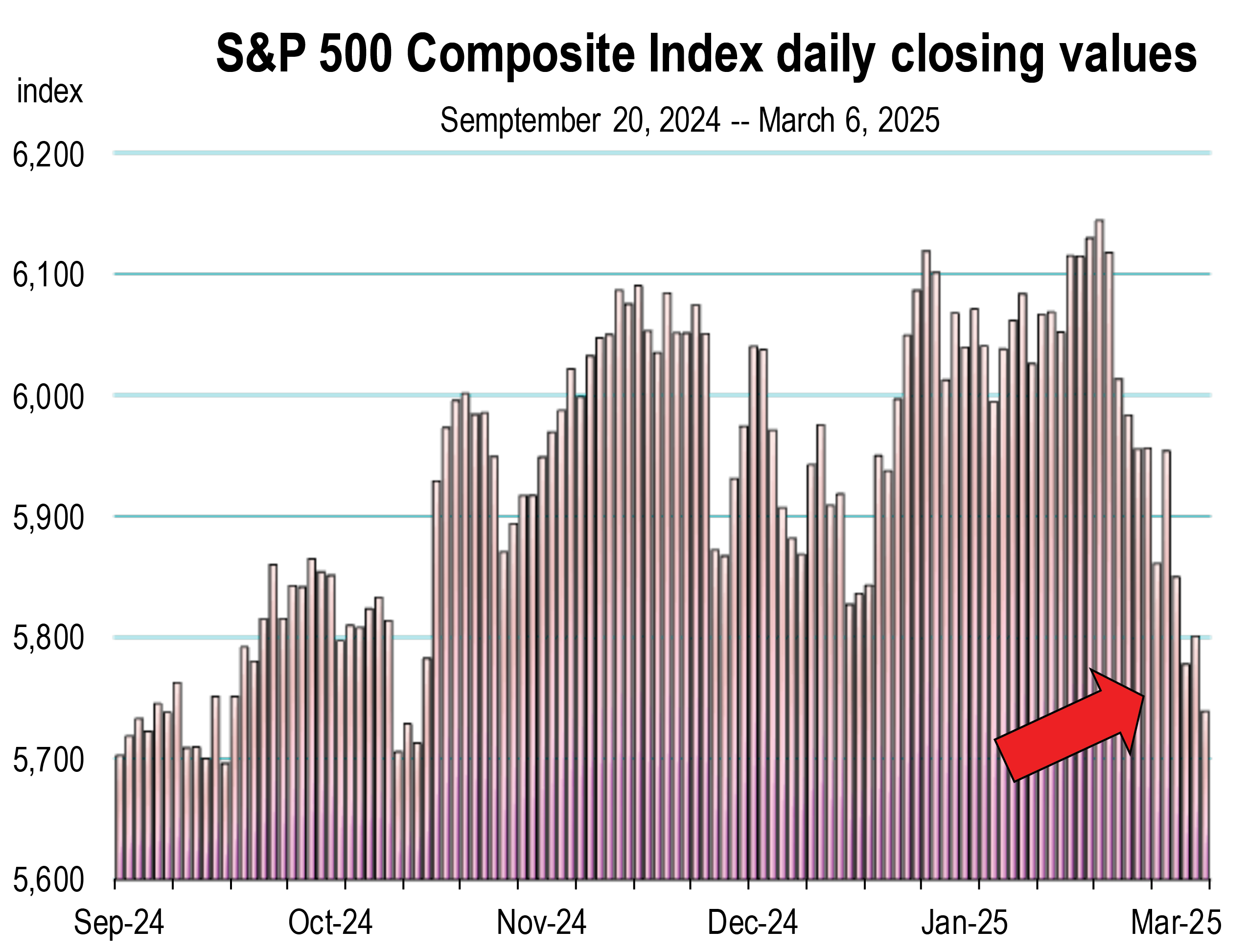

The stock market is overly worrisome with uncertainty, and overreacted last April. Earnings reports for Q1 and now for Q2 have been more positive then expected. The market pushed to an all time record high in July. It looks overbought now so don’t be surprised if a correction this month and into September dominates the movement of stock values.

The full impact of tariff policy is still unfolding. The pundits are still warning that the negative effects on prices, employment and GDP growth will become more pronounced in the future.

Course Correction on Tariffs

The initial tariff plan revealed on April 2 with the reciprocal tariff rates on all countries worldwide appears now to have been a gigantic PR scheme to coax our trading partners to rethink their tariff rates on U.S. exports and/or their non-tariff barriers which effectively preclude U.S. exports altogether.

A clearer picture of the global trade landscape is now emerging.

The United Kingdom was the first country to negotiate trade policy with the U.S., back in May. The tariff rate was set at 10 percent. The EU is the top trading partner with the U.S. and reached a 15 percent tariff agreement on July 29. The same rate was negotiated with Japan 7 days earlier. South Korea reached a deal on July 30. Though these recent trade deals have eased some uncertainty around tariff policy, they strongly suggest 15% is shaping up to be the floor for tariffs.

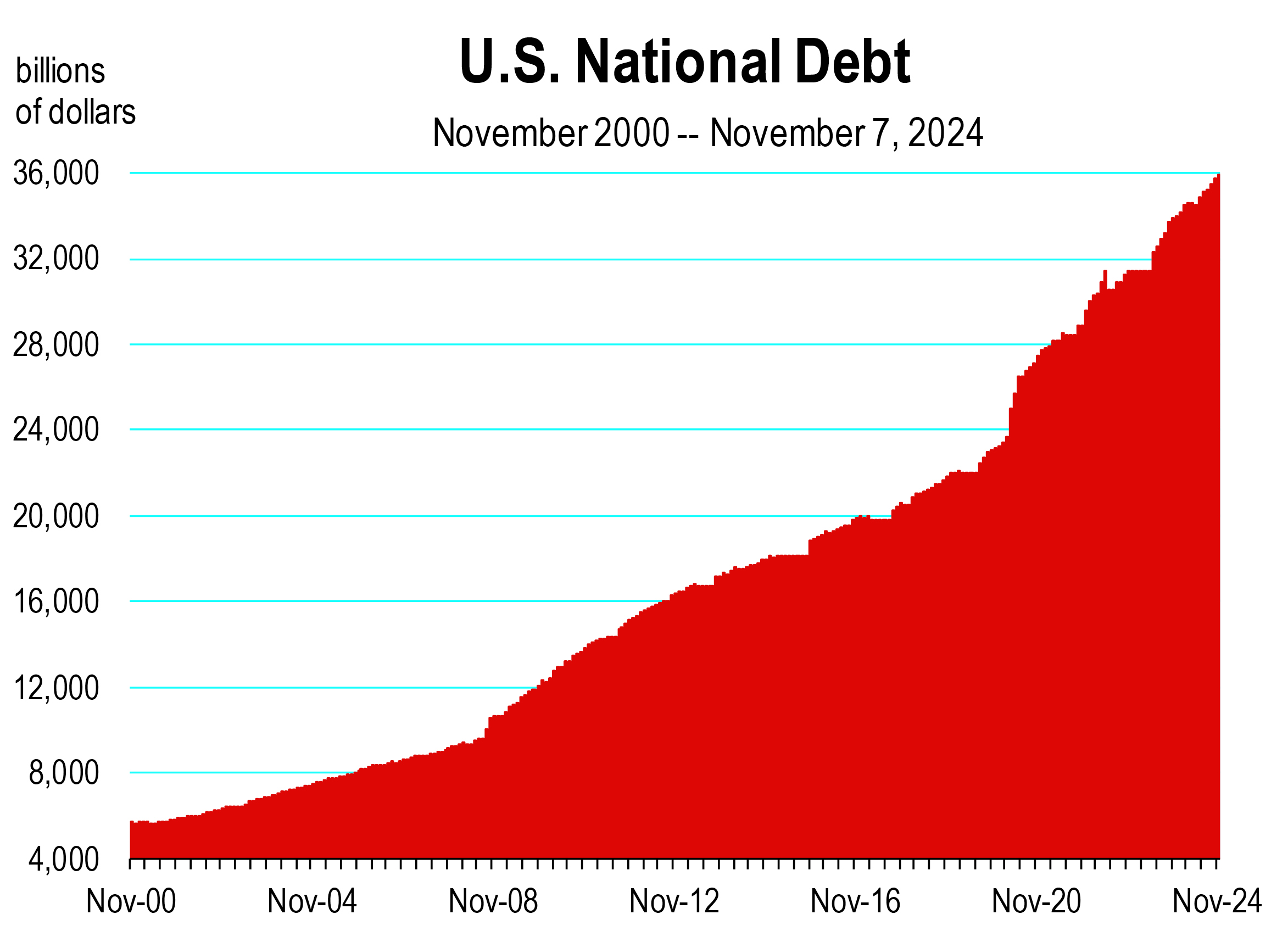

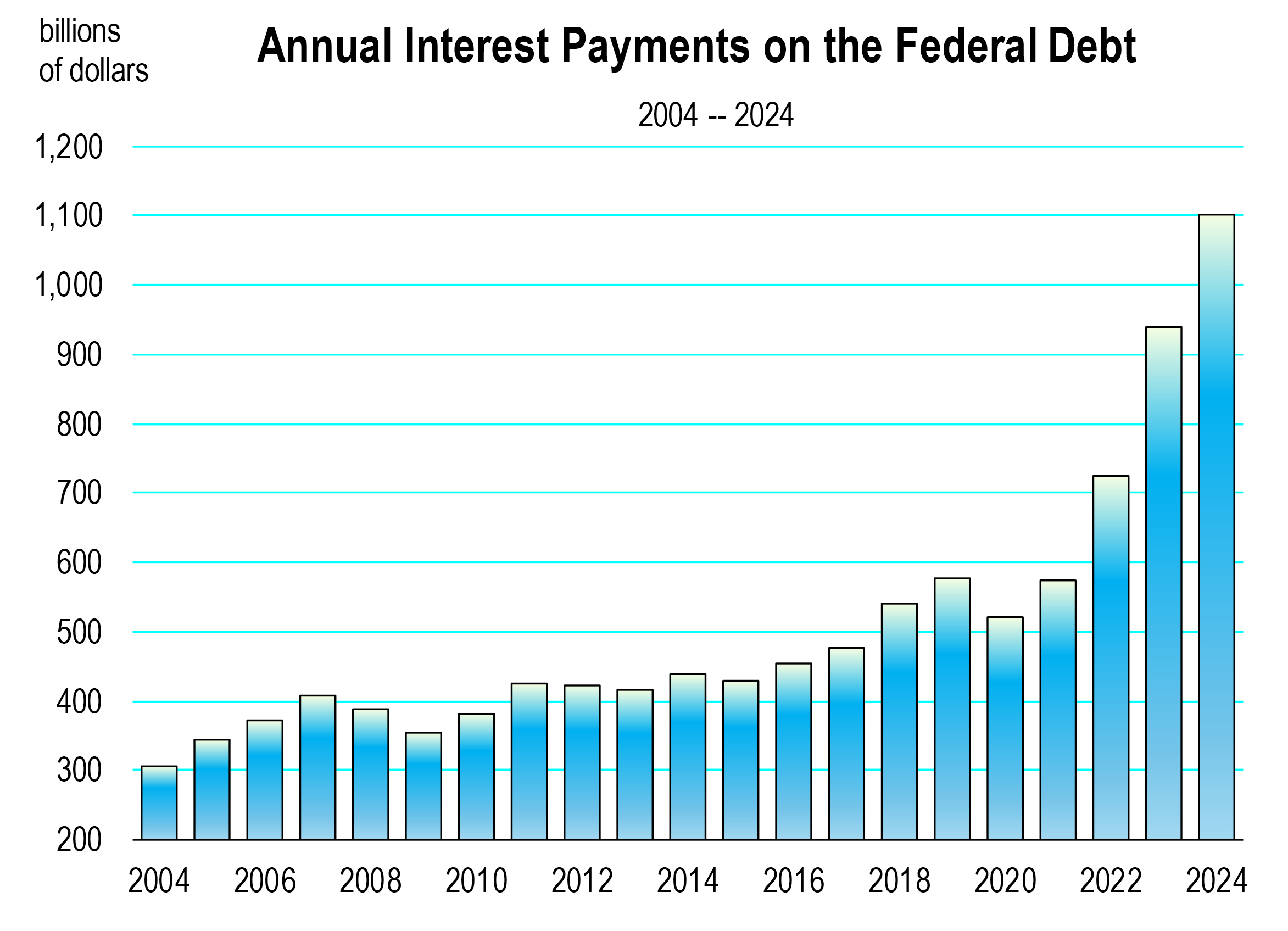

Tariffs at the current rate of 10 to 15 percent on all goods coming into the U.S. are generally manageable. Trump confirmed on July 28 that 15 percent represents the new standard for tariff negotiations. Furthermore, at the current rate of received tariff revenues to date, the federal government is on pace to collect $350 billion this year.

The policies to date would imply the average tariff rate is nearly 18 percent, far above the 2024 average of a just over two percent and the highest rate since the 1930s. As long as these significant tariffs are in place, the U.S. trade deficit should slowly but steadily start shrinking.

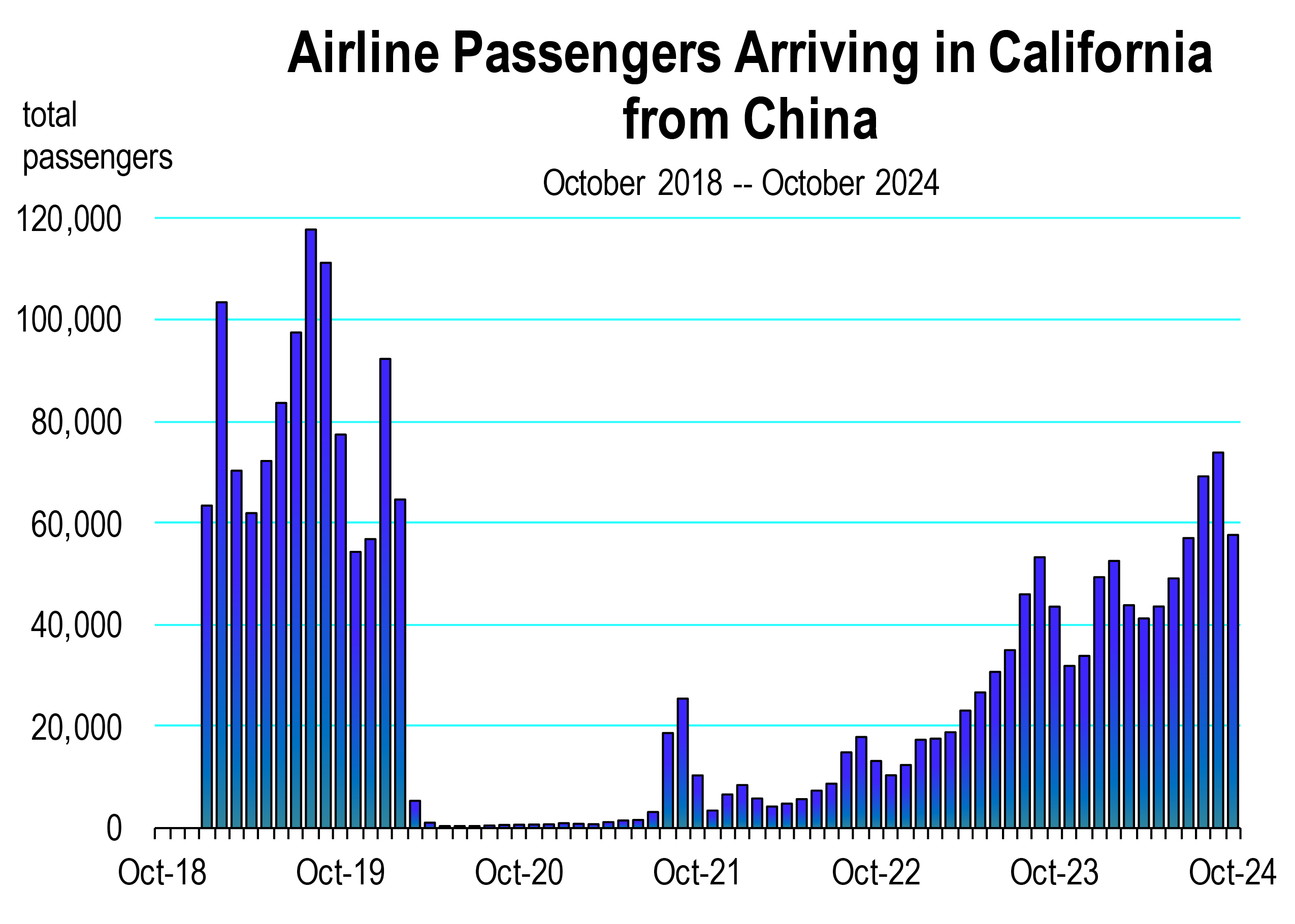

China faces an August 12 deadline to reach an agreement. Tariffs currently in place will likely add to higher export goods prices coming from China. However, we need to wait and see how the tariff structure and the corresponding response plays out.

Inflation is still an issue for the economy. The CPI for June still shows a 2.7 percent inflation rate over the last year. Fortunately, the 2025 calendar year trend for CPI inflation is decidedly down, but we still face tariffed goods coming into the U.S. and especially as the holiday season ramps up. Consumers may substitute successfully enough to avoid tariff inflated priced goods but this circumstance remains a wait and see.

Inflation is still an issue for the economy. The CPI for June still shows a 2.7 percent inflation rate over the last year. Fortunately, the 2025 calendar year trend for CPI inflation is decidedly down, but we still face tariffed goods coming into the U.S. and especially as the holiday season ramps up. Consumers may substitute successfully enough to avoid tariff inflated priced goods but this circumstance remains a wait and see.

I’m not concerned about recession this year. I’m not really concerned about the new tariff economy either. They will likely have a minimal impact on prices and consumer spending.

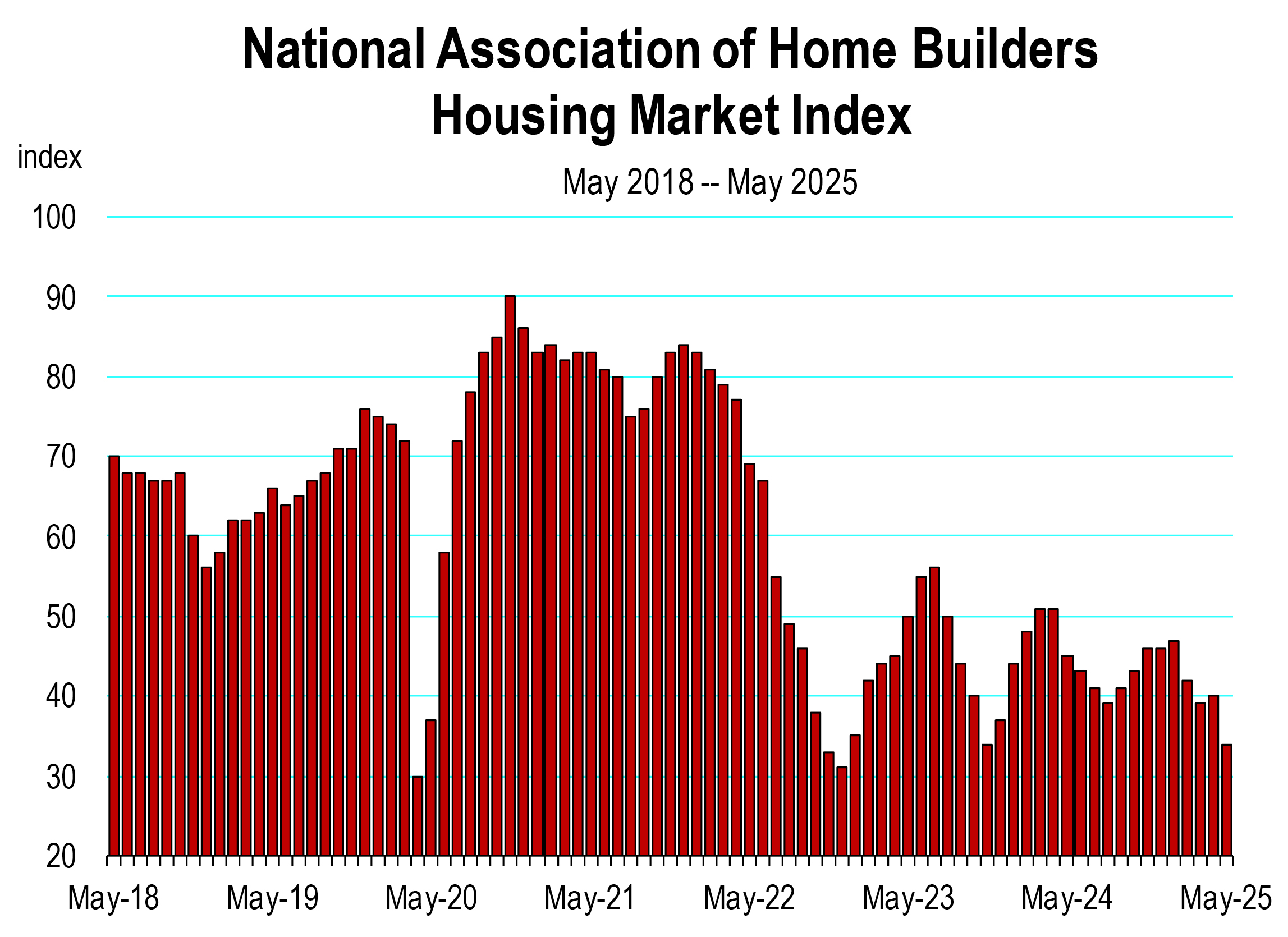

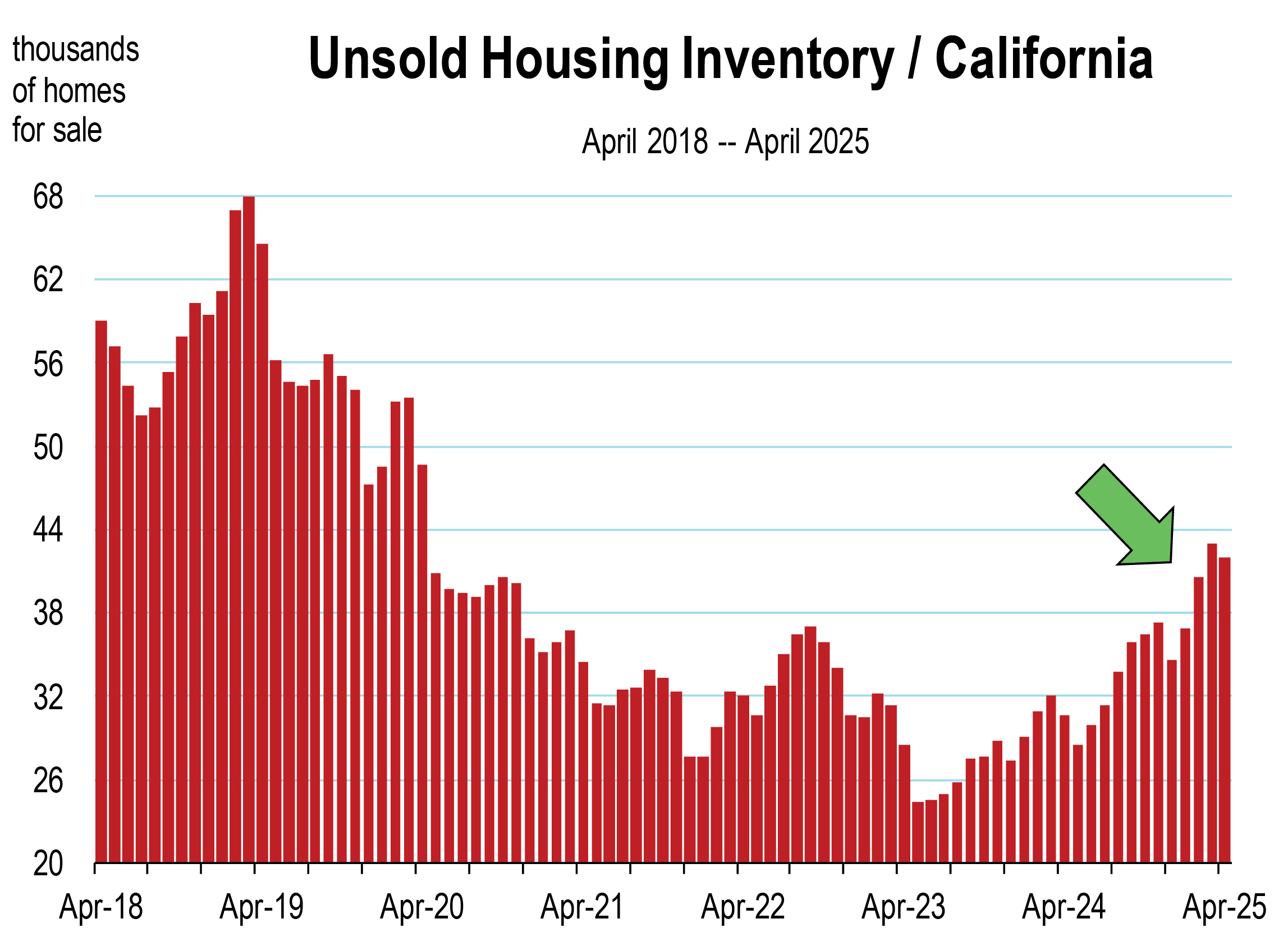

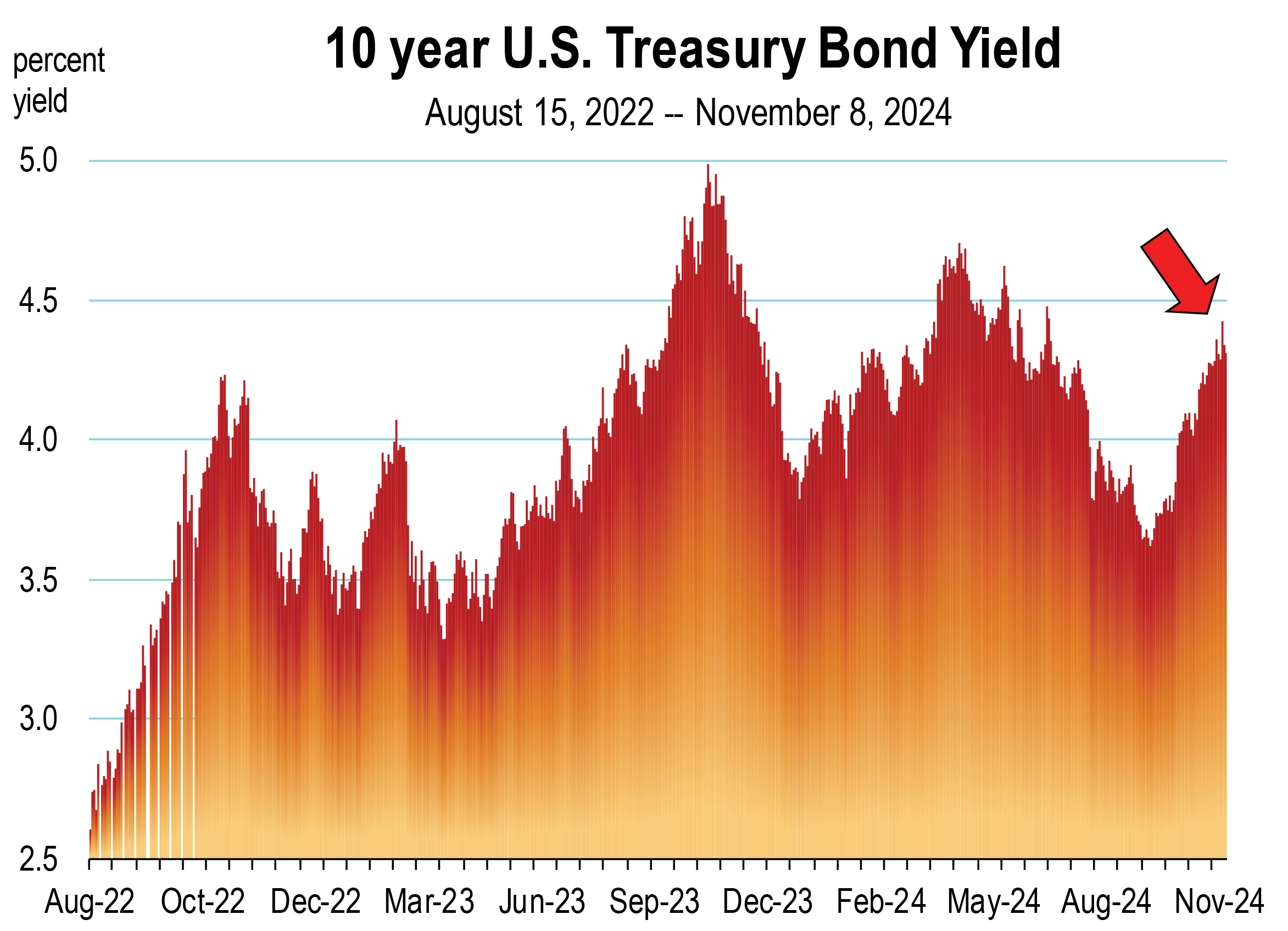

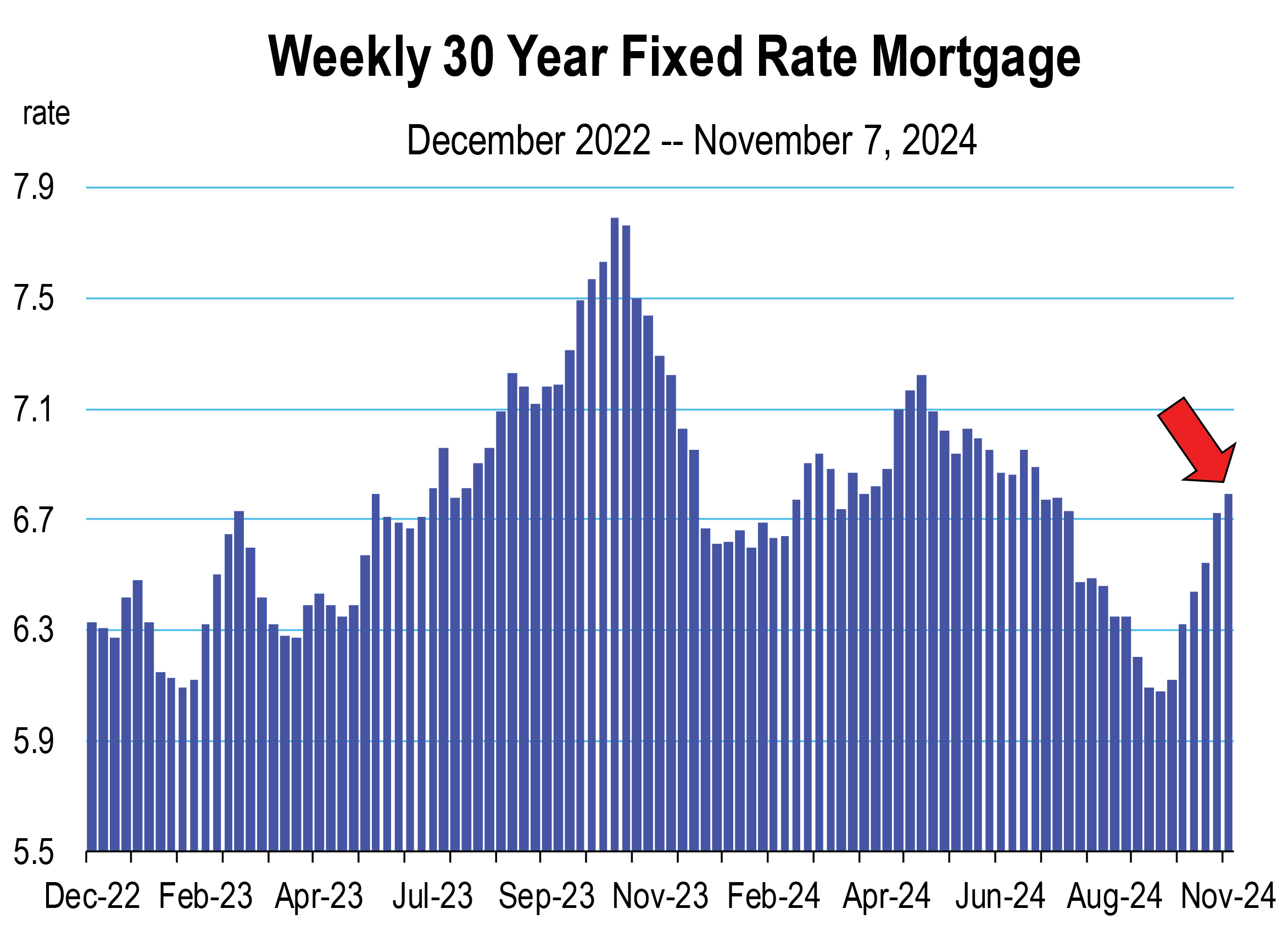

Higher interest rates are a problem for the housing market and less so, the car market. Some relief may be coming over the next 5 months but it won’t be much. Stay tuned for tariff and labor market updates. Inflation and whether unemployment rises will be the important assessment indicators for the rest of the year.

The California Economic Forecast is an economic consulting firm that produces commentary and analysis on the U.S. and California economies. The firm specializes in economic forecasts and economic impact studies, and is available to make timely, compelling, informative and entertaining economic presentations to large or small groups.

![]()

market.

market.

displace. Healthcare is the only private labor market that has consistently created jobs over the last 5 years. But even here, AI is now capable of replacing social workers, therapists, nursing assistants, and laboratory technicians. This will undoubtedly begin to reduce the rate of positive job growth that we’ve been observing in California healthcare since 2020.

displace. Healthcare is the only private labor market that has consistently created jobs over the last 5 years. But even here, AI is now capable of replacing social workers, therapists, nursing assistants, and laboratory technicians. This will undoubtedly begin to reduce the rate of positive job growth that we’ve been observing in California healthcare since 2020.

the rapid onset of AI which has been the case since 2023.

the rapid onset of AI which has been the case since 2023. California survey of respondents was optimistic regarding construction business activity in 2025. Nearly 63 percent of those surveyed expect modest growth in overall business activity this year.

California survey of respondents was optimistic regarding construction business activity in 2025. Nearly 63 percent of those surveyed expect modest growth in overall business activity this year. for construction materials along with unknown cost hikes due to tariffs has delayed project starts this year.

for construction materials along with unknown cost hikes due to tariffs has delayed project starts this year. the BART Silicon Valley tunneling project.

the BART Silicon Valley tunneling project.

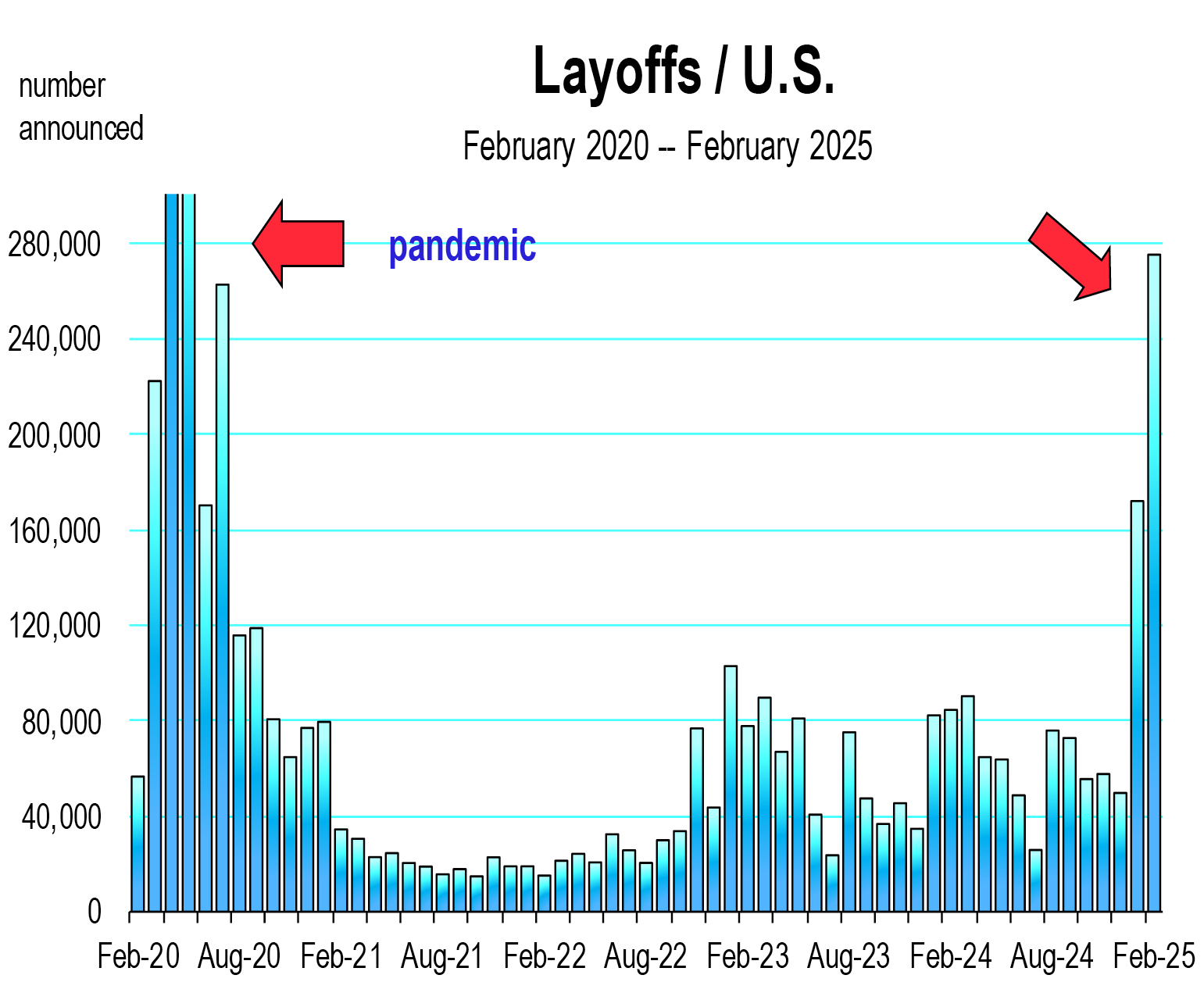

monthly Challenger Report on layoffs and the weekly unemployment insurance claim reports to monitor the possibility of higher rates of unemployment.

monthly Challenger Report on layoffs and the weekly unemployment insurance claim reports to monitor the possibility of higher rates of unemployment.

are largely unknown. Just how high and for how long will tariffs will be implemented, and will there be adequate and affordable substitution effects for consumers as alternatives to tariffed goods.

are largely unknown. Just how high and for how long will tariffs will be implemented, and will there be adequate and affordable substitution effects for consumers as alternatives to tariffed goods.

hiring, quits and layoffs in the labor market. In December, hiring and separations through quits or layoffs both increased. Though still at a modest level, the slower pace of layoffs (which remain historically soft) continue to ensure job growth. The unemployment rate for January slipped further, to 4.0 percent.

hiring, quits and layoffs in the labor market. In December, hiring and separations through quits or layoffs both increased. Though still at a modest level, the slower pace of layoffs (which remain historically soft) continue to ensure job growth. The unemployment rate for January slipped further, to 4.0 percent.

divert through the Panama Canal.

divert through the Panama Canal.

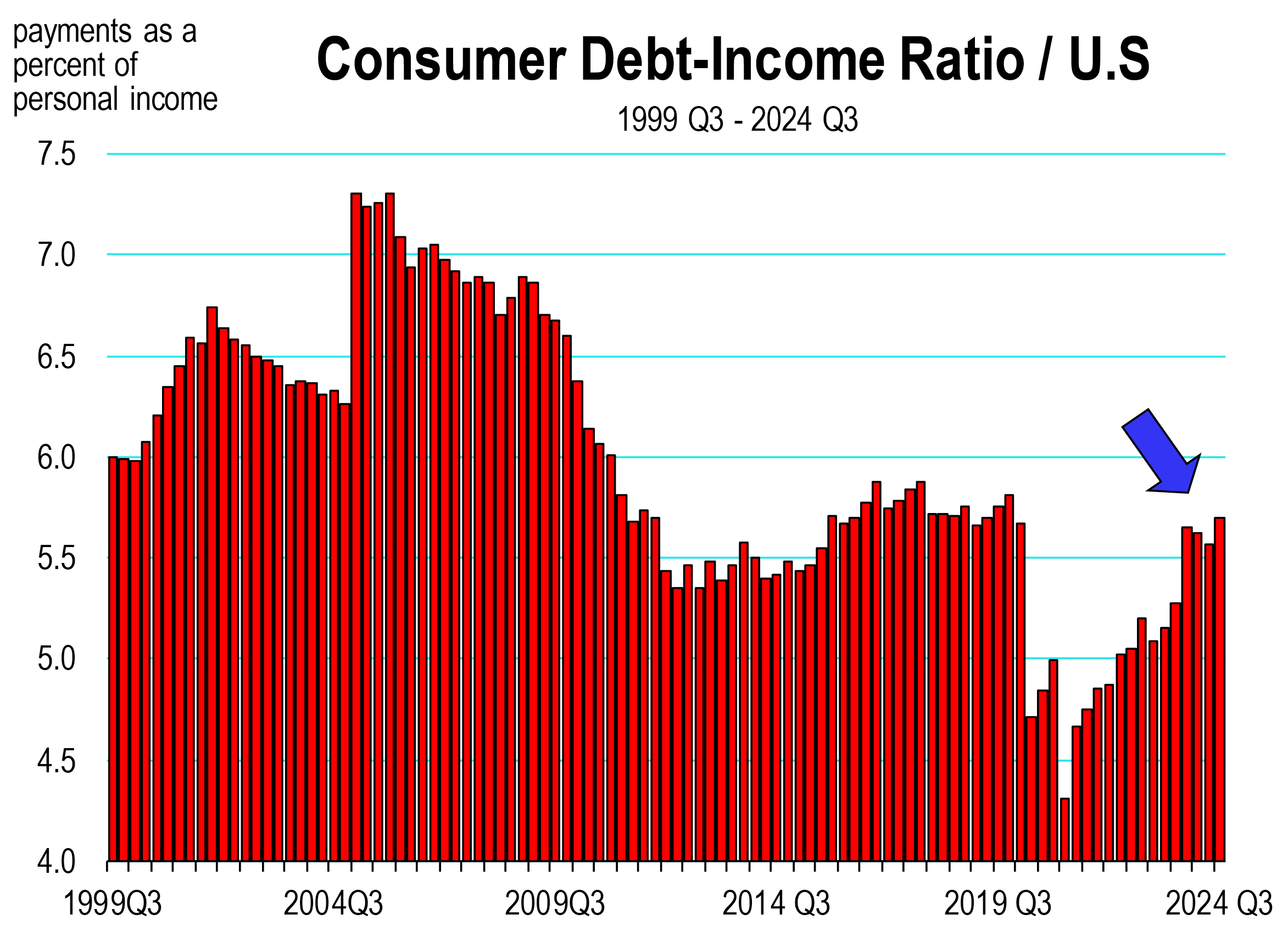

is up $4 billion from quarter 1. 24 million Americans have a personal loan. The 60-day delinquency rate for personal loans is 3.4 percent, the highest rate since 2012.

is up $4 billion from quarter 1. 24 million Americans have a personal loan. The 60-day delinquency rate for personal loans is 3.4 percent, the highest rate since 2012.