Mark Schniepp

April 11, 2023

The Chicken Little contingency is suggesting that the market and home prices are in a bubble-like condition, similar to 2008. There are a couple of very sound reasons why this will not take place. In 2008, low teaser mortgage rates required refinancing within 2-5 years. As rates increased, owners were forced to basically either abandon their properties to the banks or face foreclosure. They did not have equity in their homes, meaning there was nothing to protect. With negative equity, walking away was easy. Not so today.

— Chuck Lech, The Lech Report, March 6, 2023

During the housing bubble years of 2003-2007 which precipitated the Great Recession, the era of short term, variable rate, easy-to-qualify-for-mortgages has largely been replaced by down payments of 20 percent, and 30-year fixed mortgages with rigorous income verification. Most homeowners today have built up equity in their homes, have low interest rate mortgages and only one mortgage, and do not need to re-finance.

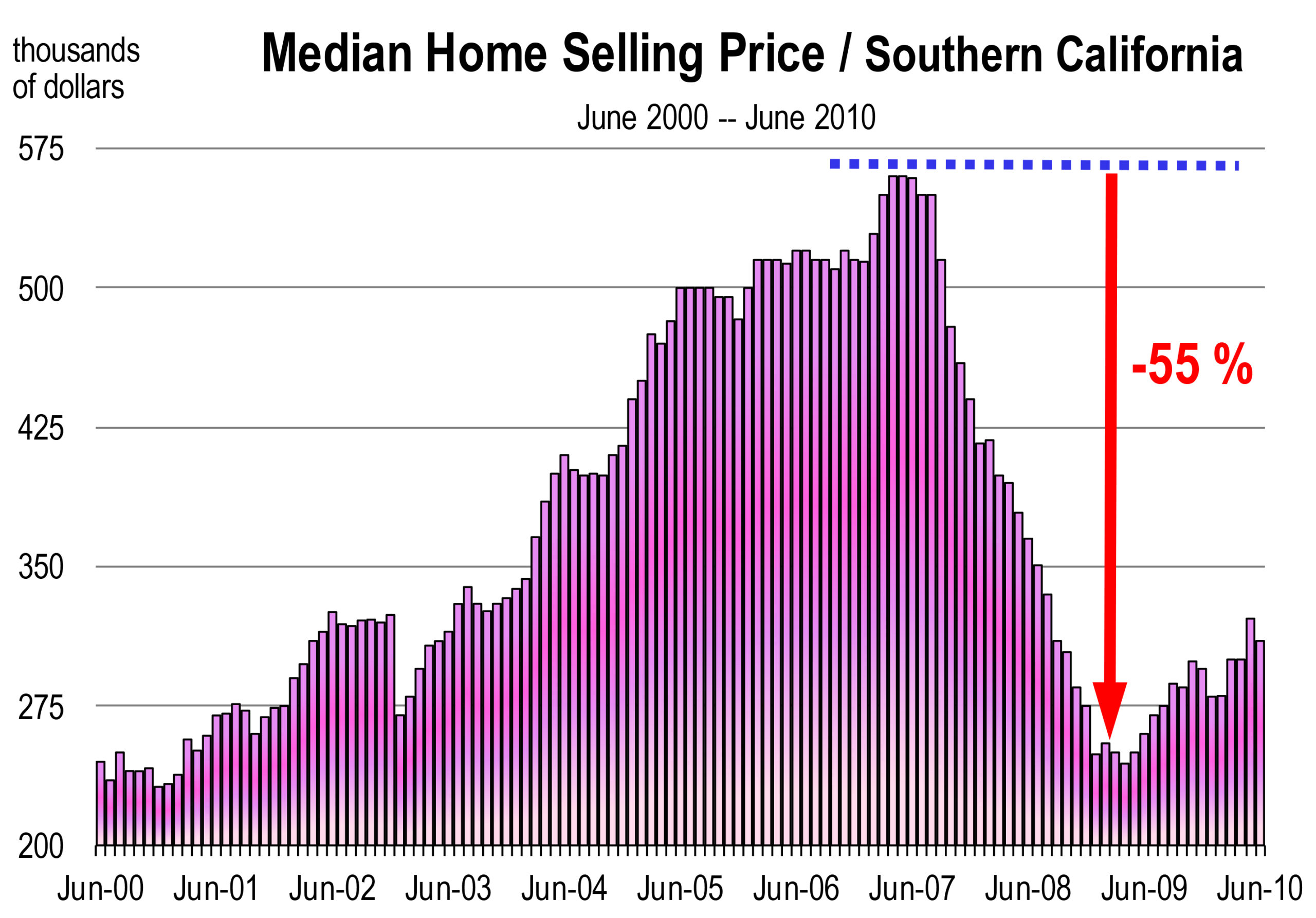

The housing market is now in recession as housing bears the impact of increased interest rates. Sales are off 40 percent and home prices are retreating again, but not like in 2008 or 2009 when values declined 30 to 60 percent across California.

The Price Correction to Date

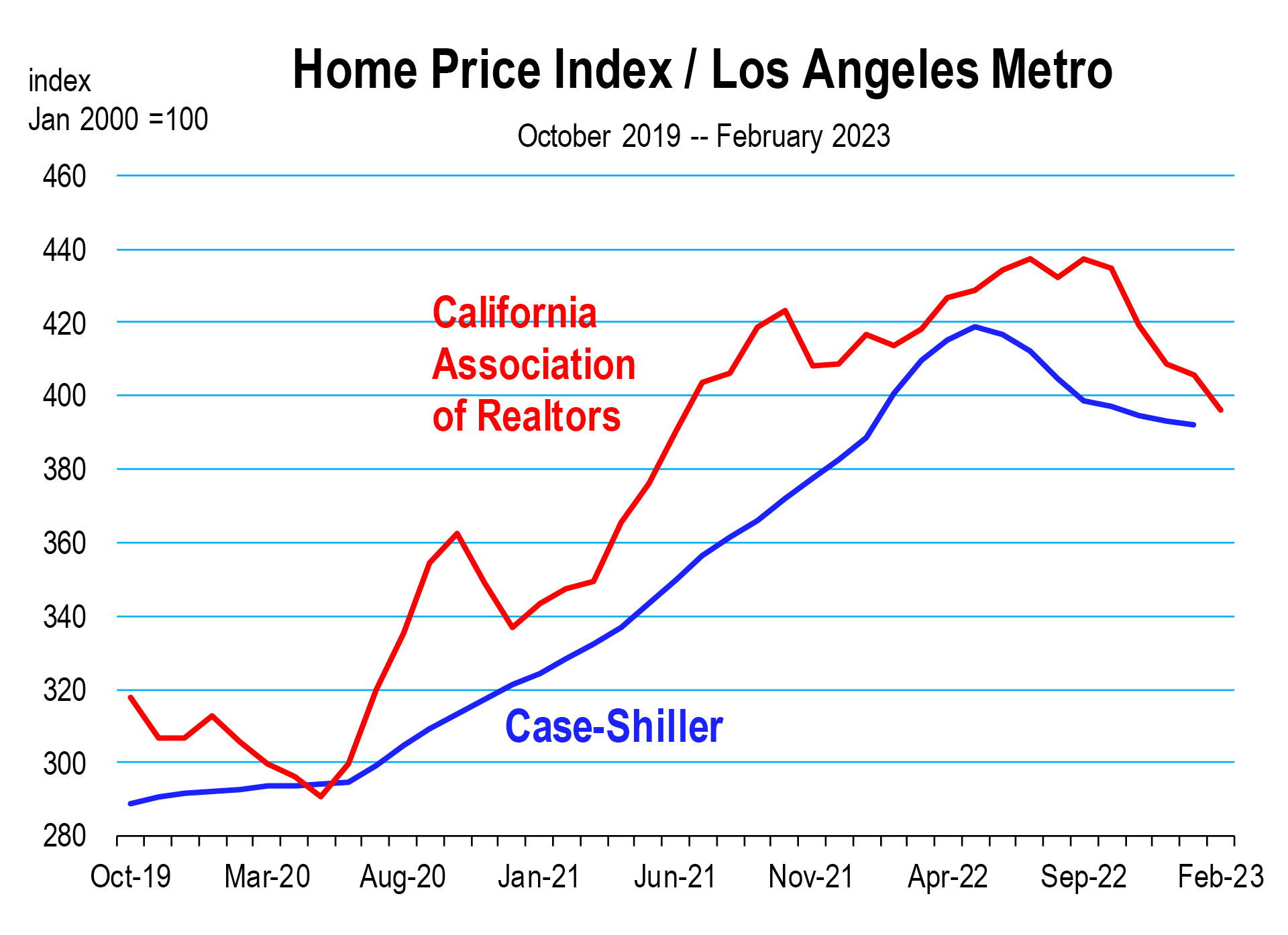

To date, the median price for a home in California has declined 18 percent from the peak month for selling value, which was May 2022. The Los Angeles County reported median selling price is 15.5 percent off the peak. And the San Francisco Bay Area median has plunged 35 percent.

However, confusing these reported price declines is the composition of homes that are selling. Currently, more lower priced homes are closing escrows relative to the sales mix in 2020, 2021, or early 2022. A mix of sales with a higher concentration of lower priced homes reduces the median price, but does not necessarily reduce the value of real estate proportionately.

Holding constant the sales mix (or the quality/size/location of the home), and evaluating how prices are actually declining for the asset, we turn to the Case Shiller housing index which espouses to track actual real estate values nationally and over time.

For the 20 largest cities combined, the price index is off only 5 percent from the peak in May 2022 to February 2023.

For the Los Angeles area, the index has declined 6.4 percent and San Diego County is down 8.3 percent. San Francisco shows the most severe price correction to date at 13.2 percent, not 35 percent as the California Association of Realtors reports. It should be noted that soaring price appreciation during the 2019 to 2021 period was more prevalent in the Bay Area than any other region of California. But now, with residents departing the Bay area in droves to Sacramento and the San Joaquin Valley, home prices are adjusting downward as a result of diminishing demand.

In 2009, the total decline in the Case Shiller price index for the Los Angeles Metro area was 41 percent. To date, it is off less than 7 percent. Consequently, we have a long way to go for price declines to match the trauma of the Great Recession.

It’s Actually Different This Time

Realistically, the pace of the rise in prices at 20 plus percent per year was unsustainable. The markets from late 2020 through the first half of 2022 were similar to what happened just ahead of the Great Recession when home prices were accelerating at a similar pace. But other than for that, today’s market is quite dissimilar from the bubble days of 2005-2007. Consider the following:

- In 2006, the percent of California buyers with no down payment was 21 percent. Today, it is less than 3 percent.

- The percentage of home buyers who purchased with a second mortgage was 43 percent in 2006. Today it is less than 2 percent.

- Adjustable rate mortgages accounted for 33 percent of all purchases in 2006. Today they account for 2 percent.

- There are nearly twice as many all-cash buyers today than in 2006.

- Lending criteria are much stricter today and have not loosened up much since the abuses during the bubble years. A buyer needs to have a down payment, verifiable income, and a minimum credit score that is higher today than in 2006.

A Welcome Change

Not only the slowing of home price growth but a reversal of home prices is actually a welcome change to the market because it will bring more balance to the transaction between buyers and sellers, resulting in healthier housing market conditions. It will also increase the affordability of homes in California, expanding the domain of potential buyers who might otherwise defect from the state. This has been the circumstance currently driving the substantial volumes of out-migration in 2021 and 2022.

Vulnerabilities

A looming vulnerability is rising household debt. If the impending recession unleashes unexpected trauma in the labor markets, workers become unemployed and their household debt levels would rise along with the likelihood of home foreclosures.

The onset of foreclosures would increase housing supply, amid rapidly evaporating demand, and crash home prices further. This could spiral out of control as it did in 2008 and 2009.

Layoffs would have to become pervasive leading to rising unemployment, other than just prevalent leading to a rapid rehire as they are today. The risk is there but it’s low, as most economists expect a mild recession with very little attendant labor market calamity.

The California Economic Forecast is an economic consulting firm that produces commentary and analysis on the U.S. and California economies. The firm specializes in economic forecasts and economic impact studies, and is available to make timely, compelling, informative and entertaining economic presentations to large or small groups.

![]()