by Mark Schniepp

October 7, 2021

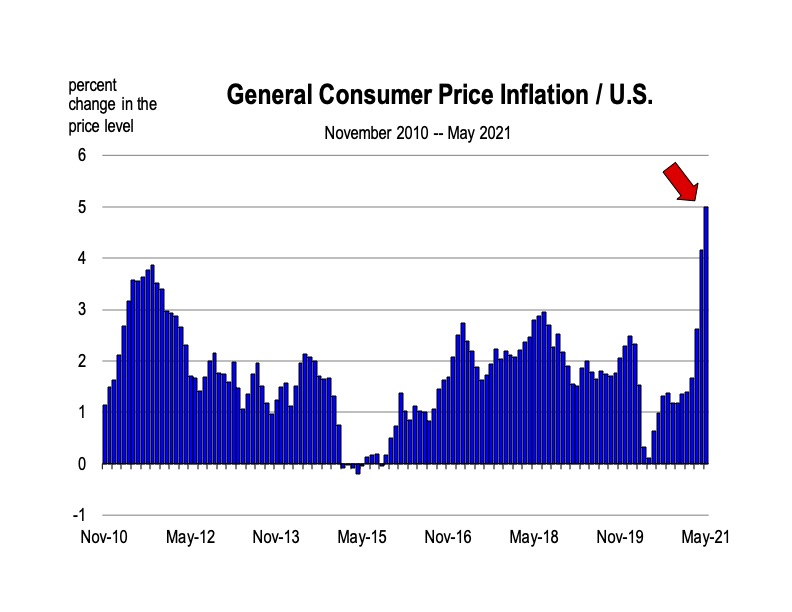

Global supply disruptions continue to hamper the U.S. economy, contributing to the acceleration of inflation. It doesn’t take a rocket scientist to notice the clear evidence that supply-chain issues are creating economic costs.

Global supply disruptions continue to hamper the U.S. economy, contributing to the acceleration of inflation. It doesn’t take a rocket scientist to notice the clear evidence that supply-chain issues are creating economic costs.

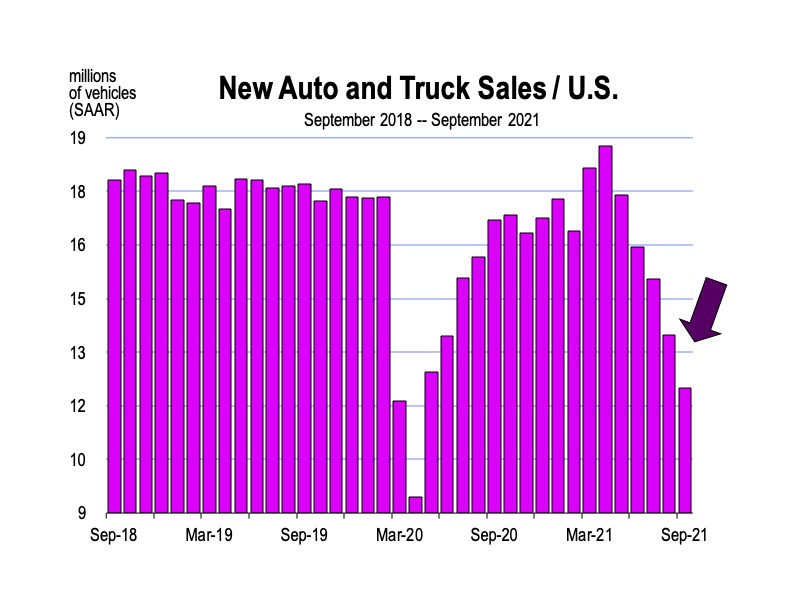

Looking at this chart of new U.S. vehicles sales each month through September, you’d think that consumer demand for autos was falling like a rock. Normally that’s what tends to drive the variation in this series. This time however, it’s a supply issue, indicative of many product supply constraints today.

Usually, cars are like Doritos—they can always make more—but cars utilize semi-conductors to run most of their internal and external systems. And now there is a semiconductor supply issue from Asian producers, due to intermittent factory shutdowns because of COVID-19, limiting production.

A spate of supply “shortages” emerged when ocean carrier sailings were cancelled, manufacturing capacity was cut, and workers everywhere were displaced. Circumstances where the growth of demand for a product is outpacing the growth of supply—and this includes the scenario where the normal volume of supply has been interrupted—manifest as shortages. The latter circumstance has pushed prices higher, adding to the surge in inflation this year.

Many products that we import—including coffee and Nike shoes—are further delayed into seaports because of problems with ships and containers. The world-wide pandemic-induced demand for PPE rerouted containers and ships about the globe, or shut down ships entirely during much of 2020. These particular outcomes have interrupted shipping schedules and the normal supply of shipping containers. Factory shutdowns or dockworker quarantines due to coronavirus outbreaks further exacerbated the supply issues.

The Great Shipping Debacle

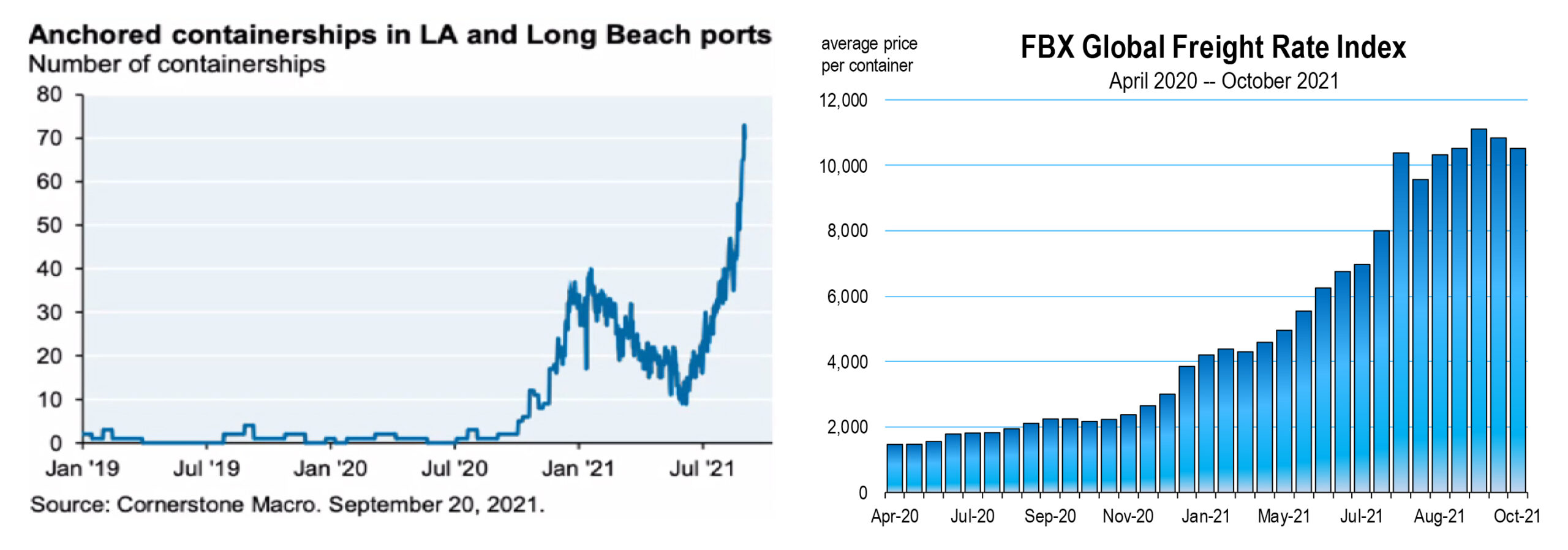

Dozens of mega-container ships are waiting off the coast of Los Angeles to dock at the Ports of LA and Long Beach. The route into San Pedro Bay accounts for about one-third of all US imports, and the backlog is causing ships to wait weeks to dock and unload. The mega-ships take much longer to unload, and they carry millions of dollars worth of furniture, auto parts, clothes, electronics, and plastics. Backlogs in most of these goods are seriously piling up.

As of late September, more than 70 container ships are anchored in the San Pedro Bay, a record number. The lack of having all of the goods unloaded at the Ports and transported to markets results in (1) shortages of products, and (2) rising prices for these goods to alleviate the shortages.

Thousands of containers are still stuck in unfamiliar routes or are stuck on ships waiting to unload. Fewer containers are in normal circulation which is causing the existing container supply to rise steeply in price as companies compete for them.1

Container prices have quadrupled or quintupled in one year. Rising container prices increase the cost of shipping, which increases the end-product costs to consumers. Container prices will ultimately normalize but it will take time.

The largest question bankers, economists, and company CEOs can’t answer with certainty is this: Are the shortages and delays merely temporary mishaps accompanying the resumption of business, or something more insidious that could last well into next year?

Consumers who continued to consume through the pandemic exhausted inventories of goods that the idled factories and delayed ships were unable to replenish. This rate of consumption continues today. We originally assumed that factories would catch up and ships would work through the backlog in a few months.

Not so. Coronavirus-related closures of key ports in Asia, the intermittent factory shutdowns, and the delayed unloading of waiting container ships has extended the catch-up period.

Now with Christmas approaching, consumer demand for goods will accelerate, creating further competition for limited supplies carried by the crippled supply chain, which will further add pressure on prices. This is demand-pull inflation. And it is likely to persist at least into next year.

Trucking

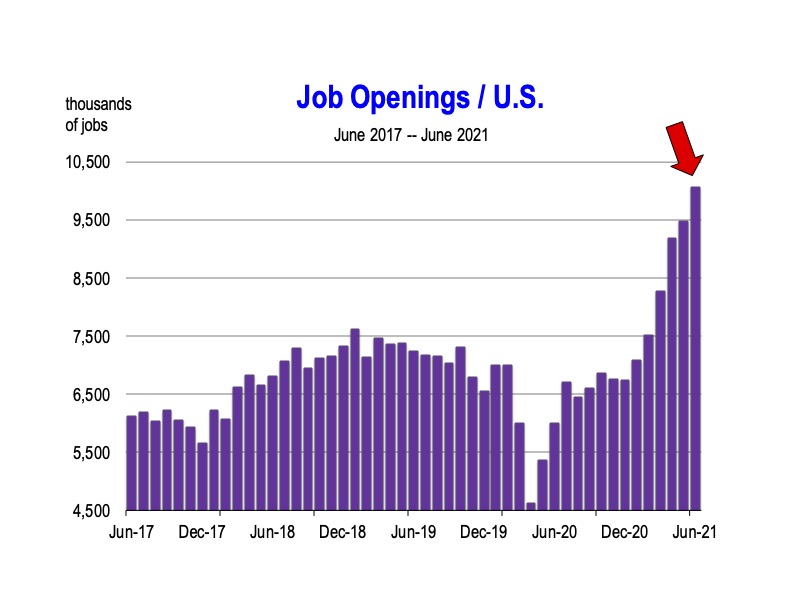

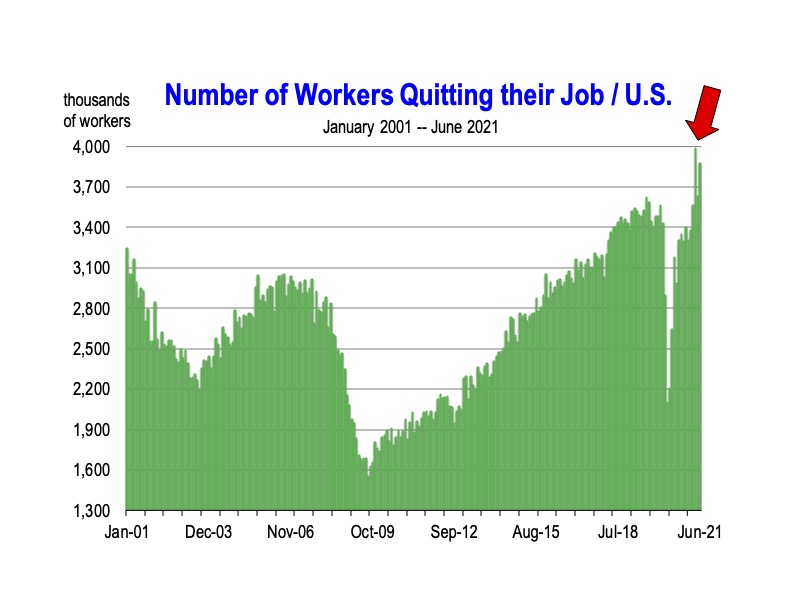

The primary source of container transport when the cargo is unloaded is trucking. A “shortage” of drivers translates into container volume that does not get moved to its destination on time. The driver workforce has been reduced by safety concerns, care giving priorities at home, expanded unemployment benefits, and other job openings offering a better lifestyle.

Wages are rising sharply, but the process to lure (and/or train) enough workers back into the industry will be lengthy. The truck driver shortage may be the most acute of bottlenecks in the supply chain, and it does not bode well for a rapid resolution of the overall disruption.

Delta

The bite of the Delta variant on the economy is easing. New infections and hospitalizations have dropped as the worst of the current coronavirus wave is clearly receding.

But it’s likely that Delta extends the supply-chain issues, particularly for semiconductors. Though there are a significant number of shortages now, domestic production for a number of them are improving, and this should ease some price pressures soon. The Delta variant still creates some upside risk to inflation. If the highly transmissible strain prompts fewer workers to return to the labor force, it may require businesses to further bid up wages and pass on the extra labor cost to consumers. This is cost push inflation, which is difficult to address with either fiscal or monetary policy.

Consequently, we need infections to abate, the economy to remain open, and the labor force to expand to avert the vagaries of cost push inflation, which is the more pernicious form of inflation, and can lead to stagflation.

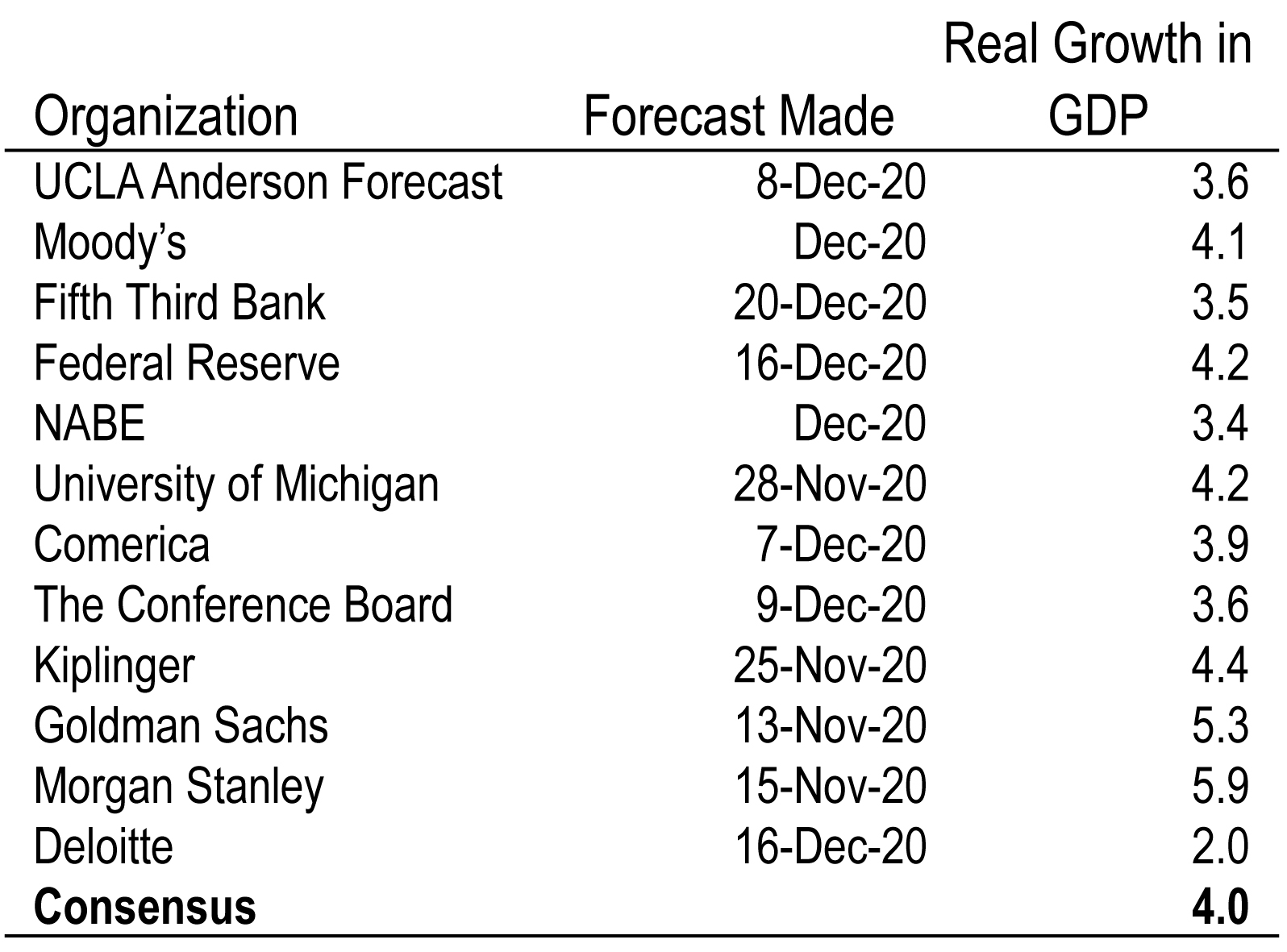

GDP estimates for the third quarter have been scaled downward, but not sharply. The annualized rates are now between 3.3 and 3.9 percent, and rising to 4.3 percent in the fourth quarter, the period we are currently in now.

1 When the Suez Canal was blocked in March by the Ever Grand, it stranded thousands of containers and caused backlogs and delays in shipping schedules that lasted months. Vessels had to wait for the canal to open or take a much longer route around Africa. The shutdown of a key port in southern China in May and June left approximately 350,000 containers idle.

The California Economic Forecast is an economic consulting firm that produces commentary and analysis on the U.S. and California economies. The firm specializes in economic forecasts and economic impact studies, and is available to make timely, compelling, informative and entertaining economic presentations to large or small groups.

![]()

by Mark Schniepp

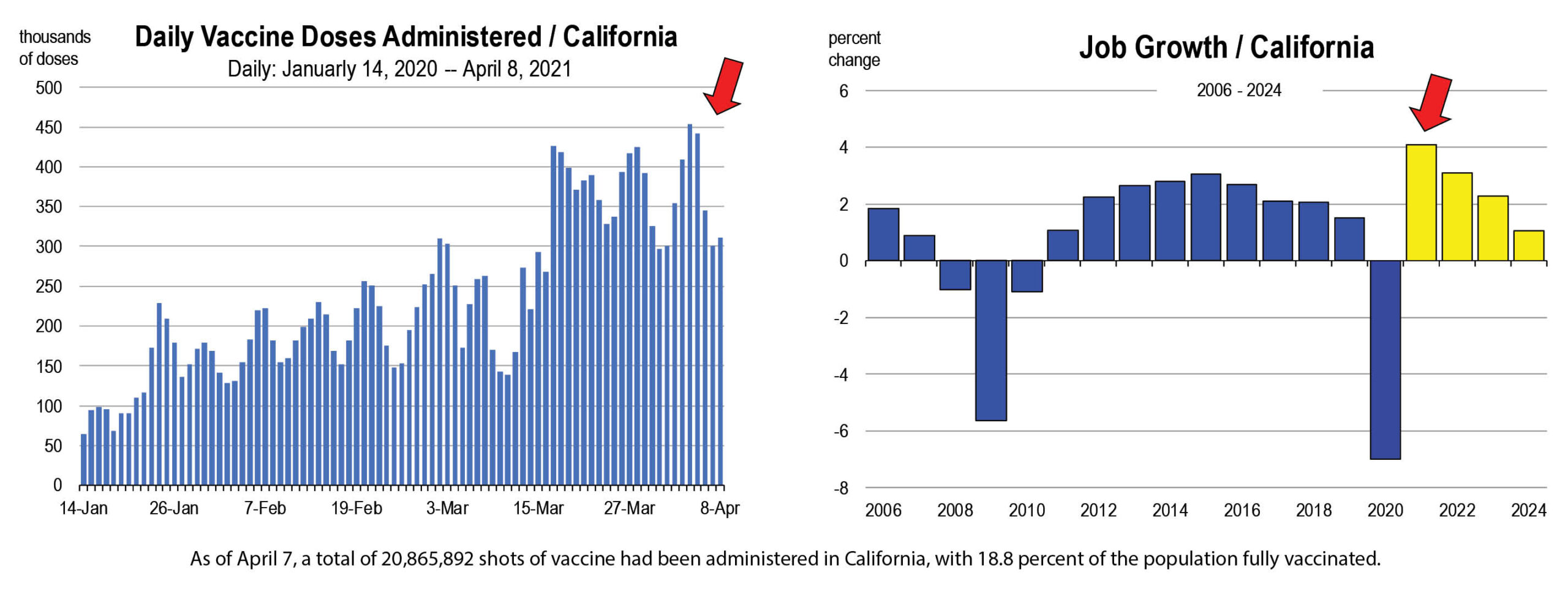

by Mark Schniepp The impact on the economy of California was more significant than the rest of the nation but the recovery will progress at a faster pace, catching up to the U.S. by 2023.

The impact on the economy of California was more significant than the rest of the nation but the recovery will progress at a faster pace, catching up to the U.S. by 2023. The Great Resignation

The Great Resignation Remote work and virtual meetings will continue

Remote work and virtual meetings will continue by Mark Schniepp

by Mark Schniepp

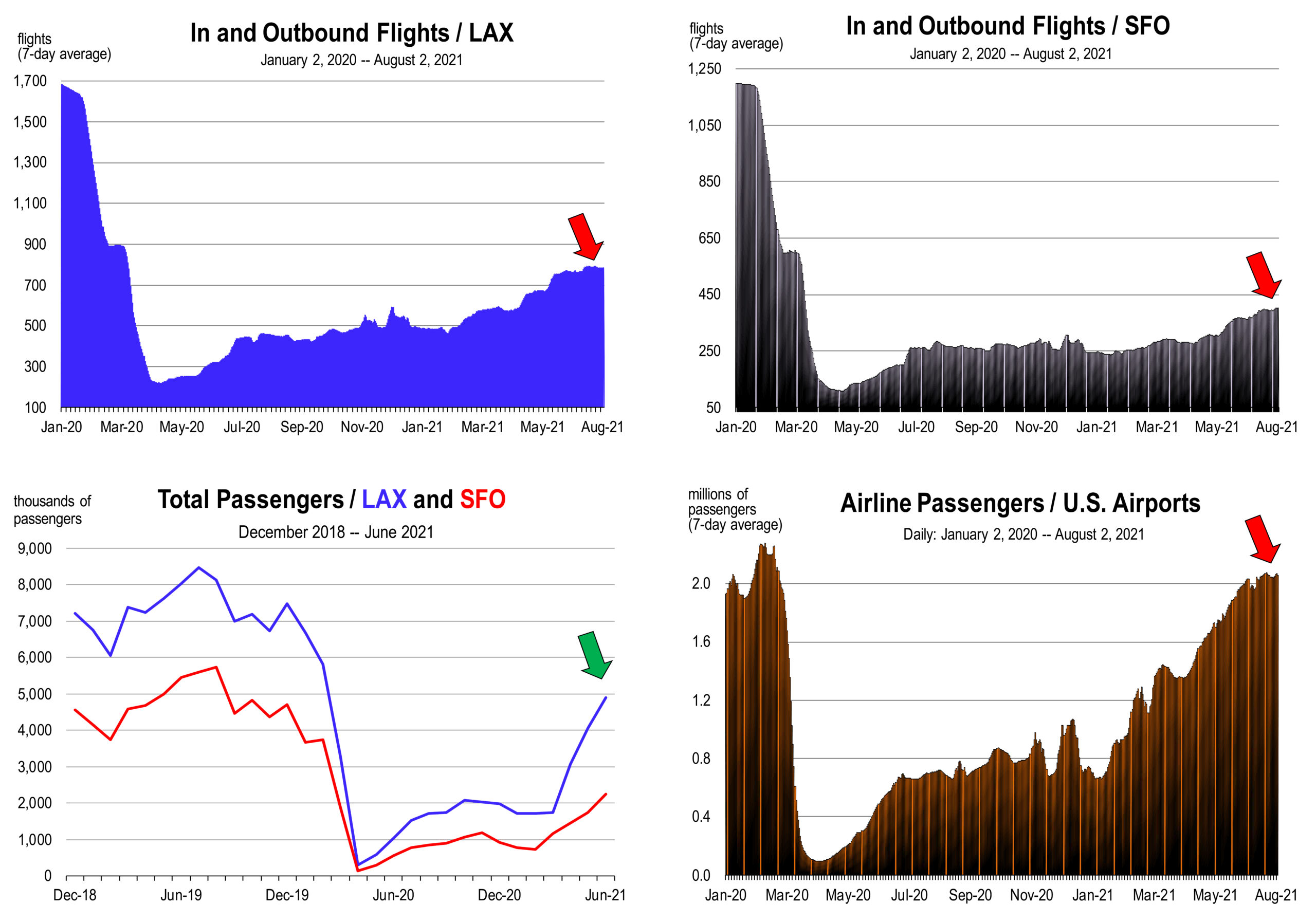

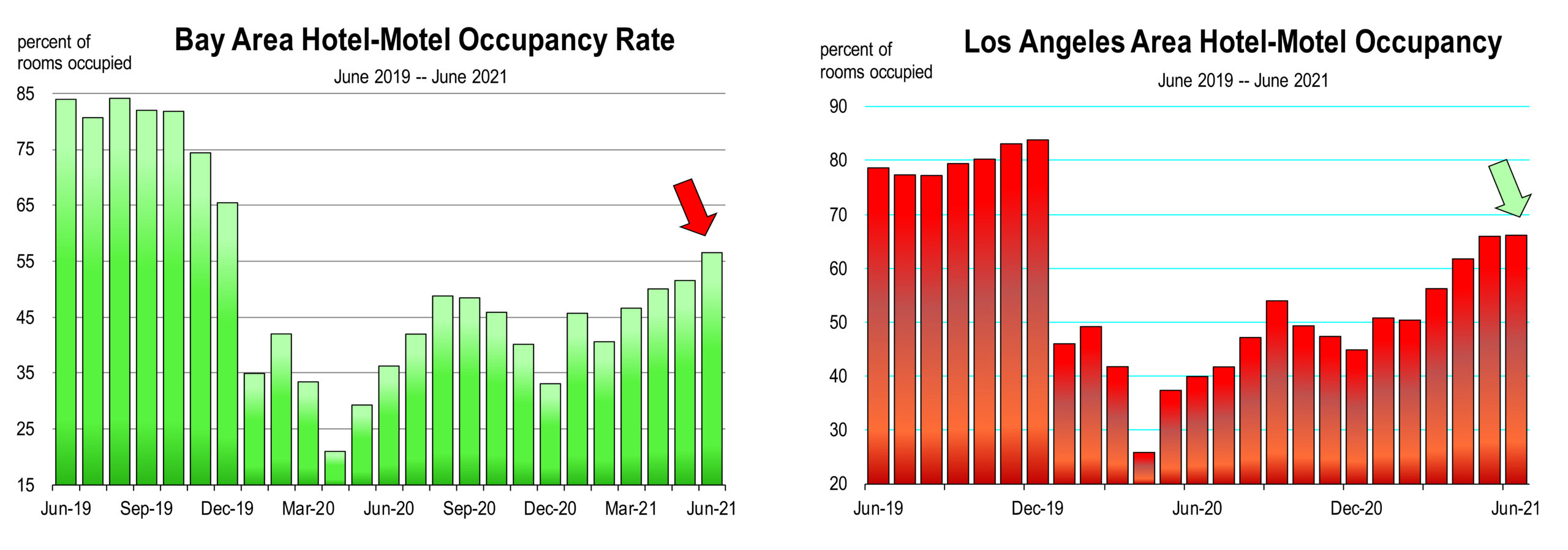

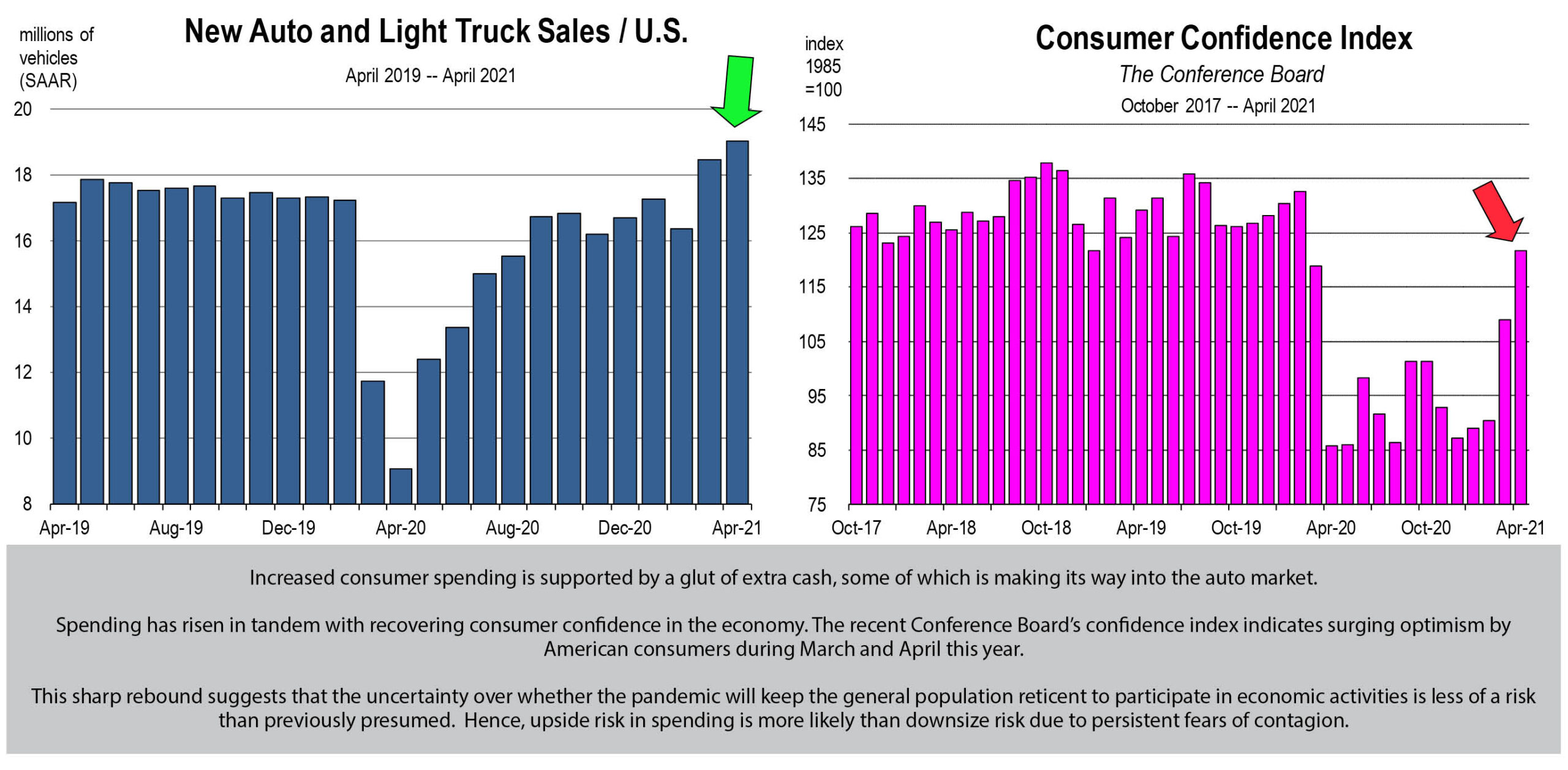

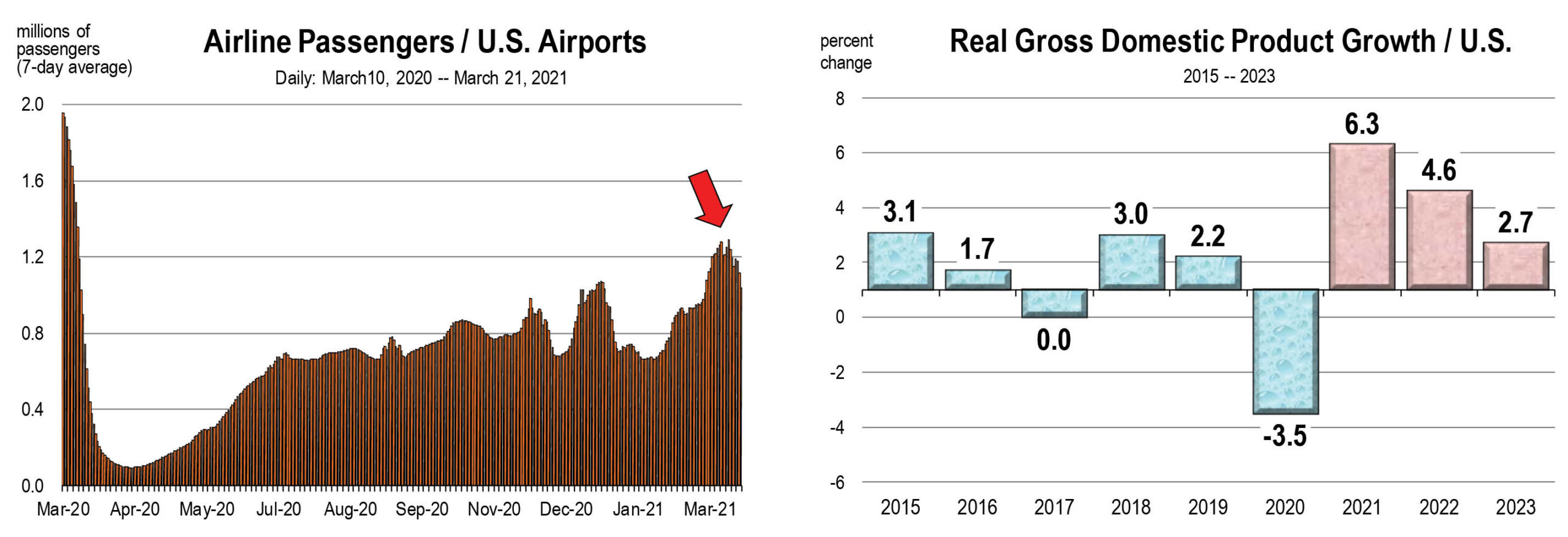

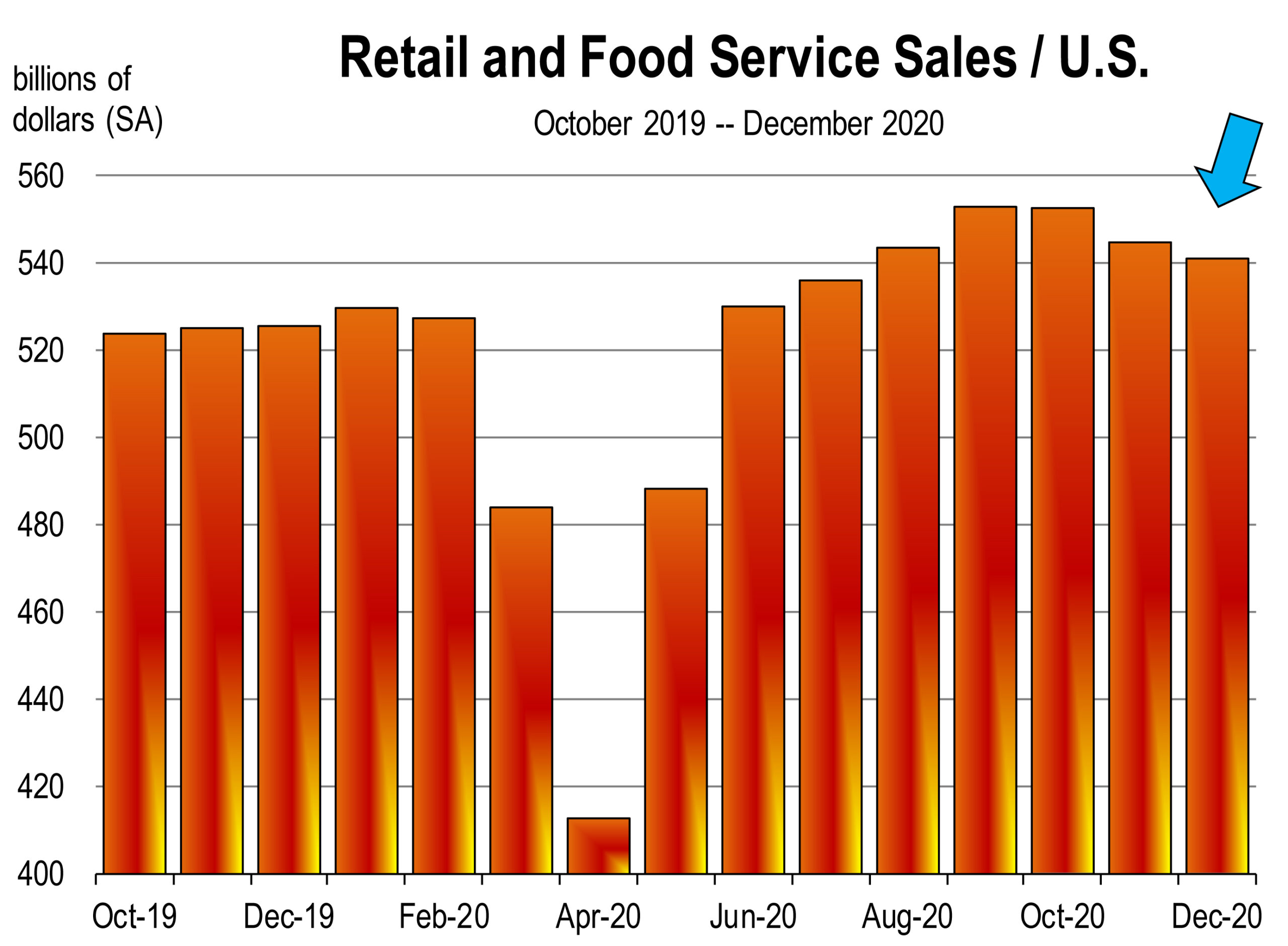

While air passenger travel in California has recovered 66 percent, passenger travel nationwide has recovered nearly 80 percent, and the clear increase in travel has produced higher hotel-motel occupancy rates.

While air passenger travel in California has recovered 66 percent, passenger travel nationwide has recovered nearly 80 percent, and the clear increase in travel has produced higher hotel-motel occupancy rates.

Travel related price increases are very likely catchup from the steeply discounted prices offered a year ago when no one was traveling anywhere.

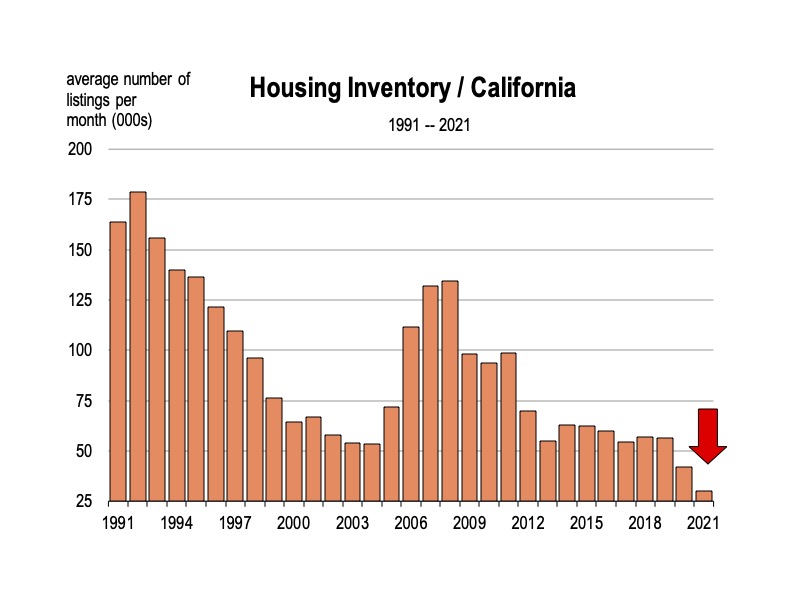

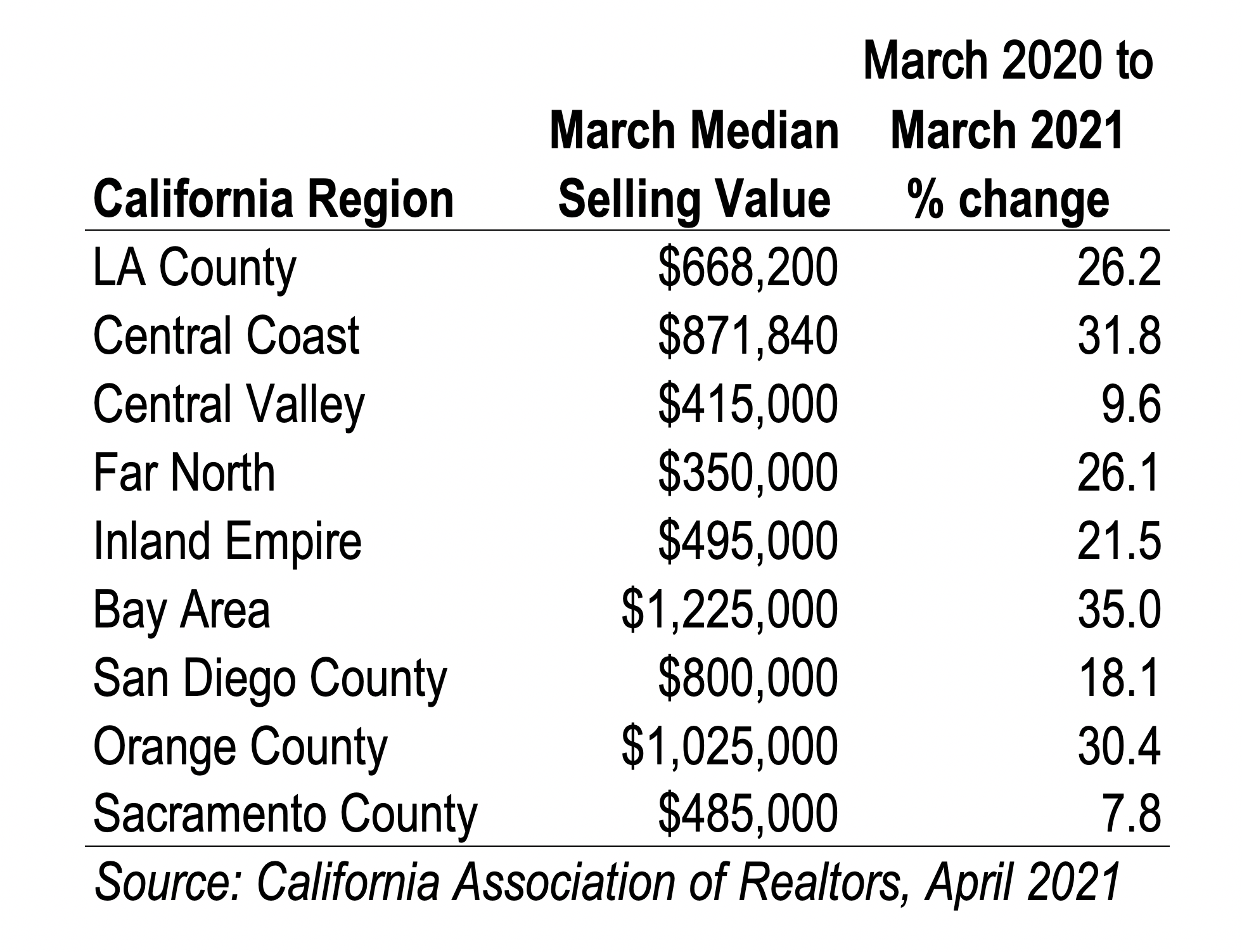

Travel related price increases are very likely catchup from the steeply discounted prices offered a year ago when no one was traveling anywhere. Only 1.16 million homes were on the market in April, a 20 percent drop from a year ago, according to the National Association of Realtors. In California, over the last 6 months, inventory levels have declined to their lowest on record.

Only 1.16 million homes were on the market in April, a 20 percent drop from a year ago, according to the National Association of Realtors. In California, over the last 6 months, inventory levels have declined to their lowest on record. What will be different?

What will be different? As the labor force rebounds, so will jobs in food services, hospitality and entertainment. As international travel resumes, larger gains are expected.

As the labor force rebounds, so will jobs in food services, hospitality and entertainment. As international travel resumes, larger gains are expected. New construction is underway all over Los Angeles, including LAX. The high-speed rail project continued through the pandemic and employs more workers now than at any other time. Large multi-family building projects have resumed in San Francisco and Sacramento. In downtown Los Angeles, they never stopped.

New construction is underway all over Los Angeles, including LAX. The high-speed rail project continued through the pandemic and employs more workers now than at any other time. Large multi-family building projects have resumed in San Francisco and Sacramento. In downtown Los Angeles, they never stopped. A return to normal

A return to normal Early spring and it’s all good news at this point. Though the improvement in the U.S. economy this year was expected, the actual levels of growth are better than anticipated.

Early spring and it’s all good news at this point. Though the improvement in the U.S. economy this year was expected, the actual levels of growth are better than anticipated.

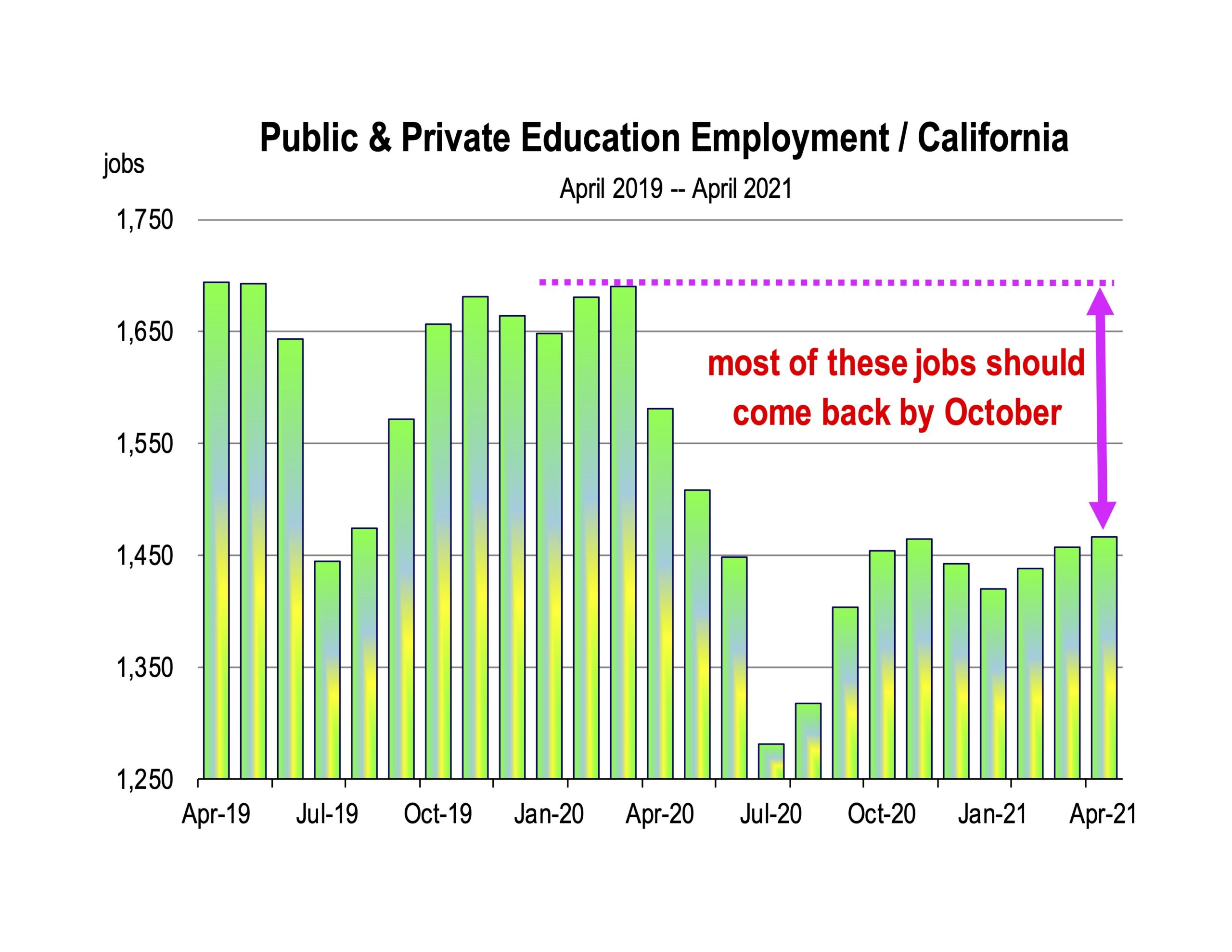

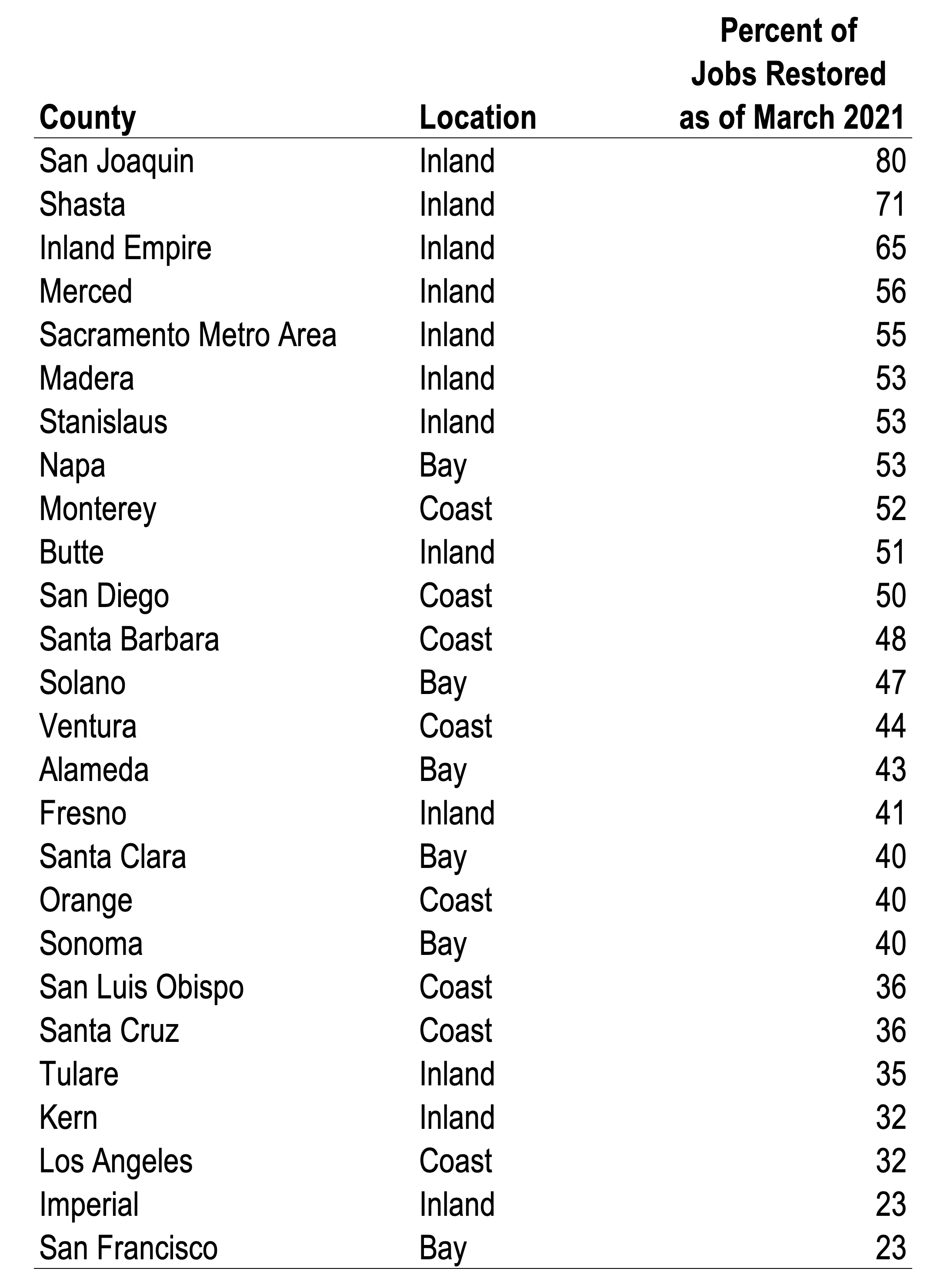

Through April 2021, the recovery is geographically uneven across the state, with inland counties reinstating their workforces faster than coastal counties or the Bay Area.

Through April 2021, the recovery is geographically uneven across the state, with inland counties reinstating their workforces faster than coastal counties or the Bay Area. We look forward to June

We look forward to June

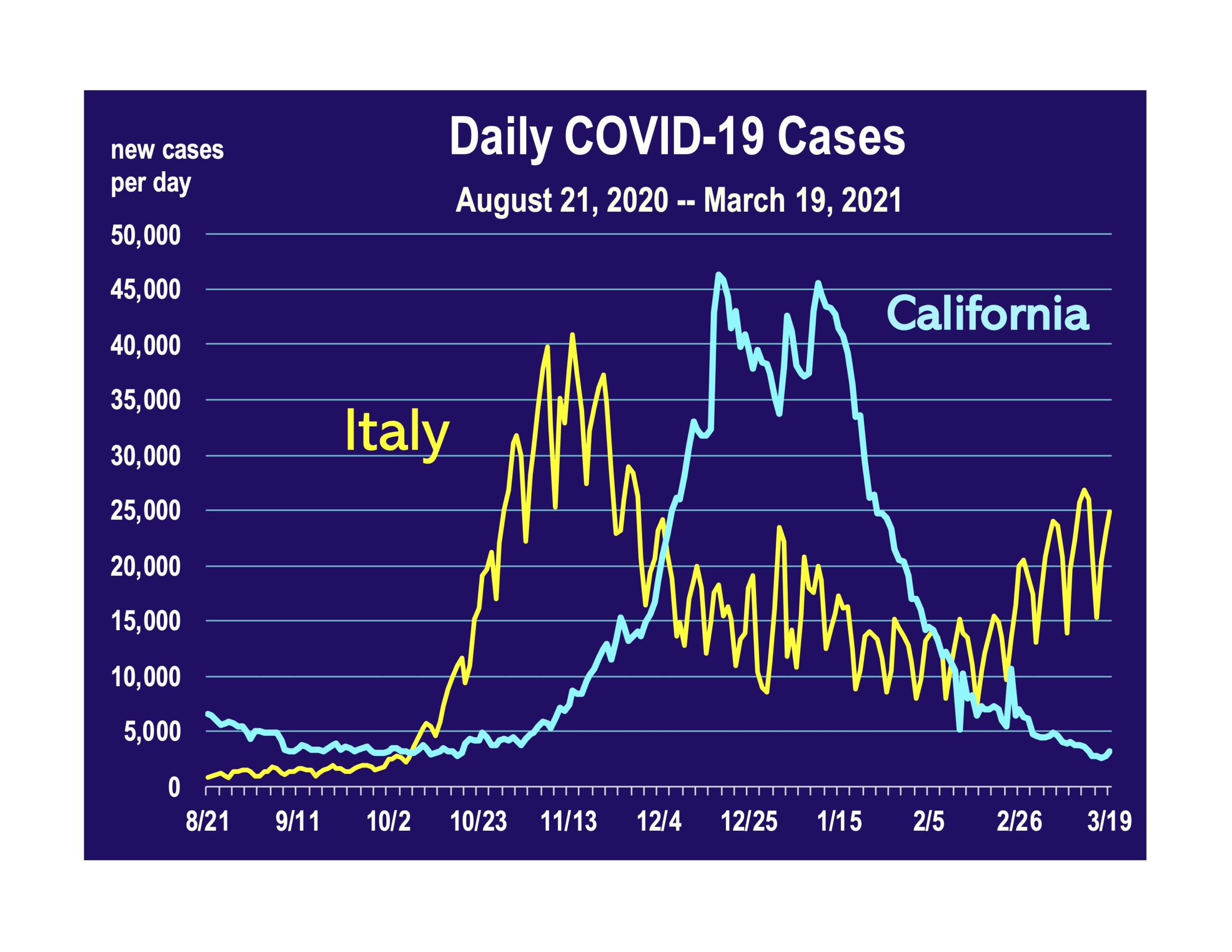

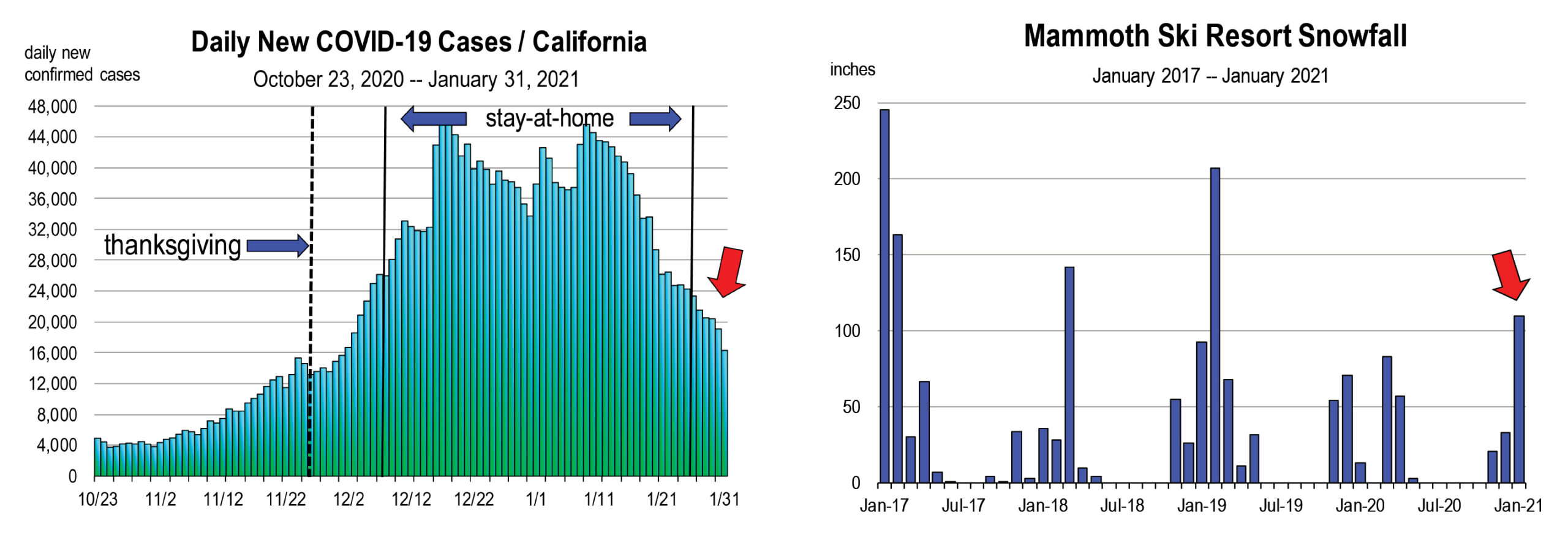

This possibility exists, and infectious disease experts from major universities in California are predicting the onset of another surge—at the end of March or beginning of April. If the European Union is a precursor to the path of the coronavirus in California, then another surge is likely, unless the vaccine can interrupt what has been a reliable predictor of past surges.

This possibility exists, and infectious disease experts from major universities in California are predicting the onset of another surge—at the end of March or beginning of April. If the European Union is a precursor to the path of the coronavirus in California, then another surge is likely, unless the vaccine can interrupt what has been a reliable predictor of past surges.

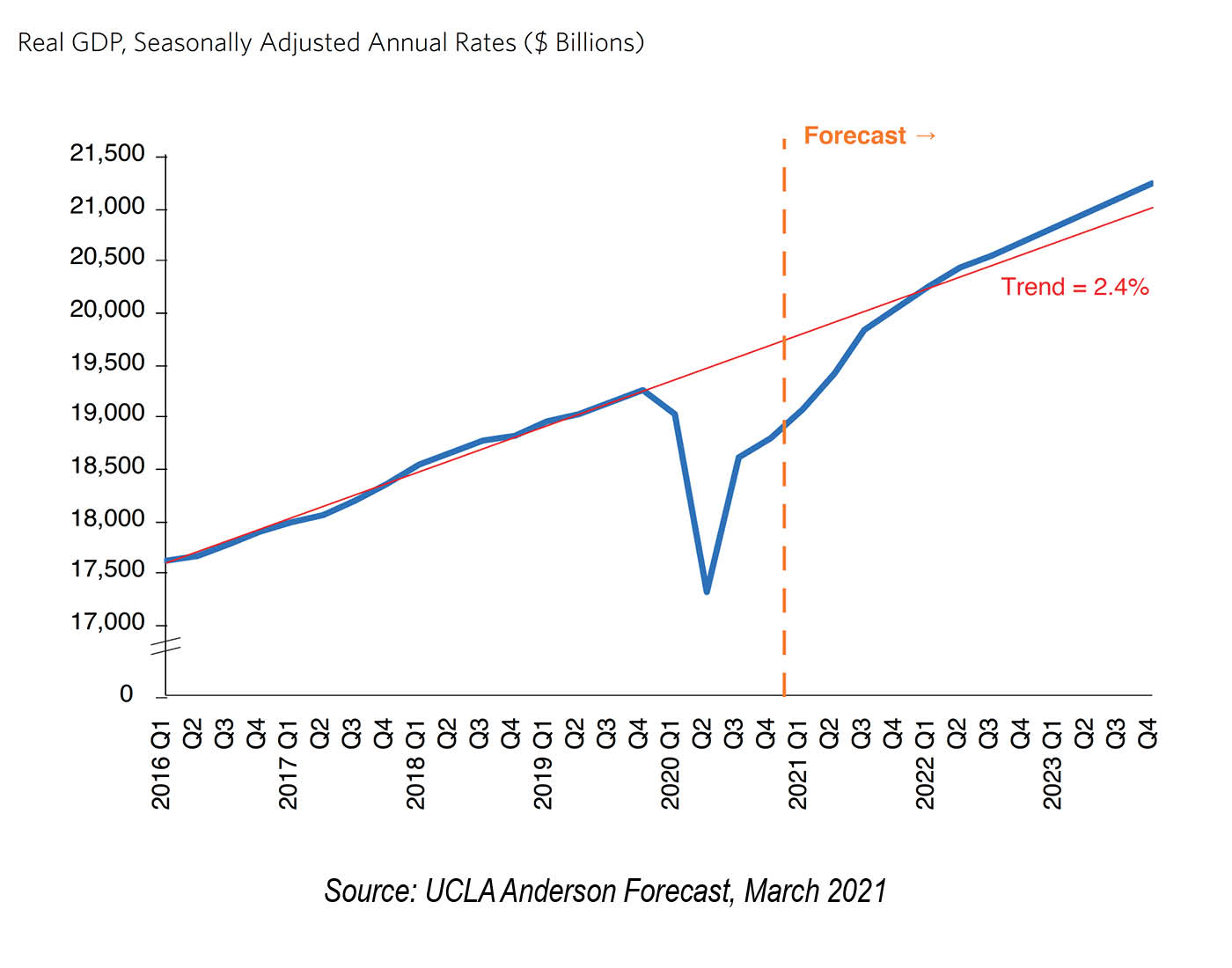

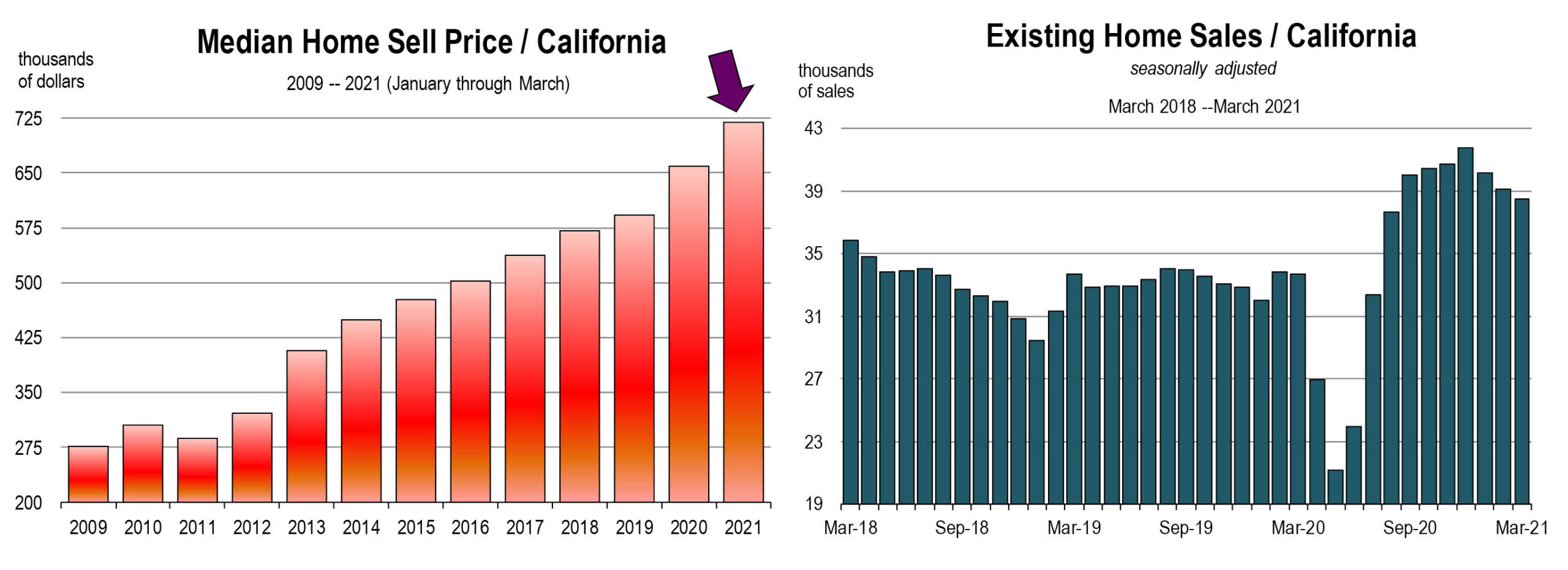

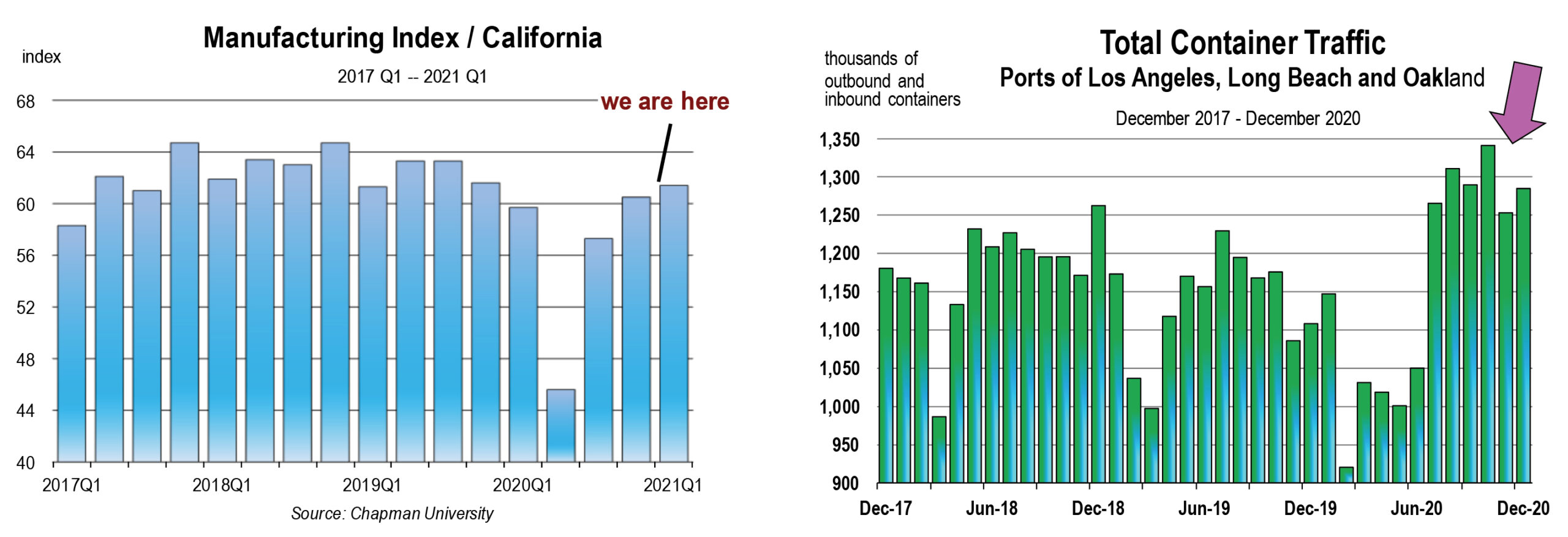

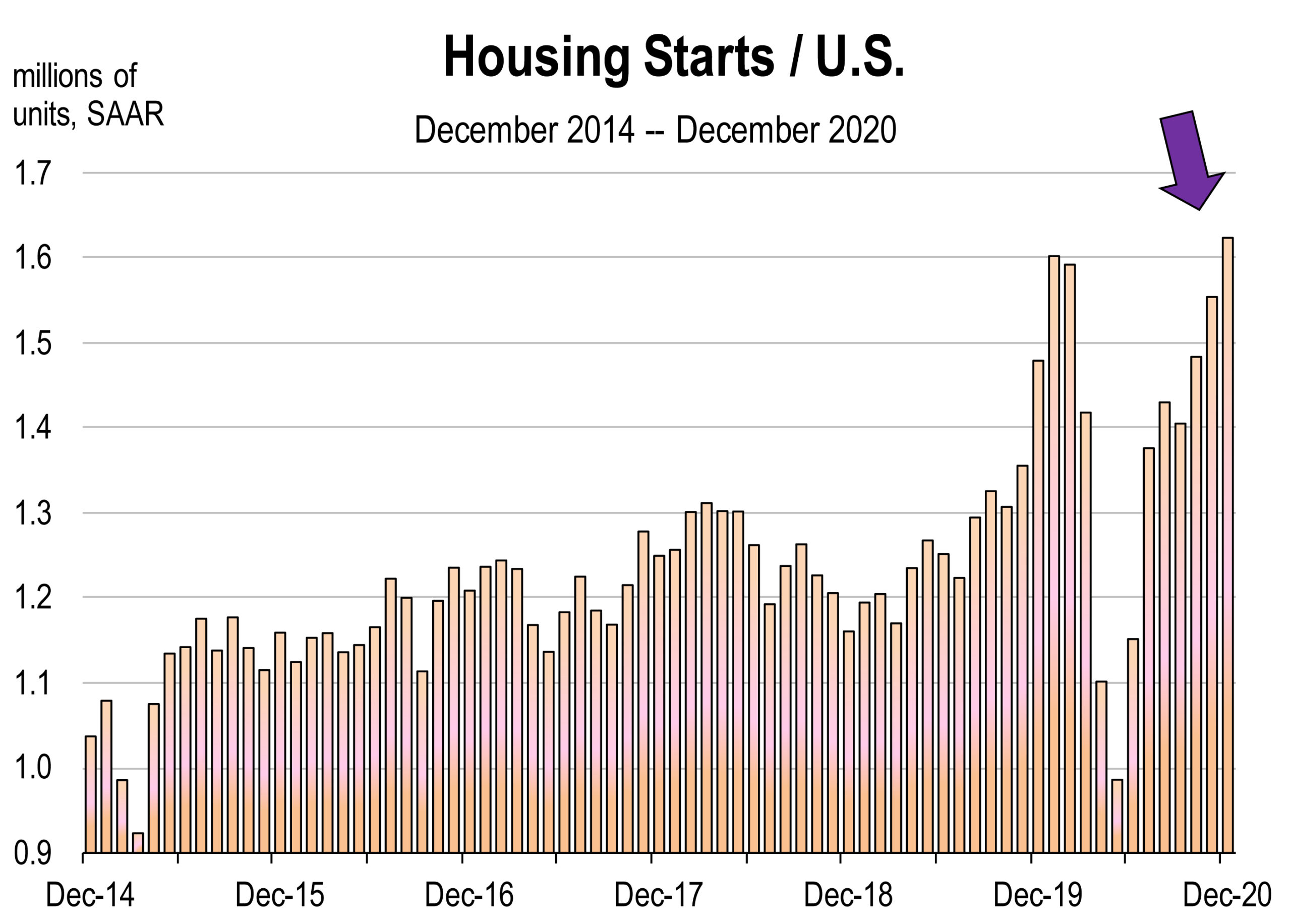

Housing is one particular indicator that is contributing largely to GDP improvement.

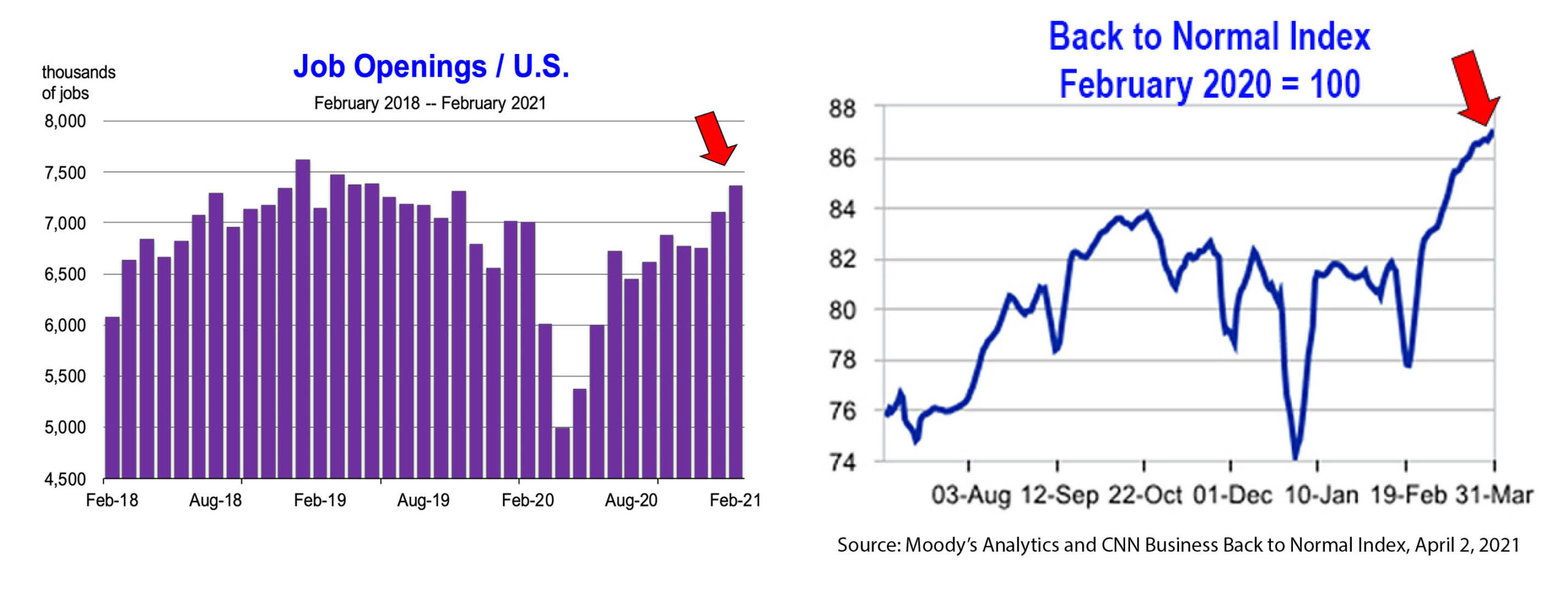

Housing is one particular indicator that is contributing largely to GDP improvement. New claims for unemployment benefits have declined during the last two weeks of January. This is encouraging news although the level of claims is still extremely high. Too many American workers are still out of work. The unemployment rate is 6.7 percent. But add to that the four million people who were working a year ago but have dropped out of the labor force and are therefore not included as unemployed. Counting them would boost the nation’s unemployment rate to 9.0 percent.

New claims for unemployment benefits have declined during the last two weeks of January. This is encouraging news although the level of claims is still extremely high. Too many American workers are still out of work. The unemployment rate is 6.7 percent. But add to that the four million people who were working a year ago but have dropped out of the labor force and are therefore not included as unemployed. Counting them would boost the nation’s unemployment rate to 9.0 percent. 2020 is now in the rear view mirror. For the economy and for most every living person, the year was horrific. If anyone was guessing, they’d likely say that the outlook for 2021 would be better if not infinitely better, especially now that the world is being vaccinated meaning the pandemic will soon be eradicated.

2020 is now in the rear view mirror. For the economy and for most every living person, the year was horrific. If anyone was guessing, they’d likely say that the outlook for 2021 would be better if not infinitely better, especially now that the world is being vaccinated meaning the pandemic will soon be eradicated.